Court Upholds Taxpayer's Right to Interest Waiver in Land Acquisition Case

Full News

Court Upholds Taxpayer's Right to Interest Waiver in Land Acquisition Case

Court Upholds Taxpayer's Right to Interest Waiver in Land Acquisition Case

This case involves Anupinder Singh, a landowner who received enhanced compensation for acquired land. The dispute centered around the waiver of interest on delayed tax filing. The court ruled in favor of the petitioner, stating that interest should be waived until the date of receipt of enhanced compensation.

Case Name**: ANUPINDER SINGH VS COMMISSIONER OF INCOME TAX & ANR

**Key Takeaways**:

1. The Commissioner's discretion under Section 273A (of Income Tax Act, 1961) must be exercised judiciously and objectively.

2. Interest waiver should be considered up to the date of actual receipt of compensation, not just the date of court judgment.

3. The case emphasizes the importance of considering practical realities in tax matters related to land acquisition compensation.

**Issue**:

Should the petitioner be granted a full waiver of interest under Sections 139(8) (of Income Tax Act, 1961) and 217 of the Income Tax Act for delayed filing of returns related to enhanced land acquisition compensation?

**Facts**:

1. Anupinder Singh owned agricultural land that was acquired by the State Government on 12.10.1979.

2. The compensation was enhanced through court judgments, with the final judgment on 7.10.1988.

3. The petitioner received the enhanced compensation between July and November 1989 in two installments.

4. Income tax returns for assessment years 1982-83 to 1988-89 were filed voluntarily before any notices were issued.

5. The Assessing Officer charged interest under Sections 139(8) (of Income Tax Act, 1961) and 217 of the Income Tax Act.

6. The Commissioner partially waived interest up to 30.11.1988, citing that the petitioner knew about the liability on 7.10.1988.

**Arguments**:

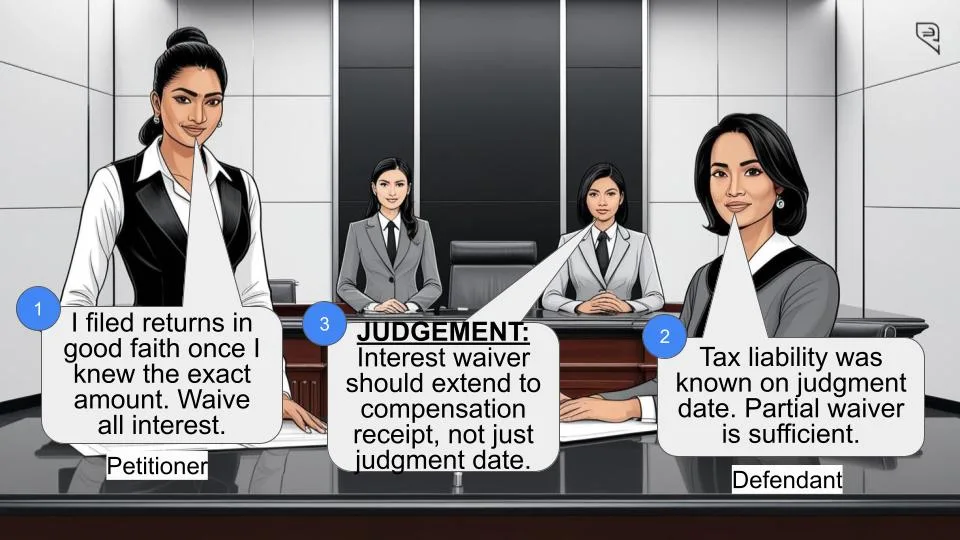

Petitioner's Argument:

- The returns were filed voluntarily and in good faith after receiving the enhanced compensation.

- The exact amount of compensation was unknown until receipt, justifying the delay in filing returns.

- Complete waiver of interest under Sections 139(8) (of Income Tax Act, 1961) and 217 should be granted.

Commissioner's Argument:

- The liability to pay tax was known to the assessee on 7.10.1988 when the High Court judgment was received.

- Returns should have been filed by 30.11.1988, but were filed on 18.5.1990.

- Partial waiver up to 30.11.1988 was justified, but not for the remaining period.

**Key Legal Precedents**:

1. Shanti Sarup Sharma v. Commissioner of Income Tax and another, (1999) 237 ITR 376

2. Parkash Devi (Smt.) v. CWT (1983) 141 ITR 122

3. Apex Finance and Leasing Limited v. Commissioner of Income Tax and others, (1994) 207 ITR 781

4. Ganesh Trading Co. v. Commissioner of Income Tax and another, (2004) 265 ITR 495

These cases established principles for waiver of interest and interpretation of Section 273A (of Income Tax Act, 1961).

