Court Upholds Extraordinary Profits for Tax Deduction, Rejects Revenue's Appeal

Full News

Court Upholds Extraordinary Profits for Tax Deduction, Rejects Revenue's Appeal

Court Upholds Extraordinary Profits for Tax Deduction, Rejects Revenue's Appeal

This case involves an appeal by the Revenue department against Schmetz India Pvt. Ltd., a subsidiary of a German company. The dispute centered around the company's claim for deduction under Section 10A (of Income Tax Act, 1961) for its manufacturing unit in Kandla, which showed extraordinary profits. The court ultimately ruled in favor of the company, rejecting the Revenue's arguments.

Case Name**: COMMISSIONER OF INCOME TAX VS SCHMETZ INDIA PVT. LTD.

**Key Takeaways**:

1. Extraordinary profits alone don't indicate an arranged setup for claiming higher deductions.

2. Efficient functioning shouldn't be penalized through tax assessments.

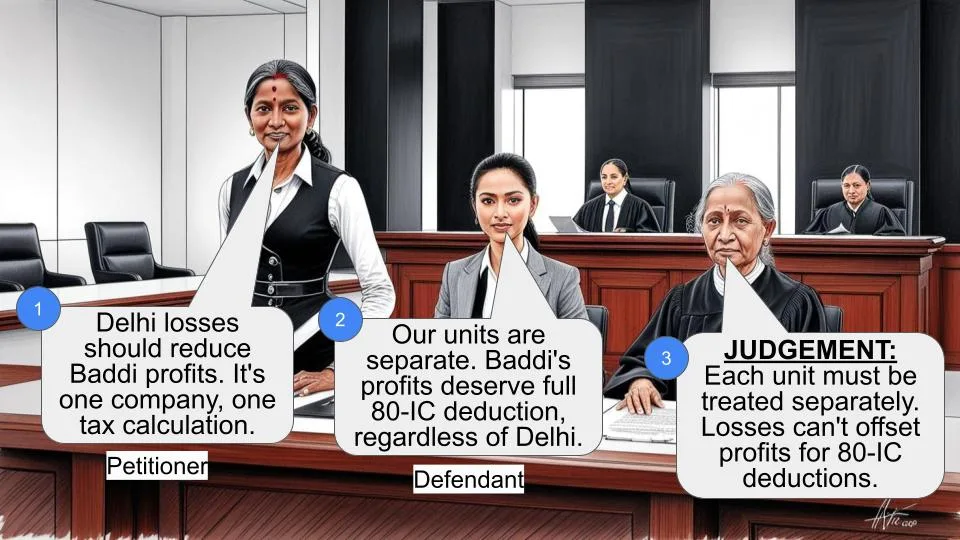

3. Losses from one unit cannot be set off against profits of another unit before claiming deductions under Section 10A (of Income Tax Act, 1961).

4. The court emphasized the importance of factual evidence in determining tax arrangements.

**Issue**:

Was the Income Tax Appellate Tribunal justified in allowing the assessee's claim for deduction under Section 10A (of Income Tax Act, 1961), despite the company showing abnormally high profits?

**Facts**:

1. Schmetz India Pvt. Ltd. is a wholly-owned subsidiary of a German company.

2. The company has two divisions in India:

a) A manufacturing unit in Kandla Free Trade Zone, producing and exporting industrial sewing machine needles.

b) A trading division in Mumbai, importing and selling different types of industrial sewing machine needles.

3. For the assessment year 2004-2005, the Kandla unit declared an income of Rs. 20.54 crores and claimed 100% deduction under Section 10A (of Income Tax Act, 1961).

