Court Upholds Tribunal's Decision: Matka Business Income Belongs to Usman M. Kh…

Full News

Court Upholds Tribunal's Decision: Matka Business Income Belongs to Usman M. Khan, Not G.R. Madhyan

Court Upholds Tribunal's Decision: Matka Business Income Belongs to Usman M. Khan, Not G.R. Madhyan

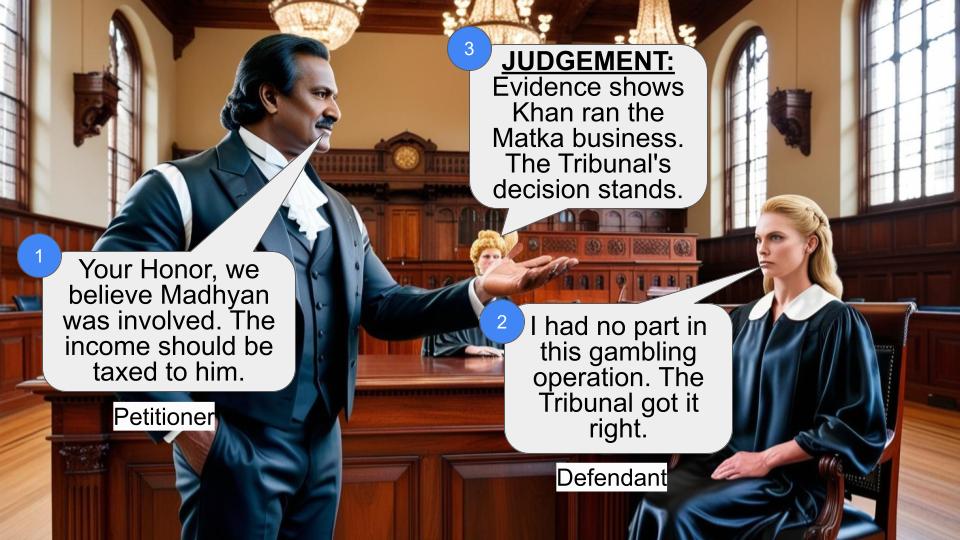

This case is all about a tax dispute between the Commissioner of Income Tax (the revenue department) and G.R. Madhyan. The main issue was whether Madhyan was involved in a Matka business (a type of gambling) and should be taxed on that income. The Income Tax Tribunal had earlier decided that Madhyan wasn't involved in the Matka business and that the income should be taxed to Usman M. Khan instead. The High Court agreed with the Tribunal's decision, essentially saying, "Yep, the Tribunal got it right.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs G.R. Madhyan (High Court of Bombay)

Income Tax Appeal No.431 of 2001

Date: 22nd January 2008

Key Takeaways:

1. The court emphasized the importance of respecting factual findings made by lower tribunals.

2. It highlighted that when a factual finding has been upheld in a related case, it can have a binding effect on similar cases.

3. The case demonstrates how tax assessments can be made on both substantive and protective bases, and how these can be challenged.

Issue:

The main question here was: Should the income from the Matka business be taxed in the hands of G.R. Madhyan (on a substantive basis) or Usman M. Khan (changing from a protective to a substantive basis)?

Facts:

1. The Assessing Officer initially taxed G.R. Madhyan on a substantive basis for the Matka business income.

2. The same officer taxed Usman M. Khan on a protective basis for the same income.

3. The Income Tax Appellate Tribunal (ITAT) decided that Madhyan wasn't involved in the Matka business at all.

4. The ITAT said the business belonged to Usman M. Khan and should be taxed to him on a substantive basis.

5. The revenue department (tax folks) weren't happy with this and appealed to the High Court.

Arguments:

The revenue department's main argument was that the ITAT was wrong in its decision to attribute the Matka business income to Usman M. Khan instead of G.R. Madhyan. They wanted the court to overturn the ITAT's decision.

G.R. Madhyan's side likely argued that the ITAT's decision was correct and based on factual findings, which shouldn't be disturbed by the High Court.

Key Legal Precedents:

The key precedent here was actually from a related case. The court mentioned that in a previous appeal (Income Tax Appeal No.330/2001) related to Usman M. Khan, they had already upheld the ITAT's finding that the income should be assessed in Khan's hands on a substantive basis. This decision was made on July 23, 2004.