**Judgement**:

The court partially allowed the petition, ruling that:

1. The Commissioner erred in limiting the waiver to 30.11.1988.

2. The petitioner was entitled to waiver of interest until the date of actual receipt of enhanced compensation (July to November 1989).

3. The matter was remanded to the Commissioner for passing a fresh order in accordance with the court's observations.

**FAQs**:

1. Q: Why did the court disagree with the Commissioner's decision?

A: The court found that the Commissioner didn't consider the actual date of receipt of compensation, which was crucial for determining when the petitioner could accurately file returns.

2. Q: What is the significance of Section 273A (of Income Tax Act, 1961)?

A: Section 273A (of Income Tax Act, 1961) gives the Commissioner discretionary power to reduce or waive interest and penalties, but this discretion must be exercised judiciously and objectively.

3. Q: How does this judgment impact similar cases?

A: It sets a precedent for considering the practical aspects of when taxpayers actually receive compensation in land acquisition cases, rather than just relying on the date of court judgments.

4. Q: What are the key conditions for waiver under Section 273A (of Income Tax Act, 1961)?

A: The key conditions include voluntary filing of returns, good faith, full disclosure of wealth, cooperation in assessment, and satisfactory arrangements for tax payment.

5. Q: Does this judgment provide complete waiver of interest?

A: Not necessarily. It directs the Commissioner to reconsider the waiver up to the date of actual receipt of compensation, which may result in a more extensive, but not necessarily complete, waiver.

1. This order shall dispose of Civil Writ Petition Nos.14724 to 14727 of 1993 as learned counsel for the parties are agreed that the facts and the issue involved are identical in all the petitions. However, the facts are being taken from CWP No.14724 of 1993 which may be briefly noticed.

2. In CWP No.14724 of 1993, the petitioner was co-owner of agricultural land measuring 9 bighas 14 biswas situated in the revenue estate of Village Barewal, District Patiala. The said land was acquired by the State Government on 12.10.1979 and the compensation was determined by the Land Acquisition Collector. The petitioner challenged the award before the District Judge, Patiala. Compensation was enhanced to ` 96,800/- per acre. On further appeal, the amount of compensation was enhanced to ` 2,42,000/- per acre by this Court vide judgment dated 7.10.1988. Aggrieved by the judgment, the State of Punjab filed LPA No.248 of 1989 in this Court which was dismissed on March 8, 1989. The petitioner received compensation from July to November 1989 in two installments. The petitioner filed income tax returns for the assessment years 1982-83 to 1988-89 prior to the issuance of notices either under section 139(2) (of Income Tax Act, 1961) or under section 148 (of Income Tax Act, 1961) (in short, “the Act”). The assessment was completed on the basis of income declared by the Assessing Officer on 30.4.1991. However, the Assessing Officer charged interest under sections 139(8) (of Income Tax Act, 1961) and 217 of the Act and also ordered to initiate penalty proceedings under section 271(1)(a) (of Income Tax Act, 1961) and 273(b) of the Act. The penalty proceedings ordered to be initiated were later on withdrawn. On appeal, the Deputy Commissioner of Income Tax (Appeals) Chandigarh Range Chandigarh deleted the interest charged under sections 139(8) (of Income Tax Act, 1961) and 217 of the Act in respect of assessment years 1982-83 to 1984-85. The department went in appeal against the said order before the Tribunal. The petitioner moved a petition under section 273A (of Income Tax Act, 1961) for waiver of interest and penalty imposable/imposed for the assessment years 1983-84 to 1988- 89 on 9.1.1991. According to the petitioner, the returns for the relevant assessment years had been filed voluntarily and in good faith which were accepted by the Assessing Officer. The Commissioner of Income Tax vide order dated 9.2.1993, Annexure P.2 held that the liability to pay tax was known to the assessee on 7.10.1988 and at best he should have filed the returns by 30.11.1988 when he had received the judgment of the High Court on 4.11.1988 but the same were filed on 18.5.1990, thus, there was reasonable cause for delay for the period upto 30.11.1988 and for the remaining period, there was no proper justification for delay in filing the returns. The Commissioner, thus, waived interest under Sections 139(8) (of Income Tax Act, 1961) and 217 of the Act upto 30.11.1988 only. Hence these petitions.

