Trust's Registration Upheld: Misappropriation Not Grounds for Cancellation

Full News

Trust's Registration Upheld: Misappropriation Not Grounds for Cancellation

Trust's Registration Upheld: Misappropriation Not Grounds for Cancellation

This case involves the Commissioner of Income Tax (CIT) attempting to cancel the registration of an educational trust under Section 12A (of Income Tax Act, 1961). The CIT's decision was overturned by the Tribunal, and the High Court upheld the Tribunal's order, ruling that misappropriation of funds by trustees is not grounds for cancellation of registration if the trust's activities remain genuine and aligned with its objectives.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs Islamic Academy of Education (High Court of Karnataka)

ITA No.805 of 2008

Date: 09 September 2014

Key Takeaways:

1. Registration cancellation of a trust is only permissible if activities are not genuine or not in line with trust objectives.

2. Misappropriation of funds by trustees doesn't justify cancellation of registration.

3. Tax authorities can deny benefits under Section 11 (of Income Tax Act, 1961) for misappropriation without cancelling registration.

4. The court emphasized the importance of focusing on the trust's core activities rather than trustees' misconduct.

Issue:

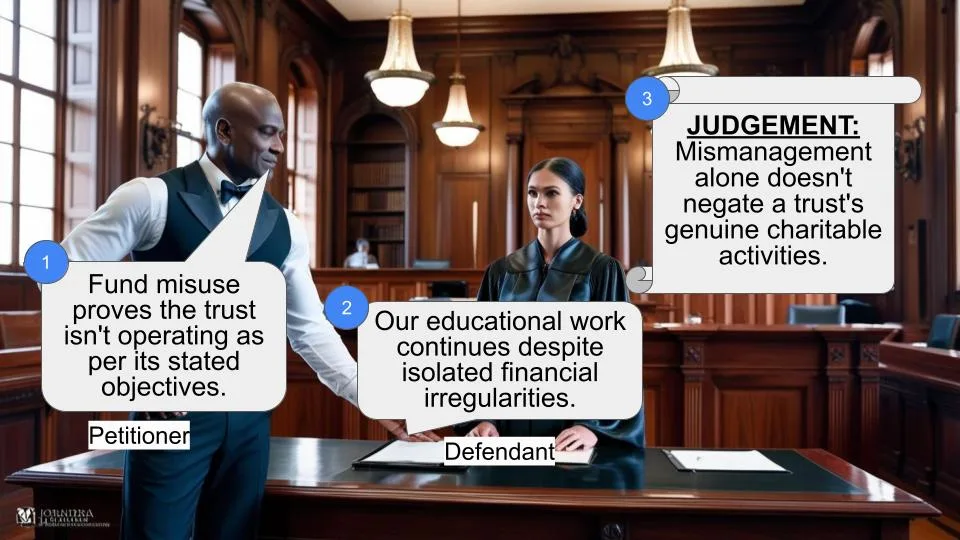

Can the registration of a trust under Section 12A (of Income Tax Act, 1961) be cancelled based on allegations of fund misappropriation by trustees, even if the trust's core activities remain genuine and aligned with its objectives?

Facts:

1. The Islamic Academy of Education was registered under Section 12A (of Income Tax Act, 1961) in 1992 .

2. The trust established and operates educational institutions, including a medical college .

3. The CIT cancelled the trust's registration citing reasons such as improper book-keeping, unaccounted donations, and alleged misappropriation of funds .

4. A search under Section 132 (of Income Tax Act, 1961) revealed undisclosed cash and admission fees .

5. The trust filed returns declaring additional income of ₹13,23,52,850/- .

Arguments:

Revenue's Arguments:

1. Cash was found in the Chairman's residence and offered for tax by the trust.

2. Bogus entries and advances to family members were discovered.

3. The trust's activities were not carried out in accordance with the law and Income Tax Act provisions.

Assessee's Arguments:

1. The genuineness of the trust and its educational activities were not disputed .

2. Violations in accounting practices don't justify cancellation of registration .

3. Tax benefits under Section 11 (of Income Tax Act, 1961) can be denied without cancelling registration .

Key Legal Precedents:

The judgment refers to Section 12AA(3) (of Income Tax Act, 1961), introduced by the Finance (No.2) Act of 2004, effective from 1.10.2004 . This section specifies the conditions under which a trust's registration can be cancelled.

Judgement:

1. The High Court upheld the Tribunal's decision, ruling in favor of the assessee (Islamic Academy of Education) .

2. The court emphasized that registration cancellation is only permissible under two circumstances:

a) When the trust's activities are not genuine

b) When activities are not carried out in accordance with the trust's objectives.

3. The court found that the trust's educational activities were ongoing and genuine.

4. Misappropriation of funds by trustees is not grounds for cancellation of registration.

5. The court suggested that tax authorities can deny benefits under Section 11 (of Income Tax Act, 1961) for misappropriation without cancelling registration.