4. The Mumbai trading division showed a loss of Rs. 70.29 lacs.

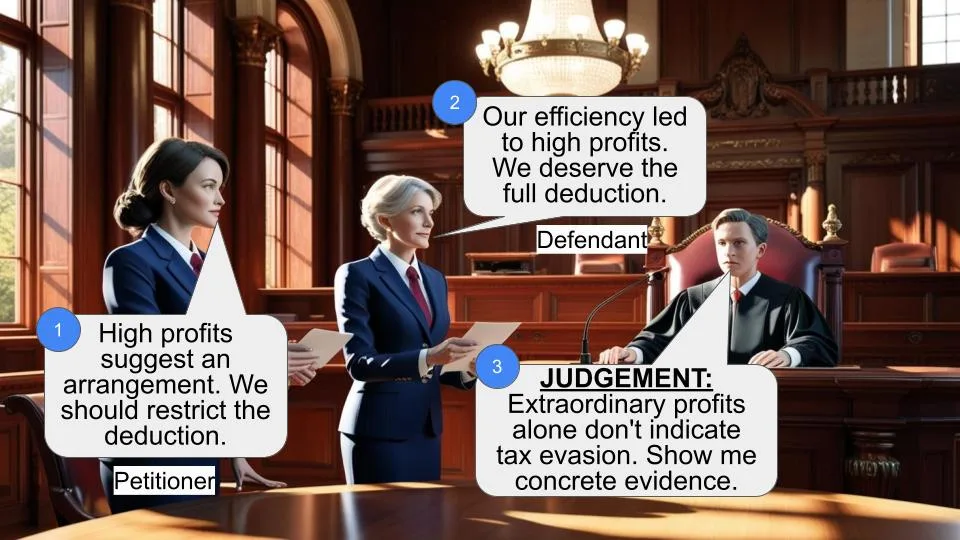

5. The Assessing Officer found the profits of the Kandla unit to be abnormally high and restricted the deduction under Section 10A (of Income Tax Act, 1961).

**Arguments**:

Revenue's Arguments:

1. The abnormally high profits of the Kandla unit were due to an arrangement with the German company to boost profits and claim higher deductions.

2. The Assessing Officer was justified in estimating lower profits for the 10A unit.

3. Losses from the trading unit should be set off against profits of the export-oriented unit before claiming deduction under Section 10A (of Income Tax Act, 1961).

Assessee's Arguments:

1. Higher profits were due to efficient functioning, not any special arrangement.

2. The company provided reasons for higher profits, including secured sales, bulk packing, and problem-free production.

3. Deduction under Section 10A (of Income Tax Act, 1961) should be computed without setting off losses from the trading unit.

**Key Legal Precedents**:

1. CIT v. Black & Veatch Consulting Pvt Ltd ITA (Lodging) No. 1237 of 2011 - This case was cited to support the argument that deduction under Section 10A (of Income Tax Act, 1961) should be computed without setting off losses from other units.

**Judgement**:

1. The court dismissed the Revenue's appeal and upheld the Tribunal's decision in favor of the assessee.

2. It was held that extraordinary profits alone cannot lead to the conclusion of an arranged setup.

3. The court agreed that deduction under Section 10A (of Income Tax Act, 1961) should be computed without setting off losses from the trading unit against profits of the export-oriented unit.

4. The court found no perversity or arbitrariness in the Tribunal's findings of fact.

**FAQs**:

1. Q: Why did the court reject the Revenue's argument about abnormal profits?

A: The court held that extraordinary profits alone don't indicate an arranged setup and that efficient functioning shouldn't be penalized.

2. Q: What was the significance of the different types of needles sold by the two divisions?

A: This fact negated the Revenue's argument about an arrangement between parties, as the products were different and not interchangeable.

3. Q: How did the court rule on setting off losses from one unit against profits of another?

A: The court agreed with the Tribunal that losses from the trading unit should not be set off against profits of the export unit before claiming Section 10A (of Income Tax Act, 1961) deduction.

4. Q: What sections of the Income Tax Act were central to this case?

A: Section 10A (of Income Tax Act, 1961) was the primary focus, with references to Section 80IA(10) (of Income Tax Act, 1961) and Section 10A(7) (of Income Tax Act, 1961) for the Assessing Officer's power to re-determine profits.

5. Q: What precedent does this case set for future tax assessments?

A: It emphasizes that tax authorities need concrete evidence of arrangements to disallow deductions, and efficient business operations resulting in high profits should not be penalized.

