Court Upholds Trust Registration Without Prior Activities

Full News

Court Upholds Trust Registration Without Prior Activities

Court Upholds Trust Registration Without Prior Activities

This case involves the Principal Commissioner of Income Tax challenging the Income Tax Appellate Tribunal's decision regarding the registration of Shri Nathji Goverdhan Nathji Charitable Trust under Section 12AA (of Income Tax Act, 1961). The High Court dismissed the appeal, affirming that a trust can be registered based on its objects without necessarily demonstrating prior charitable activities.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax vs. Shri Nathji Goverdhan Nathji Charitable Trust (High Court of Calcutta)

ITA 180 of 2018

Date: 28th February 2020

Key Takeaways:

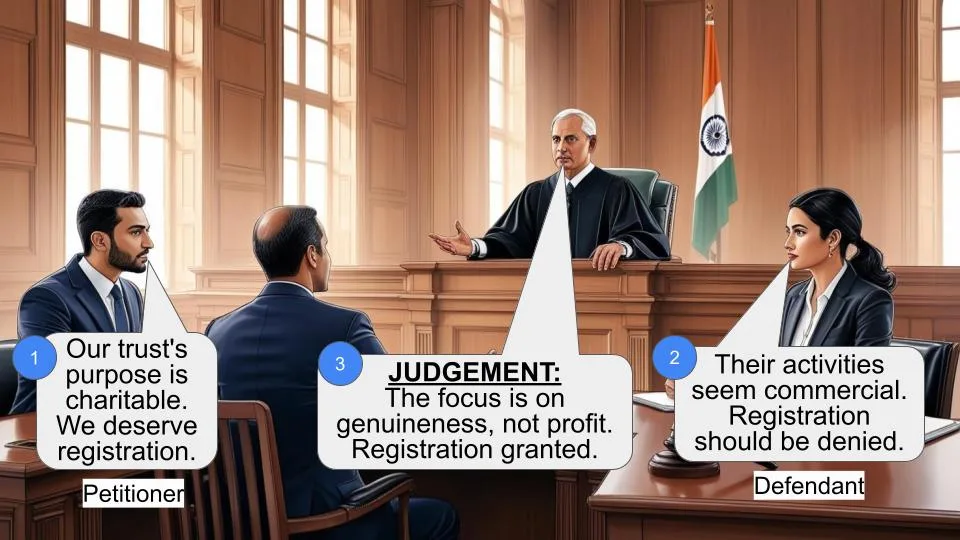

1. A trust can be registered under Section 12AA (of Income Tax Act, 1961) based on the genuineness of its objects, even without prior activities.

2. The Commissioner must consider the trust's constitution, objects, trustees, and proposed activities for registration.

3. If activities are later found non-genuine, registration can be cancelled under Section 12AA(3) (of Income Tax Act, 1961).

4. The court emphasized a purposive interpretation of the law, considering practical realities of trust formation and operation.

Issue:

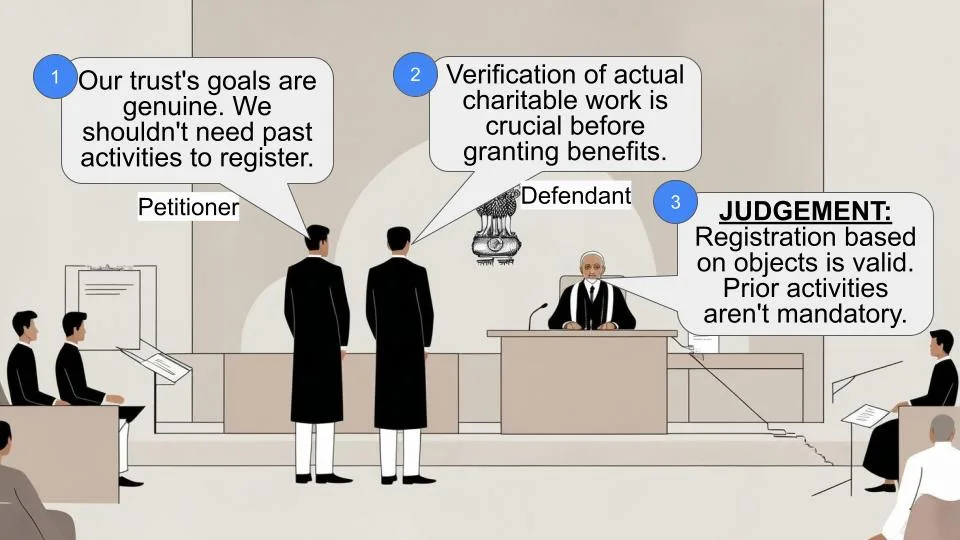

Whether the Income Tax Appellate Tribunal erred in law by interpreting that verification of genuineness of activity is not a condition precedent for granting registration under Section 12AA (of Income Tax Act, 1961)?

Facts:

- Shri Nathji Goverdhan Nathji Charitable Trust applied for registration under Section 12AA (of Income Tax Act, 1961).

- The Principal Commissioner of Income Tax denied registration, likely due to lack of prior charitable activities.

- The Income Tax Appellate Tribunal allowed the trust's appeal and remanded the matter to the Commissioner of Income Tax (Appeals) for reconsideration.

- The Revenue appealed against this order in the High Court.

Arguments:

Revenue's Argument:

- The Commissioner should verify the genuineness of a trust's activities before granting registration under Section 12AA (of Income Tax Act, 1961).

Trust's Argument (implied):

- A newly formed trust should be granted registration based on its objects, even without prior activities.

Key Legal Precedents:

1. Director of Income-Tax (Exemptions) vs. Meenakshi Amma Endowment Trust (2013) 354 ITR 219 (Karnataka):

Held that a newly formed trust can be registered based on its objects without immediate charitable activities.

2. Director of Income Tax vs. Foundation of Ophthalmic and Optometry Research Education Centre (2013) 355 ITR 361 (Delhi):

Affirmed that there's no statutory waiting period for trust registration.

3. Hardayal Charitable and Educational Trust vs. Commissioner of Income-Tax (2013) 355 ITR 534 (Allahabad):

Stated that at the time of registration, the Commissioner is not required to look into activities that haven't commenced.

4. Sree Anjaneya Medical Trust vs. Commissioner of Income Tax (2016) 382 ITR 399 (Kerala):

Emphasized the importance of "genuineness of the trust" as a vital consideration.

5. Self Employers Service Society vs. Commissioner of Income Tax (2001) 247 ITR 18 (Kerala):

Supported rejection of registration when a trust couldn't show any genuine activity for a significant period.

Judgement:

The High Court dismissed the Revenue's appeal, ruling in favor of the assessee (the trust). Key points of the judgment include:

1. The court agreed with the Tribunal's interpretation of Section 12AA (of Income Tax Act, 1961).

2. It emphasized a purposive construction of the statute, considering practical realities of trust formation and operation.

3. The Commissioner should assess the genuineness of the trust's constitution, objects, trustees, and proposed activities for registration.

4. If activities are later found non-genuine, the Commissioner can cancel registration under Section 12AA(3) (of Income Tax Act, 1961).

5. The court found it unrealistic to expect substantial activities before registration, given the tax implications and donor considerations.

FAQs:

Q1: Can a newly formed trust get registered without showing any prior activities?

A1: Yes, a newly formed trust can be registered based on the genuineness of its objects and proposed activities.

Q2: What factors should the Commissioner consider when registering a trust?

A2: The Commissioner should consider the trust's constitution, objects, trustees, and proposed activities to determine their prima facie genuineness.

Q3: What happens if a registered trust's activities are later found to be non-genuine?

A3: The Commissioner has the option to cancel the registration under Section 12AA(3) (of Income Tax Act, 1961).