FAQs:

Q1: Does this judgment mean trustees can misappropriate funds without consequences?

A1: No, the judgment suggests that while registration cancellation isn't appropriate, tax benefits can be denied and other legal actions may be taken.

Q2: What are the only grounds for cancelling a trust's registration under the Income Tax Act?

A2: Registration can be cancelled only if the trust's activities are not genuine or not carried out in accordance with its objectives.

Q3: Can tax authorities take any action against trusts misusing funds?

A3: Yes, they can deny benefits under Section 11 (of Income Tax Act, 1961) and pursue other legal remedies without cancelling registration.

Q4: Does this judgment apply to all types of trusts?

A4: While the case specifically dealt with an educational trust, the principles could potentially apply to other types of trusts registered under the Income Tax Act.

Q5: What should trusts learn from this case?

A5: Trusts should ensure their core activities remain genuine and aligned with their objectives, while also maintaining proper financial records to avoid scrutiny.

1. The revenue has preferred this appeal against the order passed by the Commissioner of Income Tax cancelling registration.

2. The assessee was registered under section 12A (of Income Tax Act, 1961) by the CIT, Karnataka-III, Bangalore, vide certificate dated 4.6.1992. Recognition under section 80G (of Income Tax Act, 1961) was also granted to the assessee vide certificate dated 3.11.1992 by the CIT, Karnataka-III, Bangalore. The recognition granted under section 80G (of Income Tax Act, 1961) was valid from 19.10.1992 to 31.3.1994 and renewal of recognition under section 80G (of Income Tax Act, 1961) was granted vide certificate dated 1.3.2005. The renewal of recognition was valid from 15.6.2004 to 31.3.2006. Registration under section 12A (of Income Tax Act, 1961) and recognition under section 80G (of Income Tax Act, 1961) were withdrawn with effect from 1.4.1996. The reasons for such withdrawal are:

i) The institution has not maintained proper books of account.

ii) Donations received have been kept outside the books of account.

iii) The assessee has accounted only the fees fixed by the University. The assessee is collecting fees over and above the fees fixed by the University and this amount has not been recorded in the cash book and it has introduced this cash to the bank as and when the need arises. The assessee has issued receipts for the sums received over and above the fees fixed by the University.

(iv) Three of the Trustees of the assessee are also the Directors/Chairman in Yenepoya Institute of Medical Science Research Pvt. Ltd., (YIMSRPL), a private limited company. The assessee has invested 20 lakhs in ordinary shares of YIMSRPL during the previous year relevant to assessment year 1995-96 and continued to remain so invested up to 31.3.2005. The assessee is paying huge rent to YIMSRPL and also given huge deposit of 225 lakhs which was claimed as rent deposit.

v) Search u/s.132 (of Income Tax Act, 1961) was conducted on 21.9.2005 in the office premises of the institute as well as the residential premises of the three of the trustees. Cash of `.74 lakhs was found in the residential premises of Shri.Y.Abdullah Kunhi and the same was offered to tax. Fees for admission reported to have been collected much higher than what was recorded in the books and that the actual amount of fees collected has been suppressed. The assessee has admitted that the contract payment of `.350 lakhs paid to M/s.Horizon Construction Co., shown as creditor in the balance sheet, was only bogus and the same was offered for taxation.

(vi) The assessee has filed returns u/s.153A(a) (of Income Tax Act, 1961) declaring additional income of 13,23,52,850/-.

3. A show cause notice dated 27.11.2006 was issued to the assessee calling for reasons as to why registration granted under section 12A (of Income Tax Act, 1961) and recognition granted under section 80G (of Income Tax Act, 1961) should not be withdrawn. A detailed reply was filed. Not being satisfied with the reply, the registration granted under section 12A (of Income Tax Act, 1961) and the recognition under section 80G (of Income Tax Act, 1961) was withdrawn. Aggrieved by the said order, the assessee preferred an appeal before the Tribunal. The Tribunal held that at the time of considering cancellation of registration of Trust already granted, what is mainly to be seen is, whether the activities of the Trust or Institution are not genuine or are not being carried out in accordance with the objects of the Trust or Institution. There is nothing on record to show that the activities are not being carried out in accordance with the objects of the Trust i.e., imparting education. Admittedly, the Trust is carrying on the object of the Trust namely imparting of education. The Trust is not sham or bogus. It is nobody’s case that Trust is not in existence at all or that there is no activity of imparting education and therefore, the Tribunal has set aside the order passed by the Commissioner of Income Tax and restored the registration. Aggrieved by the said order, the revenue is before this Court.

4. The appeal was admitted to consider the following substantial questions of law:

Whether the Tribunal was correct in holding that the registration granted u/s. 12A (of Income Tax Act, 1961) had been incorrectly cancelled u/s. 12AA(3) (of Income Tax Act, 1961) by the Commissioner despite being satisfied based on material detected in the course of search that the activity of the trust was not genuine and was not being carried out in accordance with the objects of the trust?

