Court Upholds Separate Treatment of Units for Tax Deduction, Rejects Loss Adjus…

Full News

Court Upholds Separate Treatment of Units for Tax Deduction, Rejects Loss Adjustment

Court Upholds Separate Treatment of Units for Tax Deduction, Rejects Loss Adjustment

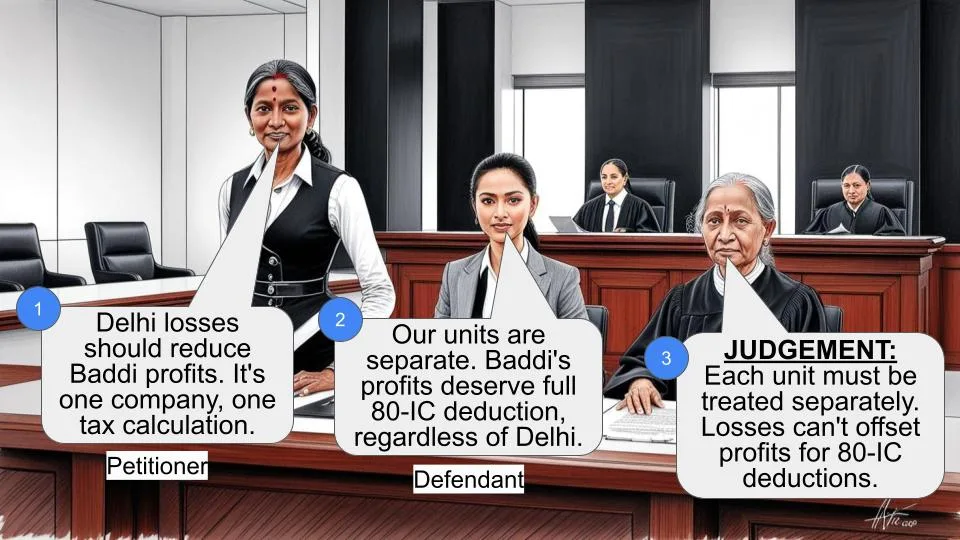

This case involves a dispute between the Commissioner of Income Tax and Gravs Appliance Pvt Ltd. The main issue was whether losses from the company's Delhi units could be adjusted against profits from its Baddi unit when calculating deductions under Section 80-IC (of Income Tax Act, 1961). The court ruled in favor of the assessee (Gravs Appliance), affirming that each unit should be treated separately for tax deduction purposes.

Case Name**: COMMISSIONER OF INCOME TAX VS. GRAVS APPLIANCE PVT LTD

**Key Takeaways**:

1. Each unit of a company must be treated separately for tax deduction purposes under Section 80-IC (of Income Tax Act, 1961).

2. Losses from one unit cannot be adjusted against profits from another unit when calculating eligible profits for deduction.

3. The court's decision reinforces the interpretation of Section 80-IA(5) (of Income Tax Act, 1961) and its application to Section 80-IC(7) (of Income Tax Act, 1961).

**Issue**:

Can the losses of Delhi units be adjusted while computing eligible profits in respect of the Baddi unit for granting deduction under Section 80-IC (of Income Tax Act, 1961)?

**Facts**:

1. The assessee, Gravs Appliance Pvt Ltd, owned three units: two in Delhi and one in Baddi, Himachal Pradesh.

2. The Baddi unit was eligible for benefits under Section 80-IC (of Income Tax Act, 1961).

3. For the Assessment Year 2006-07, the assessee declared a loss of ₹45,89,621 for its Delhi units.

4. The assessee claimed a deduction under Section 80-IC (of Income Tax Act, 1961) on the computed profit of ₹86,76,687 for the Baddi unit.

5. The Assessing Officer adjusted the losses of the Delhi units against the profits of the Baddi unit, arriving at an eligible profit of ₹40,44,824 for deduction under Section 80-IC (of Income Tax Act, 1961).