Q4: Why did the court find it impractical to expect substantial activities before registration?

A4: The court recognized that without registration, a trust would not receive tax benefits or attract donations, making it difficult to carry out substantial activities.

Q5: Does this judgment change how trusts are registered in India?

A5: While it doesn't change the process, it clarifies the interpretation of Section 12AA (of Income Tax Act, 1961), potentially making it easier for newly formed trusts to obtain registration.

On 10th January, 2019 a division bench of this court admitted this appeal to be heard on the following substantial question of law:

“Whether the Income Tax Appellate Tribunal erred in law by misinterpreting Section 12AA (of Income Tax Act, 1961) and came to an erroneous decision that verification of genuineness of activity is not condition precedent for granting registration under Section 12AA (of Income Tax Act, 1961).”

Section 12AA (of Income Tax Act, 1961) provides that the Principal Commissioner or Commissioner of Income Tax shall register a trust on being satisfied about its objects and the genuineness of its activities.

The only question to be decided is whether the trust should show some activities undertaken by it before registration to the Commissioner to satisfy him or is the Commissioner required to be satisfied that the intended activities of the trust after registration are genuine?

In this case, the tribunal proceeded on the basis that the activities of the trust were at the commencement stage and that the registration of the trust was to be made after the Commissioner only satisfied himself that the objects of the trust were charitable. By its impugned order dated 28th March, 2018, the tribunal allowed the appeal of the respondent trust by remanding the matter to the Commissioner of Income Tax (Appeals) to rehear and reconsider the matter on the above observations. The Revenue appeals to us against that order.

Now, let me discuss the authorities on the subject. In Director of Income-Tax (Exemptions) Vs. Meenakshi Amma Endowment Trust reported in (2013) 354 ITR 219 (Karnataka), a division bench of the Karnataka High Court opined as follows:-

“On a perusal of the records we note that the trust was formed on January 23, 2008, and within a period of nine months they had filed an application under section 12A (of Income Tax Act, 1961) for issuance of the registration claiming exemption. The fact that the corpus of the trust is nothing but the contribution of Rs.1,000 by each of the trustees as corpus fund goes to show that the trustees were contributing the funds by themselves in a humble way and were intending to commence charitable activities. It is not even the case of the Revenue that by the time the application of the assessee came to be considered by them, the assessee had collected lots of donations for the activities of the trust. On the other hand, the grievance of the concerned authorities seems to be that there was no activity which could be termed as charitable as per the details furnished by the assessee, therefore, such registration could not be granted. When the trust itself was formed in January, 2008, with the money available with the trust, one cannot expect them to do activity of charity immediately and because of that situation the authority cannot come to a conclusion that the trust was not intending to do any activity of charity. In such a situation the objects of the trust have to be taken into consideration by the authority and the objects of the trust could be read from the trust deed itself. In the subsequent returns filed by the trust, if the Revenue comes across that factually the trust has not conducted any charitable activities, it is always open to the authorities concerned to withdraw the registration already granted or cancel the said registration under section 12AA(3) (of Income Tax Act, 1961).”

In Director of Income Tax Vs. Foundation of Ophthalmic and Optometry Research Education Centre reported in (2013) 355 ITR 361 (Delhi), a division bench of the Delhi High Court relying on the above decision of the Karnataka High Court added its own authority by qualifying the ratio by saying that in case of a newly registered trust the consideration for registration should be its objects. It pronounced the following ratio:-

“Facially, the above provisions would suggest that there are no restrictions of the kind which the Revenue is reading into in this case. In other words, the statute does not prohibit or enjoin the Commissioner from registering a trust solely based on its objects, without any activity, in the case of a newly registered trust. The statute does not prescribe a waiting period, for a trust to qualify itself for registration.”