5. The learned counsel for the revenue assailing the impugned order contended that the material on record discloses that cash was found in the residential premises of the Chairman which was offered to tax by the Trust. A sum of 3.5 Crores is admitted to be a bogus entry and offered to tax. Advances are made to the family members of the Trust out of the Trust fund which are kept outside the accounts and reflected in the coded words. The activities of the Trust are not carried out in accordance with law and contrary to the provisions of the Income Tax Act. Therefore, he submits that a case for cancellation is made out and the Tribunal erroneously set-aside the CIT order.

6. Per contra, learned counsel appearing for the assessee submitted that when once the genuineness of the Trust is not disputed and when the object of the Trust namely imparting education has been carried on uninterruptedly, a case for cancellation of the Trust is not made out. If there are violations, such as not accounting the money received which was found in the possession of the Trustees, bogus entries in the accounts and payments made to the members of the family which are recorded in code numbers, the benefit under section 11 (of Income Tax Act, 1961) need not be extended and such amounts should be taxed. But that is not a justification for cancellation of registration of the Trust.

7. Section 12AA (of Income Tax Act, 1961) provides for procedure for cancellation of registration of the Trust or Institution by the Commissioner of Income Tax. The power of cancellation of registration flows from the power to register. However, there has been unnecessary litigation on this issue. Under what circumstances, the registration of a Trust or Institution granted under section 12A (of Income Tax Act, 1961) could be cancelled by the Commissioner of Income Tax was the subject matter of various interpretation by the various High Courts. In order to avoid such unnecessary litigations, the Parliament introduced sub-section (3) to section 12AA (of Income Tax Act, 1961) by Finance (No.2) Act of 2004 with effect from 1.10.2004 which reads as under:

“Section 12AA(3) (of Income Tax Act, 1961): Where a trust or an institution has been granted registration under clause (b) of sub-section (1) [or has obtained registration at any time under section 12A (of Income Tax Act, 1961) [as it stood before its amendment by the Finance (No.2) Act, 1996 (33 of 1996) and subsequently the Commissioner is satisfied that the activities of such trust or institution are not genuine or are not being carried out in accordance with the objects of the trust or institution, as the case may be, he shall pass an order in writing cancelling the registration of such trust or institution:

Provided that no order under this sub-section shall be passed unless such trust or institution has been given a reasonable opportunity of being heard.]”

As is clear from the circular No.5 of 2005 dated 15.7.2005 issued by the Central Board of Direct Taxes, the aforesaid section was amended so as to specifically provide that if the Commissioner of Income Tax is satisfied that the activities of any Trust or Institution are not genuine or are not being carried out in accordance with the objects of the Trust or Institution, he shall, after giving reasonable opportunity of being heard to the concerned Trust or Institution, pass an order in writing cancelling the registration granted under the said section. Therefore, in view of the aforesaid express provision, registration granted to a Trust could be cancelled under two circumstances namely,

(1) When the activities of the Trust or Institution are not genuine; and

(2) The activities of the Trust or Institution are not being carried out in accordance with the objects of the Trust or Institution.

Only if the Commissioner is satisfied that any one of these conditions exists, then he shall pass an order in writing cancelling the registration of such Trust or Institution. Therefore what follows is, except the aforesaid two grounds and on no other ground, an order cancelling registration of the Trust could be passed.

8. In the instant case, the material on record shows that the Trust has established educational institution and imparting medical education. Every year, students are admitted. Huge investment is made for construction of buildings for housing the college, hostel and to provide other facilities to the students who are studying in the College. The College is recognized by the Medical Council of India, State of Karnataka and all other statutory authorities. Therefore, it cannot be said that the Trust is not genuine. Admittedly, the students are being admitted every year. Students are studying in all courses. Thus the object of the constitution of the Trust namely imparting of education is going on uninterruptedly. Therefore, it cannot be said that the activities of the Trust are not being carried out in accordance with the objects of the Trust. When the aforesaid two conditions are fully satisfied, on the ground that the trustees are misappropriating the funds of the Trust the registration of the Trust cannot be cancelled. If the trustees are misappropriating the funds, if they are maintaining false accounts, it is open to the authorities to deny the benefit under section 11 (of Income Tax Act, 1961), but that is not a ground for cancelation of registration itself. That is precisely what the Tribunal has held.

Therefore, the substantial question of law is answered in favour of the assessee and against the revenue. There is no merit in this appeal.

Accordingly, the appeal is dismissed.

Sd/-

JUDGE

Sd/-

JUDGE

×

Similar Ripples

Questions

Trust's Registration Upheld: Misappropriation Not Grounds for Cancellation

Write your CommentSimilar Posts

Generic

- Reportdata/4627.pdf