**Arguments**:

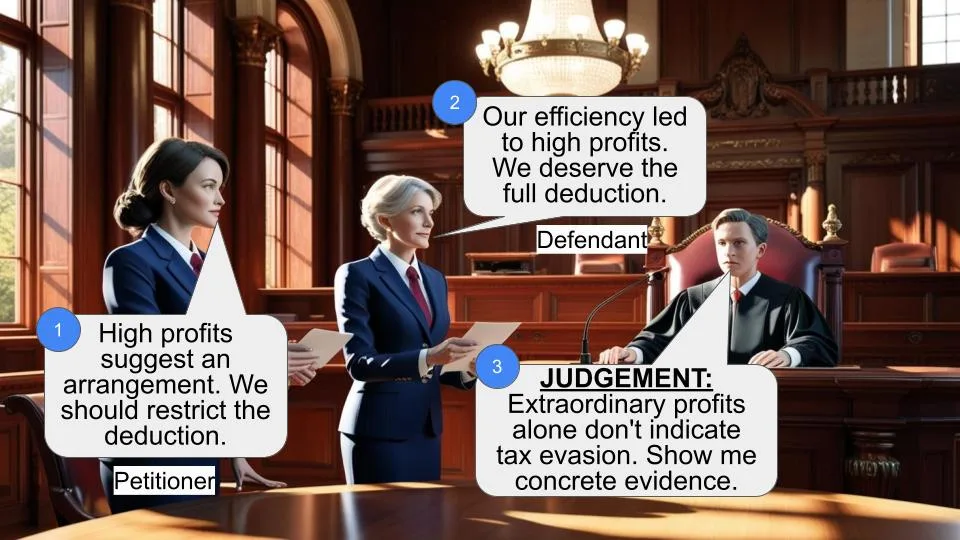

The Revenue (Income Tax Department) argued that the losses from the Delhi units should be adjusted against the profits of the Baddi unit before calculating the deduction under Section 80-IC (of Income Tax Act, 1961).

The assessee contended that each unit should be treated separately, and losses from one unit should not affect the deduction eligibility of another unit.

**Key Legal Precedents**:

1. CIT v. Dewan Kraft Systems P. Ltd., 297 ITR 305

2. CIT v. Sona Koyo Steering Systems Ltd., (2010) 321 ITR 463

These cases established that each industrial undertaking or unit should be treated separately and independently for the purpose of tax deductions under similar sections of the Income Tax Act.

**Judgement**:

The court dismissed the appeal of the revenue department and ruled in favor of the assessee. The key points of the judgment are:

1. The court affirmed that Section 80-IA(5) (of Income Tax Act, 1961), which is incorporated into Section 80-IC(7) (of Income Tax Act, 1961), requires each unit to be treated separately for tax deduction purposes .

2. The losses of the Delhi units cannot be adjusted while computing eligible profits for the Baddi unit under Section 80-IC (of Income Tax Act, 1961) .

3. The court agreed with the reasoning of the Income Tax Appellate Tribunal (ITAT) and found no fault in their approach .

4. The court clarified that the deduction cannot exceed the gross total income computed by the Assessing Officer, as per Section 80A(2) (of Income Tax Act, 1961) .

**FAQs**:

Q1: What was the main issue in this case?

A1: The main issue was whether losses from one unit of a company could be adjusted against profits from another unit when calculating tax deductions under Section 80-IC (of Income Tax Act, 1961).

Q2: How did the court rule on this issue?

A2: The court ruled that each unit should be treated separately, and losses from one unit cannot be adjusted against profits from another unit for tax deduction purposes.

Q3: What sections of the Income Tax Act were crucial in this case?

A3: Sections 80-IC and 80-IA(5) were crucial in this case, particularly the interpretation of how these sections interact.

Q4: Does this judgment apply to all types of tax deductions?

A4: This judgment specifically applies to deductions under Section 80-IC (of Income Tax Act, 1961), which incorporates provisions from Section 80-IA (of Income Tax Act, 1961). It may have implications for similar deductions, but it's best to consult a tax professional for specific cases.

Q5: Can the company still carry forward the losses from its Delhi units?

A5: The court mentioned that this matter should be considered by the Assessing Officer separately, as it wasn't part of the current dispute .

The Revenue, in this appeal, seeks to urge the following question of law: -

“Whether the Tribunal was justified in holding that the sum of 86,76,687/- could be granted the benefit of Section-80IC (of Income Tax Act, 1961) in respect of the unit in Baddi, Himachal Pradesh, without the deduction of the losses incurred by the Delhi units in the circumstances of the case?”

2. The Assessee had owned three units; two of them located in Delhi and the third at Baddi, Himachal Pradesh. The latter was eligible for benefit under Section 80 (of Income Tax Act, 1961) IC of the Income Tax Act. For the relevant period i.e. AY 2006-07, the assessee declared a loss of ` 45,89,621/- in respect of its two Delhi units. In respect of the Baddi unit, it claimed deduction under Section-80IC (of Income Tax Act, 1961) on the computed profit of ` 86,76,687/-. The Assessing Officer adjusted the losses of the Delhi units against the profits of the Baddi unit and arrived at profit eligible for deduction under Section 80 (of Income Tax Act, 1961) IC at 40,44,824/- The assessee carried the matter in appeal; the appeal was accepted by the CIT (A) who applied decisions of this Court including CIT v. Dewan Kraft Systems P. Ltd., 297 ITR 305. The Revenue’s appeal to the ITAT was dismissed by the impugned order. The relevant reasoning of the ITAT is as follows: -

