Court Upholds Tax Addition When Transaction Shrouded in Mystery

Full News

Court Upholds Tax Addition When Transaction Shrouded in Mystery

Court Upholds Tax Addition When Transaction Shrouded in Mystery

This case involves P.C. CHANDRA AND SONS (INDIA) PVT. LTD. AND ANOTHER (the appellant/assessee) challenging a tax assessment made by the Deputy Commissioner of Income Tax. The High Court upheld the decision of the Income Tax Tribunal, which had previously affirmed the Commissioner of Income Tax (Appeals)'s order. The court found that the Assessing Officer was justified in making additions to the assessee's income when the entire transaction was shrouded in mystery.

Case Name**: P.C. CHANDRA AND SONS (INDIA) PVT. LTD. AND ANOTHER VS DEPUTY COMMISSIONER OF INCOME TAX **Key Takeaways**: 1. When a transaction lacks clarity or is "shrouded in mystery," tax authorities are justified in making additions to the assessed income. 2. Inconsistent statements from involved parties can weaken the assessee's case. 3. The court is unlikely to interfere with factual findings of lower tax authorities unless there's a substantial question of law. **Issue**: Was the Assessing Officer justified in making additions to the assessee's income when the entire transaction was unclear or "shrouded in mystery"? **Facts**: 1. The case relates to the assessment year 2011-2012. 2. The Income Tax Department raised a demand of Rs.12,11,86,487/- on the assessee. 3. The assessee's appeal was pending before the Commissioner of Income Tax (Appeals). 4. An order dated July 17, 2014, under Section 220(6) (of Income Tax Act, 1961), required the assessee to pay 50% of the total demand. 5. The assessee's request for staying the demand was rejected by the Commissioner of Income Tax, Kolkata – I on September 4, 2014. 6. The assessee's bank accounts, including cash credit accounts, were attached by the income tax authorities. **Arguments**: Assessee's argument: 1. The demand was unjust on its face. 2. A sum of Rs.26,35,09,093/- was incorrectly added to their income. 3. The addition was based on an erroneous assumption about the conversion of gold from 24 carats to 22 carats. Tax Department's argument: The quantity of pure gold declared was mixed with alloy, reducing the proportion of pure gold from 24 carats to 22 carats, and the excess quantity was sold in the market for the "added back" amount. **Key Legal Precedents**: 1. K.M. Adam vs. Income-Tax Officer, II Additional II Circle, Madras (33 ITR 26): This Madras High Court decision opines that a loan fund cannot be said to be a debt of the bank to the customer nor could it be said to be money on account of the customer. Hence, it cannot be attached. **Judgement**: 1. The High Court found no reason to interfere with the order of the Tribunal. 2. The court agreed that when a transaction is shrouded in mystery, the Assessing Officer is justified in making additions. 3. The court found that all issues raised by the appellant were pure questions of fact, which the Assessing Officer had thoroughly analyzed. 4. No substantial question of law was found to arise for consideration. However, the court did provide some relief to the assessee: 1. The attachment on the cash credit account with Allahabad Bank, Bowbazar Branch was discharged. 2. Other bank accounts remained attached, but the department was not allowed to appropriate any sum until the disposal of the appeal before the Commissioner (Appeals). 3. The Commissioner of Income Tax (Appeals) was directed to dispose of the appeal by December 31, 2014. **FAQs**: 1. Q: What does "shrouded in mystery" mean in this context? A: It means that the details of the transaction were unclear, inconsistent, or not fully disclosed, making it difficult for tax authorities to verify its legitimacy. 2. Q: Why did the court uphold the addition to income? A: The court found that the Assessing Officer had thoroughly analyzed the facts and that the transaction lacked clarity, justifying the addition. 3. Q: Did the assessee receive any relief from the court? A: Yes, the court discharged the attachment on one cash credit account and prevented the tax department from appropriating funds from other accounts until the appeal was resolved. 4. Q: What's the significance of this judgment for other taxpayers? A: It emphasizes the importance of maintaining clear and consistent records of transactions, as lack of clarity can lead to unfavorable tax assessments. 5. Q: What happens next in this case? A: The Commissioner of Income Tax (Appeals) was directed to dispose of the appeal, which would determine the final outcome of the tax dispute.

The concerned assessment order is 2011-2012. There is a demand from the Income Tax Department upon the assessee-writ petitioner for a sum of Rs.12,11,86,487/-.

Against the assessment order in question the assessee’s appeal before the Commissioner of Income Tax (Appeals) is pending. By an order dated 17th July 2014 passed under Section 220(6) (of Income Tax Act, 1961) the assessee was required to pay 50% of the total demand in the following manner:

Rs. 2.10 crores i.e. 10% of the above demand immediately and the balance 40% i.e. Rs.8.40 crores in six monthly installments of Rs.1.40 crores each, starting from the end of July, 2014.

