Court upholds Tribunal's decision on business income for Section 80HHC (of Inco…

Full News

Court upholds Tribunal's decision on business income for Section 80HHC (of Income Tax Act, 1961) deduction

Court upholds Tribunal's decision on business income for Section 80HHC (of Income Tax Act, 1961) deduction

This case is all about a tax dispute between the Commissioner of Income Tax (that's the Revenue) and Premier Polytronics Ltd. (the assessee). The main issue was whether certain types of income should be considered part of the company's business income for calculating a tax deduction under Section 80HHC (of Income Tax Act, 1961). The Income Tax Appellate Tribunal sided with the company, and the High Court agreed, dismissing the Revenue's appeal.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Premier Polytronics Ltd. (High Court of Madras)

T.C. (Appeal) No.247 of 2004

Date: 6th November 2007

Key Takeaways:

1. The court emphasized the importance of considering the nature of a company's business activities when determining what constitutes business income.

2. Income from service charges, lease rentals, and packing and forwarding charges can be considered business income if they're part of the company's regular operations.

3. The decision reinforces the principle that tax authorities need solid evidence to exclude certain incomes from the Section 80HHC (of Income Tax Act, 1961) deduction calculation.

Issue:

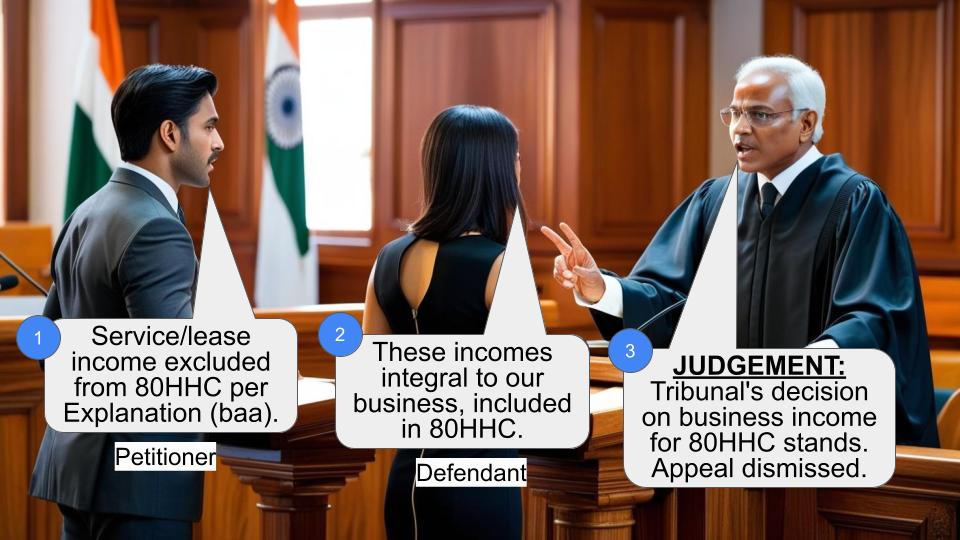

The main question here was: Should service income, lease income, and packing and forwarding collection be considered part of the assessee's business income for calculating the deduction under Section 80HHC (of Income Tax Act, 1961)?

Facts:

1. The case is about the assessment year 1992-93.

2. Premier Polytronics Ltd. (our assessee) was in the business of selling plant and machinery.

3. They also provided maintenance services, had a leasing division, and charged for packing and forwarding.

4. Initially, the Assessing Officer included all these incomes for calculating the Section 80HHC (of Income Tax Act, 1961) deduction.

5. The Commissioner of Income Tax (Appeals) revised this order, saying these incomes should be excluded.

6. The Income Tax Appellate Tribunal disagreed with the Commissioner and ruled in favor of the assessee.

7. The Revenue (that's the tax department) wasn't happy with this and appealed to the High Court.

Arguments:

The Revenue's side:

- They argued that service charges, lease income, and packing and forwarding charges weren't part of the assessee's main business.

- They said these should be excluded under Explanation (baa) to sub-section (4A) of Section 80HHC (of Income Tax Act, 1961).

The Assessee's side:

- They said all these incomes were related to their regular business activities.

- The service charges were from Annual Maintenance Contracts for the machinery they sold.

- The leasing income came from a separate division but was still part of their diversified business.

- The packing and forwarding charges were just reimbursements for expenses they incurred while supplying machinery.

Key Legal Precedents:

1. CIT vs. Bangalore Clothing Co. (2003) 260 ITR 371 (Bom): This case established that you need to look at the nature of the company's activities before excluding income under Explanation (baa).

2. K.R.M. Marine Exports Ltd. vs. Asst. CIT (2007) 288 ITR 151 (Mad): This case clarified that the profit referred to in Section 80HHC (of Income Tax Act, 1961) is specifically export profit, not general profit.