3. Learned counsel for the petitioners submitted that the enhanced compensation and interest thereon was received and it was on that basis that the returns were filed for the earlier years and since the assessees had not known the exact amount of enhanced compensation and the interest in those years, charging of interest under Sections 139(8) (of Income Tax Act, 1961) and 217 of the Act in toto should have been waived. He placed reliance upon a Division Bench judgment of this Court in Shanti Sarup Sharma v. Commissioner of Income Tax and another, (1999) 237 ITR 376 to submit that the compensation and interest received from the Government on a subsequent date which was not ascertained at the time of due date for filing of the return for a particular assessment year, the interest under sections 139(8) (of Income Tax Act, 1961) and 217 of the Act was liable to be waived. Learned counsel further submitted that the Commissioner had erred in partly allowing the petition filed under section 273A (of Income Tax Act, 1961). Once the conditions as enumerated in Section 273A (of Income Tax Act, 1961) were fulfilled by the assessee,interest under sections 139(8) (of Income Tax Act, 1961)/217 of the Act ought to have been waived completely. Reliance was also placed on judgment of the Hon'ble Supreme Court in Apex Finance and Leasing Limited v. Commissioner of Income Tax and others, (1994) 207 ITR 781, Division Bench judgment of this Court in Smt.Parkash Devi v. Commissioner of Wealth Tax, Jullundur, (1983) 141 ITR 122, and Single Bench judgment of this Court in Ganesh Trading Co. v. Commissioner of Income Tax and another, (2004) 265 ITR 495 in support of the contentions.

4. After hearing learned counsel for the parties and perusing the record, we find that the writ petitions deserve to succeed.

5. A Division Bench of this Court while considering the provisions relating to Section 18B of the Wealth Tax Act, 1957 which are pari materia to those in Section 273A (of Income Tax Act, 1961), in Parkash Devi (Smt.) v. CWT (1983) 141 ITR 122, held that the following five conditions are required to be fulfilled:-

“1) that the returns were filed by the petitioner prior to the issuance of a notice to her under sub-section (2) of section 14 (of Income Tax Act, 1961);

2) that these were filed voluntarily and in good faith;

3) that the petitioner had made full and true disclosure of her net wealth;

4) that she had cooperated in the inquiry relating to the assessment of her net wealth; and

5) that she had paid or made satisfactory arrangements for the payment of the tax or interest payable in consequence of an order passed under the Act in respect of the relevant assessment years.”

6. Further, this Court while delving into the scope of Section 273A (of Income Tax Act, 1961) in Shanti Sarup Sharma's case (supra) held as under:-

“Section 273A (of Income Tax Act, 1961), empowers the Commissioner to reduce or waive interest and penalty. The power under Section 273A (of Income Tax Act, 1961) is discretionary. The Commissioner is given the discretion, when the requisite conditions envisaged by that section are satisfied, that he may waive or reduce the penalty or the interest imposable under the Act. However, the exercise of discretion cannot be either arbitrary or capricious and has to be judicious and objective. Section 273A (of Income Tax Act, 1961) does not confer absolute discretion upon the Commissioner to pass any order which he pleases to make. He is required to consider the application on the merits.”

7. Adjudicating the issue in favour of the petitioner, the Division Bench of this Court observed that the petitioner therein had received compensation in February 1991 and, therefore, there was no justification in charging interest for the earlier period.

8. Adverting to the factual matrix in the present case, the petitioner received the enhanced compensation during the period from July to November 1989 in two installments relating to assessment years 1982-83 to 1988-89. In such a situation, the rejection of the petition on the ground that the assessee had the order of the High Court available with him on 4.11.1988 and so the interest could be waived upto 30.11.1988, would not be correct. It was not disputed that the enhanced compensation and the interest was received between July to November 1989 and the assessee did not know before that the amount which was to be depicted in the income tax return for purposes of tax. The assessee was, thus, entitled for waiver of interest till the date of receipt of enhanced compensation.

9. In view of the above, all the four petitions are partly allowed and it is held that the Commissioner was not right in holding that there was no proper justification for delay after 30.11.1988 in filing return for the assessment years in question. The order Annexure P.2 in all the petitions is set aside to that extent. The matter is remanded to respondent No.1 for passing fresh order in accordance with law keeping in view the observations made hereinabove.

(Ajay Kumar Mittal)

Judge

July 19, 2012 (Gurmeet Singh Sandhawalia)

'gs' Judge

×

Similar Ripples

Questions

Court Upholds Taxpayer's Right to Interest Waiver in Land Acquisition Case

Write your CommentSimilar Posts

Generic

- Reportdata/5652.pdf