Although in the said order the assessee has been asked to pay 50% of the demand, a mere look at the demand would show that the assessee was asked to deposit 100% of the demand. Being aggrieved the assessee approached the Commissioner of Income Tax, Kolkata – I. However, by his decision dated 4th September 2014 the request of the assessee for staying the demand was rejected.

A further approach has been made before the Principal Commissioner of Income Tax regarding which there is no response till date. On 10th September 2014 the order dated 17th July 2014 was “annulled”.

Mr. J. P. Khaitan, learned senior advocate for the petitioner tries to unfold the prima facie case of the assessee to show that the demand ex facie is unjust. To a substantial extent he has been able to establish such prima facie case.

On a reading of paragraph 10 of the assessment order it shows that a sum of Rs.26,35,09,093/- has been added to the income of the assessee. The ground on which this income has been added is that the quantity of pure gold as declared was mixed with alloy bringing down the proportion of pure gold in the product from 24 carats to 22 carats. An excess quantity than what was declared was produced and sold in the market for the “added back” amount. This, according to Mr. Khaitan, and I accept Mr. Khaitan’s contention, is not quite correct. According to the summary of stock which is annexed to the writ petition at page 177 thereof and is also part of the writ petitioner’s audited accounts, the quantity of gold of 24 carats which was said to have been converted to 22 carats upon addition of alloy was in fact of only 22 carats. It is nobody’s case that that particular quantity of gold was further converted to gold of lesser carat value. The addition of Rs. 26,35,09,093/- made on the said basis is prima facie erroneous.

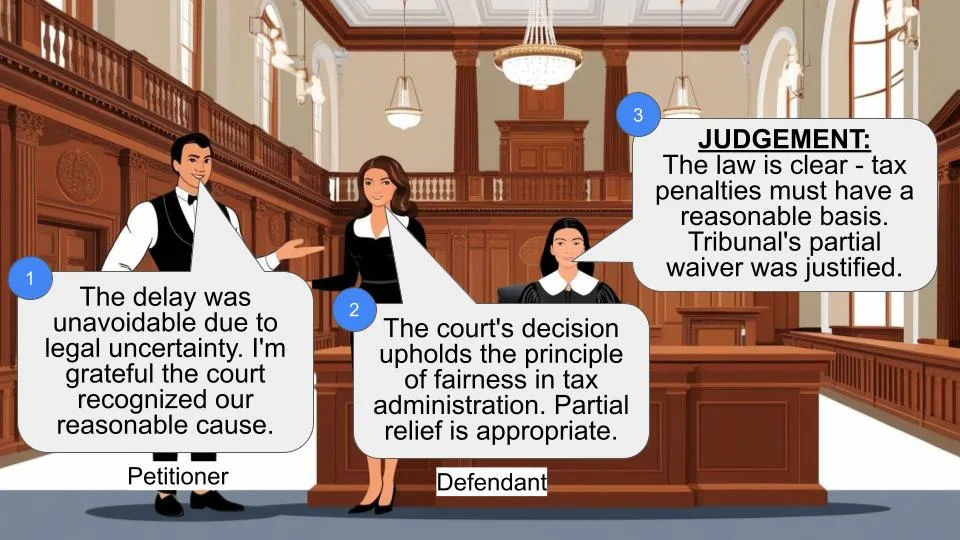

Therefore, in my opinion, the writ petitioner has a substantial case to be tried before the Commissioner (Appeals). After filing of the petitioner’s application before the Principal Commissioner of Income Tax the banks accounts including the cash credit accounts of the writ petitioner have been attached by the income tax authorities.

In my opinion, the petitioner should be relieved of some of the rigours of this attachment.

I discharge the attachment with regard to the cash credit account of the petitioner with Allahabad Bank, Bowbazar Branch. In this I am supported by a decision of the Madras High Court in K. M. Adam vs. Income-Tax Officer, II Additional II Circle, Madras reported in 33 ITR 26 which opines that a loan fund cannot said to be a debt of the bank to the customer nor could it be said to be money on account of the customer. Hence it cannot be attached.

I direct the Commissioner of Income Tax (Appeals) to dispose of the appeal by 31st December 2014. Other bank accounts of the writ petitioner with Union Bank of India, Sealdah Branch and Bank of India, Bowbazar Branch will continue to remain attached with a rider that the department will not be able to appropriate any sum therefrom till the disposal of the appeal before the Commissioner (Appeals).

The continuance of attachment and operation of bank accounts will abide by the order to be passed by Commissioner (Appeals).

Nothing remains of this application.

It is disposed of by this order.

Allegations contained in the writ petition are deemed not to be admitted.

Certified photocopy of this order, if applied for, be supplied to the parties upon compliance with all requisite formalities.

(I. P. MUKERJI, J.)

×

Questions

Court Upholds Tax Addition When Transaction Shrouded in Mystery

Write your CommentSimilar Posts

Generic

- Reportdata/4573.pdf