A division bench of the Allahabad High Court following the above Karnataka High Court decision in Hardayal Charitable and Educational Trust Vs. Commissioner of Income-Tax reported in (2013) 355 ITR 534 (Allahabad) expressed a similar view as follows:-

“The preponderance of the judicial opinion of all the High Courts including this court is that at the time of registration under section 12AA (of Income Tax Act, 1961), which is necessary for claiming exemption under sections 11 (of Income Tax Act, 1961) and 12 of the Act, the Commissioner of Income-tax is not required to look into the activities, where such activities have not or are in the process of its initiation. Where a trust, set up to achieve its objects of establishing educational institution, is in the process of establishing such institutions, and receives donations, the registration under section 12AA (of Income Tax Act, 1961) cannot be refused, on the ground that the trust has not yet commenced the charitable or religious activity. Any enquiry of the nature would amount to putting the cart before the horse. At this stage, only the genuineness of the objects has to be tested and not the activities, which have not commenced. The enquiry of the Commissioner of Income-tax at such preliminary stage should be restricted to the genuineness of the objects and not the activities unless such activities have commenced. The trust or society cannot claim exemption, unless it is registered under section 12AA (of Income Tax Act, 1961) and thus at that such initial stage the test of the genuineness of the activity cannot be a ground on which the registration may be refused.”

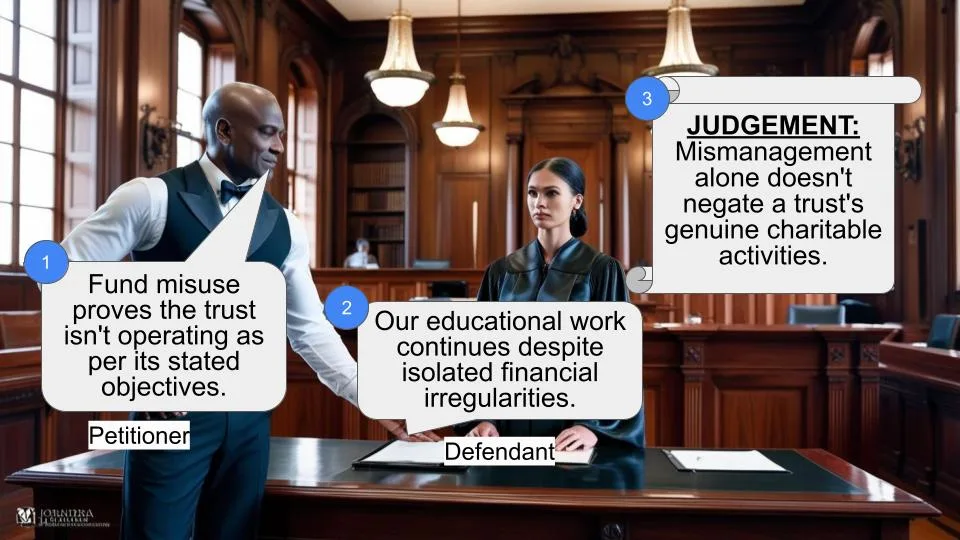

A division bench of the Kerala High Court in Sree Anjaneya Medical Trust Vs. Commissioner of Income Tax reported in (2016) 382 ITR 399 (Kerala) added a new dimension by saying that “the genuineness of the trust” was a vital consideration.

In Self Employers Service Society Vs. Commissioner of Income Tax reported in (2001) 247 ITR 18 (Kerala), a division bench of the Kerala High Court, observing that the trust for a significant period of time had not done any charitable work and could not show any genuine activity supported the decision for rejection of registration.

While we substantially agree with the ratio in the above cases, we cannot help making some observations.