The court essentially said, "Hey, we've already decided this issue in another case, so we're going to stick with that decision here too."

Judgement:

The High Court dismissed the revenue department's appeal. They said that since they had already upheld the ITAT's finding in the related case of Usman M. Khan, there was no reason to interfere with the ITAT's decision in this case. The court confirmed that the income from the Matka business should be taxed to Usman M. Khan on a substantive basis, not to G.R. Madhyan.

FAQs:

Q1: What's the difference between substantive and protective assessment?

A1: A substantive assessment is the primary tax assessment made on the person believed to be liable for the tax. A protective assessment is a backup assessment made on another person to protect the tax department's interests in case the primary assessment fails.

Q2: Why did the court give so much importance to the ITAT's findings?

A2: Courts generally respect the factual findings of lower tribunals unless there's a clear error. The ITAT, being closer to the evidence, is considered better placed to make factual determinations.

Q3: What does this mean for G.R. Madhyan?

A3: Good news for Madhyan! He won't be taxed for the Matka business income since the court agreed he wasn't involved in that business.

Q4: Could the revenue department appeal this decision further?

A4: While it's technically possible to appeal to the Supreme Court, the chances of success seem low given that this decision was based on factual findings already upheld in a related case.

Q5: What's the key lesson from this case for taxpayers?

A5: It shows the importance of challenging incorrect tax assessments at the tribunal level, as these factual findings can have a significant impact on future legal proceedings.

1. This is a appeal by revenue against the order dated 26.2.2001. By this common order a set of appeals preferred by the respondent herein and similar appeals preferred by the appellant herein were disposed of. It may be mentioned that the Assessing Officer in so far as the present respondent is concerned has assessed his income on substantive basis and in so far as respondent Usman M. Khan is concerned has assessed his income on protective basis. The learned Tribunal in Para-9 of its order was pleased to observe as under.

"In the light of above discussion, we hold that the assessee (G.R.Madhyan) did not indulge in Matka business; that the Matka business belonged to late Shri. Usman Maqbul Khan and accordingly, the A.O. is not justified in making an addition of Rs.1.35 crores and sustained by the CIT(A) at Rs.97.88 lakhs. The addition of Rs.97.86 lakhs is accordingly deleted".

2. The revenue is in appeal against this finding and order.

3. The late Usman M. Khan had preferred appeals before the ITAT for various assessment years . One such appeal was Income Tax Appeal No.627 of 1999 for the Assessment year 1987-88. The Tribunal noted that Income Tax Appeal No.583 of 1999 to 592 of 1999 relating to Assessment year 1987.88 to 1996-97, In the case of Shri.G.R. Madhyan they had held that the assessee (Shri. G.R. Madhyan) did not indulge in Matka business. They further held in the light of the observations in the case of G.R. Madhyan income is to be assessed in the hands of Usman M. Khan on substantive basis and not on protective basis. The appeal therefore, preferred on this ground was dismissed. The revenue preferred appeal before this court against the order dated 26.2.2001 passed in Income Tax Appeal No.330/2001. This court by its order dated 23.7.2004 held that the finding recorded by the Tribunal are concluded on facts and do not give rise to any substantive question of law and accordingly dismissed the appeal in limine. In other words, the finding of fact recorded by the Tribunal that income is to be assessed in hand of Usman M. Khan on substantive basis has been upheld.

4. Once that finding is upheld, in our opinion, we can confirm the finding of fact recorded by the Tribunal in this appeal. As noted earlier the A.O. had earlier assessed the income on substantive basis in the hands of the respondent and on protective basis in the hands of late Usman Maqbool Khan. Considering the finding of fact recorded by the Tribunal which has been upheld in the appeal preferred by the revenue against Usman M. Khan, in our opinion,the questions of law as framed would not arise and consequently, the appeal stands dismissed.

(R.S. MOHITE, J.) (F.I. REBELLO, J.)

×

Similar Ripples

Questions

Court Upholds Tribunal's Decision: Matka Business Income Belongs to Usman M. Khan, Not G.R. Madhyan

Write your CommentSimilar Posts

Generic

- Reportdata/4974.pdf