1. This appeal by the Revenue under Section 260A (of Income Tax Act, 1961) ('the Act') challenges the order dated 30.07.2008 of the Income Tax Appellate Tribunal ('the Tribunal') in ITA No. 7629/MUM/07 relating to the assessment year 2004-2005.

2. Being aggrieved by the order dated 30.07.2008 of the Tribunal, the Revenue has formulated the following questions of law for consideration of this court.

“Whether on the facts and in the circumstances of the case and in law the Tribunal was justified

A) in coming to the conclusion that there was nothing on record to show that the profits arrived at by the assessee in respect of the 10A unit carrying on the business of manufacturing Industrial Sewing Machine Needless was not in the normal course of its business and that the abnormally high profit was due to extraordinary arrangement between the assessee and the German company entered into only with a view to boost the profits of assessee and therefore allowing deduction of Rs.20,54,27,335/?

B) in holding that the there was no material available with the A.O. to estimate the profits of the 10A unit eligible for deduction invoking the provisions of S.80 IA(10) read with S.10A(7) of the Act was based on proper and reasonable appraisal of the material available on record?

C) in holding that the deduction under S. 10A of the Act has to be computed without setting off of the loss from the trading unit against the profits of the export oriented unit entitled to deduction under S.10A of the Act.?

3. The respondent assessee is a wholly owned subsidiary of a German Company. The respondent- assessee has two divisions in India. One division at Kandla in the Kandla Free Trade Zone, is engaged in the manufactures and export of industrial sewing machine needles. The other division at Mumbai is engaged in trading in industrial sewing machine needles. The manufacturing division at Kandla exports its entire production of industrial machine needles to its holding/principal company in Germany. The industrial sewing machine needles imported by the respondent from Germany are of a variety different from those manufactured and exported by it from the Kandla division.

4. The respondentassessee for the assessment year 20042005 declared an income of Rs.20.54 crores from its manufacturing division at Kandla and claimed 100% deduction under Section 10A (of Income Tax Act, 1961). During the course of the assessment proceedings, the Assessing Officer was of the view that abnormal profits had been declared in respect of the Kandla division, only in view of the income therefrom being exempt under Section 10A (of Income Tax Act, 1961). This view of the Assessing Officer was strengthened by the fact that the trading division at Mumbai showed a loss of Rs.70.29 lacs. Consequently, the Assessing Officer called upon the respondentassessee to explain the abnormal profits at Kandla division and also why the provisions of Section 10A(7) (of Income Tax Act, 1961) read with Section 80IA(10) (of Income Tax Act, 1961) should not be invoked. The above provision empowers an Assessing Officer to redetermine the profits which may be reasonably deemed to have arisen from such eligible business in case he is of the view that the undertaking has declared more than ordinary profits. The respondent assessee responded to the query and pointed out that the reasons for higher profits were as under :

“i) The entire production of the company is being exported to Associated Enterprises and accordingly there is no risk of unsold finished goods. This results in the company concentrating mainly on the production side.

ii) The company does not have to wait for the orders on the basis of which the production line is determined. But the company has large variety of the products to be manufactured for the Associated Enterprises. This results in machinery working at full capacity which results in the best results.

iii) The sales of the company being secured no marketing efforts or cost is involved.

iv) The sales are affected in bulk packing conditions, which saves the cost of packing materials too.

v) The basic raw material is being imported from the Associated Enterprises which results in problem free production and no chances of major rejection which could account for any losses.

vi) The Associated Enterprises is 100% holding equity and provides all finance arrangements. Thus, there is no interest burden on the company for its working capital requirements.”

5. The Assessing Officer placed reliance upon the chart submitted by assessee to show the details of expenses, gross profits etc. arising in comparable cases. On the basis of the above chart, the Assessing Officer concluded that the profits of the business of the respondentassessee for the purpose of deduction under Section 10A (of Income Tax Act, 1961) has to be arrived at by adopting 60% gross profit ratio as against 77.91% shown by the assessee. The deduction therefore under Section 10A (of Income Tax Act, 1961) was restricted by the Assessing Officer to Rs.13.17 crores and the balance of Rs.6.83 crores was brought to tax under the head 'Income from Other Sources'. Further, the Assessing Officer also held that the trading loss of Rs.70.29 lacs from its trading division at Mumbai should be first set off against manufacturing income at Kandla division before deduction under Section 10A (of Income Tax Act, 1961) can be claimed by the Kandla division.