Judgement:

The High Court sided with the assessee and dismissed the Revenue's appeal. Here's why:

1. The Tribunal had already found that these incomes were part of the assessee's regular business operations.

2. The court said that without clear evidence showing otherwise, they couldn't overturn the Tribunal's factual findings in an appeal under Section 260A (of Income Tax Act, 1961).

3. They agreed with the Bombay High Court's approach in the Bangalore Clothing Co. case, which says you need to consider the nature of the company's activities.

FAQs:

1. Q: What's Section 80HHC (of Income Tax Act, 1961) all about?

A: It's a section of the Income Tax Act that provides deductions for profits earned from the export of goods or merchandise.

2. Q: Why was this case important?

A: It clarifies what can be considered business income for the purpose of calculating the Section 80HHC (of Income Tax Act, 1961) deduction, especially for companies with diverse income streams.

3. Q: Does this mean all service charges and lease income will always be considered business income?

A: Not necessarily. The court emphasized that it depends on the nature of the company's activities and how these incomes relate to their main business.

4. Q: What should companies take away from this judgment?

A: Companies should ensure they can demonstrate how different income streams relate to their core business activities, especially when claiming tax deductions.

5. Q: Can the tax department still challenge similar cases in the future?

A: Yes, but they'll need strong evidence to show that certain incomes are not part of the regular business operations.

1. This Tax Case Appeal is filed by the Revenue, raising the following substantial question of law:

" Whether on the facts and in the circumstances of the case the Income Tax Appellate Tribunal was right in setting aside the order of the Commissioner of Income Tax under Section 263 (of Income Tax Act, 1961), holding that while computing the deduction under Section 80 (of Income Tax Act, 1961) HHC in the case of the assessee for the assessment year 1992-93, 90% of the service income, lease income and packing and forwarding collection should be excluded from the profits of the business and the said receipts would not be disqualified under explanation to Section 80 (of Income Tax Act, 1961) HHC (4A)? "

2. The assessment year under consideration is 1992-93. Originally, while computing the relief under Section 80-HHC (of Income Tax Act, 1961), the Assessing Authority did not exclude 90% of the receipts pertaining to the service income, lease income and packing and forwarding collection. However, in exercise of power under Section 263 (of Income Tax Act, 1961), the Commissioner of Income Tax (Appeals) revised the order of assessment. In the process, the Commissioner held that the three items of receipt were not part of receipts from the manufacturing activities to have the character of a business income. Consequently, the Commissioner of Income Tax held that Section 80 (of Income Tax Act, 1961) HHC being an incentive given for actual export business and not over profits from non-export activities, they have to be excluded under the computation of the eligible income in terms of explanation (baa) to sub Section (4A) of Section 80 (of Income Tax Act, 1961) HHC. The Commissioner of Income Tax directed the Assessing Officer to re-compute the assessment under Section 80 (of Income Tax Act, 1961) HHC by excluding 90% of the total receipt of service income, lease income and packing and forwarding collection.

3. Aggrieved by the order of the Commissioner of Income Tax (Appeals), the assessee preferred an appeal before the Income Tax Appellate Tribunal, wherein it was contended that the receipts on service are related to its business activity. It was also contended that the assessee had been selling plant and machinery to different buyers as part of its regular business. The assessee had also entered into Annual Maintenance Contracts with the buyers and charging separate service charges for maintaining such contracts. As far as the leasing income is concerned, the assessee contended that they were carrying separate leasing division as part of the diversified business and the lease rentals were arrived as business income. As far as packing and forwarding collection is concerned, it was contended that it was in the nature of recoupment of such expenditure already incurred by the assessee on behalf of the buyers while supplying the plant and machinery sold by the assessee. In support of its claim, the assessee relied on the decision of the Bombay High Court reported in 260 ITR 371 (CIT Vs. BANGALORE CLOTHING COMPANY) to contend that the Bombay High Court had held that the receipts forming part of the operational income of the assessee could not be excluded under Explanation (baa) to sub Section (4A) of Section 80 (of Income Tax Act, 1961) HHC. Applying the law declared by the Bombay High Court, the Income Tax Appellate Tribunal set aside the order of the Commissioner of Income Tax (Appeals). The Revenue is on appeal challenging the correctness of the order of the Tribunal.

4. Learned counsel appearing for the Revenue submitted that the service charges and packing and forwarding charges did not form part of the business of the assessee and were hit by Explanation (baa) to sub section (4A) of Section 80 (of Income Tax Act, 1961) HHC. In the circumstances, learned counsel seeks the reversal of the order of the Tribunal.