“5. We have duly considered the rival contentions and gone through the record carefully. Hon'ble Delhi High Court, vide its order dated 10.2.2010, has disposed of appeals for assessment years 1992-03 to 1995-96 and 2000-01 in the case of Sona Koyo Sterling Systems Ltd. In that case, the issue relates to computation of deduction admissible under section 80I (of Income Tax Act, 1961). Hon'ble High Court has considered the meaning of gross total income as explained in section 80-B(5) (of Income Tax Act, 1961) as well as the conditions enumerated in sub-section (6) of section 80IA (of Income Tax Act, 1961). The Hon’ble Court has also considered its earlier decision in the case of Dewan Kraft Systems (P) Ltd. wherein section 80-IA(5) (of Income Tax Act, 1961) and (7) were considered. Hon’ble Court has held that sub-section (6) of section 80-I (of Income Tax Act, 1961) begins with a non-obstante clause, according to this section the quantum of deduction is to be computed as if the industrial undertaking were the only source of income of the assessee during the relevant year s. While explaining the provisions, Hon’ble Court has observed that in other words, each industrial undertaking or unit is to be treated separately and independently. This was observed because deduction under section 80IA (of Income Tax Act, 1961) would be admissible only in those units and industrial undertaking which have a profit or gain. In sub-section (7) of section 80IC (of Income Tax Act, 1961), it has been provided that provisions contained in sub-section (5) and subsections (7) to (12) of section 80-IA (of Income Tax Act, 1961) shall, so far as may be, applied to the eligible undertaking or enterprises under this section, meaning thereby that same provision would be applicable in section 80-IC (of Income Tax Act, 1961). Hon'ble Delhi High Court in the case of Dewan Kraft Systems (P) Ltd. and Sona Koyo (supra) has held that each unit will be considered independently. In view of the above, we are of the opinion that Learned First Appellate Authority has rightly applied the ratio of Hon'ble Delhi High Court and has rightly directed the Assessing Officer not to adjust the losses of Delhi Unit while computing the eligible profit in respect of Baddi Unit for granting deduction under section 80-IC (of Income Tax Act, 1961). No other issue was agitated before us. Hence, the appeal of the revenue is dismissed.

6. In the result, the appeal of the revenue is dismissed.”

3. This Court has carefully considered the submissions. It is noticed that the ITAT took into account the provisions of Section-80IA(5) (of Income Tax Act, 1961) which are incorporated into sub-section (7). A similar provision also of Section-80 (of Income Tax Act, 1961) IC. This provision reads as under:

“80-IA (5) Notwithstanding anything contained in /any other provision of this Act, the profits and gains of an eligible business to which the provisions of sub-section (1) apply shall, for the purposes of determining the quantum of deduction under that sub-section for the assessment year immediately succeeding the initial assessment year or any subsequent assessment year, be computed as if such eligible business were the only source of income of the assessee during the previous year relevant to the initial assessment year and to every subsequent assessment year up to and including the assessment year for which the determination is to be made. 80-IC (7) The provisions contained in sub-section (5) and sub-sections (7) to (12) of Section 80-IA (of Income Tax Act, 1961) shall, so far as may be, apply to the eligible undertaking or enterprise under this section.”

4. This Court is of the opinion that having regard to the express language of Section-80IC(5) (of Income Tax Act, 1961) as well as Section-80IC(7) (of Income Tax Act, 1961) which incorporates by reference Section-80IA(5) (of Income Tax Act, 1961), the approach adopted by the Tribunal cannot be faulted. The Court also noticed that the same reasoning has been indicated in another Division Bench ruling in CIT v. Sona Koyo Steering Systems Ltd.,(2010) 321 ITR 463.

5. As regards the question whether the assessee can carry forward the losses of the Delhi units, the matter is to be considered appropriately by the Assessing Officer. We express no opinion on the question as it does not arise out of the order of the Tribunal. However, it is clarified that the deduction cannot exceed the gross total income computed by the A.O. in this case, in view of Section-80A(2) (of Income Tax Act, 1961).

6. No substantial question of law arises for consideration.

7. The appeal is accordingly dismissed.

S. RAVINDRA BHAT, J

R.V.EASWAR, J

AUGUST 06, 2012

×

Questions

Court Upholds Separate Treatment of Units for Tax Deduction, Rejects Loss Adjustment

Write your CommentSimilar Posts

Generic

- Reportdata/5588.pdf