Section 12A(1) (of Income Tax Act, 1961) states that the provisions for tax benefit under Sections 11 (of Income Tax Act, 1961) and 12 would only apply to any trust if the trust is registered under Section 12AA (of Income Tax Act, 1961). Therefore, a trust on registration gets very substantial tax benefits. A trust on formation normally looks towards donors to augment its corpus. The donor also gets corresponding tax benefits, only if the trust is registered. Take for example, the donation referred to in Section 80G(5) (of Income Tax Act, 1961) read with Section 10(23C)(v) (of Income Tax Act, 1961). Any prudent trustee would not carry out the substantial activities of the trust for a length of time and then apply for registration under Section 12AA (of Income Tax Act, 1961), for the simple reason that the income of the trust would be chargeable to income tax during that period. On the other hand, a donor would be reluctant to make donations to the trust unless it was registered. In those circumstances, it is a little unrealistic to think of two situations.

First, on creation of the trust the trustees apply for registration under Section 12AA (of Income Tax Act, 1961). In that case, they would have to demonstrate the genuineness of the objects of the trust, only, before the Commissioner. Secondly, the other situation where the trustees carry on activities for sometime and then apply for registration. In that case, the genuineness of the objects as well as the genuineness of its activities have to be proved to the Commissioner. In the second situation, practically speaking, any activity of the trust carried out without registration and without any tax benefit would likely to be insignificant.

Every word in a statute has meaning and application. The legislature does not waste words. Nor does it indulge in surplussage. Hence, every word in Section 12AA (of Income Tax Act, 1961) has to be given its meaning and effect. In my opinion, when the statute refers to the objects of the trust and the genuineness of its activities to be investigated by the Commissioner, the words have to be given a proper and purposive construction. The Commissioner has to see that the constitution of the trust, its objects, its trustees and proposed activities are prima facie genuine. On that basis he has to consider registering the trust.

If the activities are found not to be genuine at a later point of time, he always has the option of cancelling its registration under Section 12AA(3) (of Income Tax Act, 1961) of the said Act.

I am of the opinion that the tribunal has appreciated the law correctly. The question in this appeal is answered in the negative, against the Revenue and for the assessee.

The appeal (ITA 180 of 2018) is accordingly dismissed.

(I. P. MUKERJI, J.)

PROTIK PRAKASH BANERJEE, J.:

I have had the opportunity to go through the judgment of my Learned Brother and I concur fully with the same. However, I wish to add a few words to show how unrealistic the interpretation offered by the Revenue is in real life.

No trust can be created without registration under the Indian Registration Act. Section 12A (of Income Tax Act, 1961)/12AA of the Income Tax Act, 1961 does not refer to this registration. The registration referred to in Section 12AA (of Income Tax Act, 1961) is done by the Principal Commissioner of Income Tax who on being satisfied about the objects and genuineness of the activities of trust registers it and by this act of registration, permits people to donate funds to it to claim certain deductions.

If a trust registered under Indian Trust Act and Registration Act as a charitable trust, does not get itself registered before the Principal Commissioner of Income Tax it loses certain benefits both for itself and for those who donate to it. Since by definition a charitable trust is not one which makes profits and if we accept the interpretation of the Revenue that first the activities of the trust must commence and its genuineness ascertained before the Principal Commissioner registers it, we would be asking the trust to carry on activities perhaps at a loss to the corpus or by compromising on the quality of such activities if the expenditure is done from the interest on the corpus because no one will donate money to a trust knowing that it is not tax deductable. In such view of the matter, the interpretation offered by the Revenue appears to be one which perhaps defeats Section 12A (of Income Tax Act, 1961)/12AA of the said Act of 1961 and its very purpose and, therefore, also it cannot be accepted. As a result, I fully concur with the findings reached by my Learned Brother, agree with His Lordship’s reasoning and also answer the question raised in the appeal in negative against the Revenue and for the assessee.

Certified photocopy of this order, if applied for, be supplied to the parties upon compliance with all requisite formalities.

(PROTIK PRAKASH BANERJEE, J.)

×

Similar Ripples

Questions

Court Upholds Trust Registration Without Prior Activities

Write your CommentSimilar Posts

Generic

- Reportdata/6017.pdf