5. A perusal of the order of the Tribunal shows that the assessee had received income on service charges as part of the collections of the business of the assessee company. These claims were against the Annual Maintenance Contracts. The assessee was selling plant and machinery to various buyers and consequently, the Tribunal held that for the smooth conduct of the assessee's business, the assessee had taken their responsibility of providing maintenance services to the buyers; in the process, the assessee had claimed service charges which are nothing but business receipts of the assessee company and that the activity of providing repair maintenance services is incidental and very much part of the assessee's principal business. Ultimately, the Tribunal held that these are part of the business receipts and as such, they cannot be excluded in the computation of the benefits under Section 80 (of Income Tax Act, 1961) HHC. The Tribunal also pointed out that the assessee had expended on the salary, etc., on the Engineer and Technician to discharge their contractual obligation of the Annual Maintenance Contract. As regards the expenses regarding the lease income, the Tribunal found that the the assessee was doing leasing business under a separate division. The assessee claimed depreciation which was also allowed on the plant and machinery deployed by the assessee in its leasing business, and therefore it was a business income. As regards packing and forwarding charges collection, the Tribunal found that it was not an independent income in the hands of the assessee company. In the face of incurring expenditure for packing and forwarding of machineries to various destinations on behalf of its purchasers, the reimbursement of the packing and forwarding charges is very much part of the assessee's business and hence, these are to be taken as business income. Ultimately, the Tribunal found that applying the law laid down by the Bombay High Court reported in 260 ITR 371 (CIT Vs. BANGALORE CLOTHING COMPANY) and considering the nature of business of the assessee, these income are very much part of the business income, which cannot be excluded for application of Explanation (baa) to sub Section (4A) of Section 80 (of Income Tax Act, 1961) HHC.

6. In this connection, the decision of this Court as to the scope of Explanation (baa) to sub section (4A) of Section 80 (of Income Tax Act, 1961) HHC reported in 288 ITR 151 (K.R.M.MARINE EXPORTS LTD. Vs. ASSISTANT COMMISSIONER OF INCOME TAX), to which one of us is a party (K.RAVIRAJA PANDIAN,J.), needs to be referred to. Referring to the decision of the Bombay High Court reported in 260 ITR 371 (CIT Vs. BANGALORE CLOTHING COMPANY), this Court held that when receipts like interest, commission, etc. are included in the business profits as the existing formula distorted the figure of export profits; therefore, in order to clarify the meaning of the business profits for the purpose of Section 80HHC Clause (baa) (of Income Tax Act, 1961) to explain the same was inserted to remove the doubt in calculating export profits. This Court also held that the numerator and denominator showed that they referred to sale proceeds. The numerator and the denominator are required to have a common element which is the sale proceeds. In this background, the profit referred to in Section 80HHC (of Income Tax Act, 1961) is not the general profit, but is the export profit, which had to be calculated and worked out with reference to the other provisions and definitions contained in the Section itself, which sort of exercise had not been done in that case.

7. The Bombay High Court in the decision reported in 260 ITR 371 (CIT Vs. BANGALORE CLOTHING COMPANY), held that unless and until the officer concerned has necessary materials to show the nature of activity of the assessee to qualify for the non-application under Explanation (baa), it is not possible for any authority for that matter to straight away apply the formula to restrict the allowable deduction under Section 80 (of Income Tax Act, 1961) HHC. The Bombay High Court also held that no standard test could be laid down to find out what would constitute operational income. Hence, the Department has to consider the nature of the activity and the business of the assessee and such other test to find out what would be the dominant business of the company and whether receipts like interest, commission, etc., accrue as a part of the main business activity or whether they accrue out of incidental business, and apply such test. In this background, we look at the facts of this assessment.

8. The Tribunal, as a matter of fact, found that the income from the leasing of the company, amount received by way of service charges as well as recoupment of packing and forwarding collection are nothing but forming part of the business income. In the nature of the facts found by the Tribunal, unless and until there are facts otherwise to show the character of the transaction, it is not possible to accept the plea of the Revenue that the transactions does not carry the character of business income. Hence, in the face of the facts recorded by the Tribunal, it is not possible to accept the plea of the Revenue in an appeal filed under Section 260-A (of Income Tax Act, 1961). Consequently, applying the decision reported in 288 ITR 151 (K.R.M.MARINE EXPORTS LTD. Vs. ASSISTANT COMMISSIONER OF INCOME TAX), following the decision of the Bombay High Court reported in 260 ITR 371 (CIT Vs. BANGALORE CLOTHING COMPANY), we do not find any merit in this appeal. Consequently, this Tax Case Appeal is rejected and the order of the Tribunal stands confirmed. No costs.

To:

The Commissioner of Income Tax I

×

Similar Ripples

Questions

Court upholds Tribunal's decision on business income for Section 80HHC (of Income Tax Act, 1961) deduction

Write your CommentSimilar Posts

Generic

- Reportdata/5199.pdf