6. Being aggrieved, on both the above counts the respondentassessee filed an appeal to the Commissioner of Income Tax (Appeals). By an order dated 24.08.2007, the Commissioner of Income Tax (Appeals) held that the gross profit ratio of 60% adopted by the Assessing Officer as against 77.91% gross profit ratio declared by the assessee was reasonable. The profits in excess of the above was correctly brought to tax as 'income from other sources'. So far as the second issue is concerned, the Commissioner of Income Tax (Appeals) held that before exemption of income under Section 10A (of Income Tax Act, 1961) is availed, the respondentassesee must set off the losses of other units against the income of 10A units and only the balance amount available thereafter would be allowed deduction under Section 10A (of Income Tax Act, 1961). Thus, the Commissioner of Income Tax (Appeals) upheld the order of the Assessing Officer.

7. In second appeal, the Tribunal by its order dated 30.07.2008 held that merely because an assessee makes extraordinary profits, it would not lead to the conclusion that the same was organised/arranged. This according to the Tribunal would penalize efficient functioning of the unit.

The Tribunal was of the view that the Assessing Officer has not been able to prove that any arrangement had been arrived between the parties which resulted in extraordinary profits to the respondentassessee's manufacturing division at Kandla. Consequently, the reworking of the profits by the Assessing Officer was not proper. The Assessing Officer had completely ignored the fact that as the entire production of the respondent- assessee was being sold to its German principal/holding company, they did not have any expenses of marketing etc. This resulted in it being focused in reducing the cost of operation, which resulted in higher profits. The Tribunal therefore, held that the profits derived by the respondentassessee from its export division at Kandla should be taken at Rs.20.53 crores and considered for relief under Section 10A (of Income Tax Act, 1961). So far as, the second issue is concerned namely whether Section 10A (of Income Tax Act, 1961) deduction by Kandla division should be claimed after setting off the loss of its trading division at Mumbai or prior thereto the Tribunal held that the deduction to the Kandla division would be available on its profits under Section 10A (of Income Tax Act, 1961). The losses suffered by Mumbai division (trading division) should not be set off against the profits of Kandla division before claiming the deduction under Section 10A (of Income Tax Act, 1961).

8. So far as questions (a) & (b) are concerned, we find that the Tribunal has considered the entire evidence and on facts come to the conclusion that the profits earned by Kandla division of the respondentassessee is not abnormally high due to any arrangement between the respondentassessee and its German Principal. The Tribunal correctly held that extraordinary profits cannot lead to the conclusion that this is an arrangement between the parties. This would penalize efficient functioning. Further, the authorities have also recorded a finding that the industrial sewing machine needles imported and traded by the Mumbai division are different from those manufactured & exported by the Kandla division. Consequently, this also negatives any arrangement between the parties to show extraordinary profits in respect of its Kandla division so as to claim deduction under Section 10A (of Income Tax Act, 1961). These are findings one of fact. The appellantrevenue have not been able to show that the findings are perverse or arbitrary. In the circumstances, questions (a) and (b) as formulated by the appellant/revenue do not raise substantial questions of law in the present facts and are therefore dismissed.

9. So far as, question (c) is concerned, both the respondentassessee and appellantrevenue agree that the issue is covered in favour of the respondentassessee by the decision of this court in ITA (Lodging) No. 1237 of 2011 in CIT v. Black & Veatch Consulting Pvt. Ltd. dated 09.04.2012.

Therefore, question (c) is answered in the affirmative i.e. in favour of the respondent- assessee and against the appellantrevenue.

10. The appeal is disposed of in above terms. No order as to costs.

(M.S. SANKLECHA, J.) (S.J.VAZIFDAR, J.)

×

Similar Ripples

Questions

Court Upholds Extraordinary Profits for Tax Deduction, Rejects Revenue's Appeal

Write your CommentSimilar Posts

Generic

- Reportdata/5483.pdf