Court Upholds Valuation Method in Property Tax Dispute

Full News

Court Upholds Valuation Method in Property Tax Dispute

Court Upholds Valuation Method in Property Tax Dispute

This case involves a dispute between Smt. Kavita Khandelwal (the assessee) and the Commissioner of Income Tax regarding the valuation method used to determine the fair market value of certain properties for tax purposes. The court ultimately ruled in favor of the Revenue department, upholding the Tribunal's decision to use the capitalization method for determining the property value as of January 1, 1964.

Get the full picture - access the original judgement of the court order here

Case Name:

Smt. Kavita Khandelwal Vs Commissioner of Income Tax (High Court of Delhi)

ITR No. 112/1988

Date: 18th January 2008

Key Takeaways:

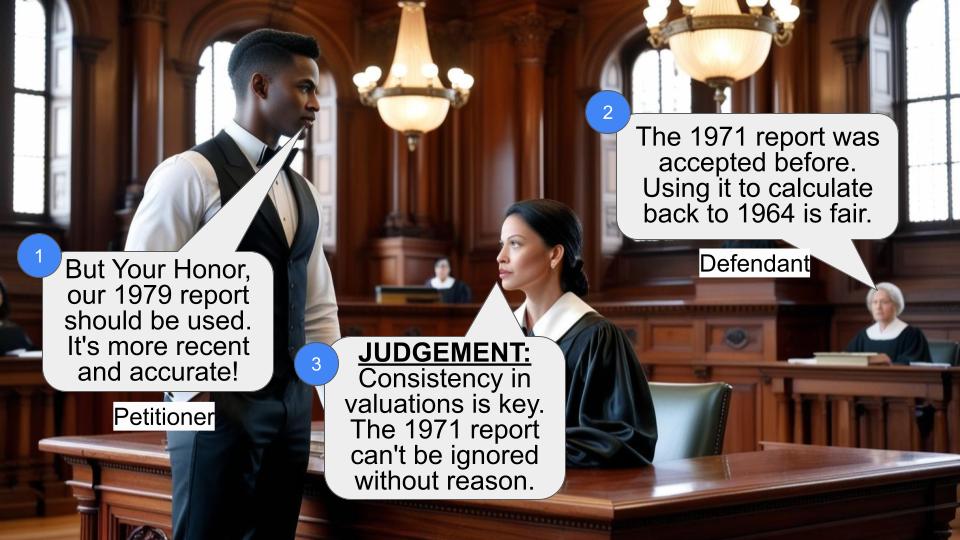

1. The court emphasized the importance of consistency in property valuations.

2. Earlier accepted valuations can be relevant for determining subsequent property values.

3. The capitalization method was deemed appropriate for determining property value in this case.

4. The court highlighted the significance of presenting evidence at the appropriate stage of proceedings.

Issue:

Whether the Income Tax Appellate Tribunal erred in holding that the value of the properties as on January 1, 1964, should be determined using the capitalization method?

Facts:

1. The assessee acquired two plots of land (No. 1 and No. 3) through partial partition of a Hindu Undivided Family (HUF) during the assessment year 1978-79.

2. The properties were later sold by the assessee.

3. For capital gains computation, the assessee claimed costs of acquisition as of January 1, 1964, based on a valuation report dated March 30, 1979.

4. The Income Tax Officer noticed that the same registered valuer had previously valued these properties on May 31, 1971, which was accepted by the department for the assessment year 1971-72.

5. The Income Tax Officer used the 1971 valuation report to compute the property value as of January 1, 1964.

Arguments:

Assessee's argument:

- The earlier valuation report (May 31, 1971) should be disregarded entirely.

- The later valuation report (March 30, 1979) should be used to determine the cost of acquisition.

Revenue's argument:

- The earlier valuation report was previously accepted and utilized by both the assessee and the Revenue.

- There was no valid reason to ignore the earlier report completely.

- The Income Tax Officer's computation based on the 1971 report was reasonable and justified.

Key Legal Precedents:

The judgment doesn't explicitly mention any specific legal precedents. However, it relies on the principle of consistency in valuations and the acceptance of previously submitted evidence.

Judgment:

1. The court ruled in favor of the Revenue department.

2. It held that the Tribunal did not err in deciding that the value of the properties as on January 1, 1964, should be determined using the capitalization method.

3. The court found no reason to disregard the earlier valuation report from 1971, which had been accepted by both parties previously.

4. The Income Tax Officer's method of working backwards from the 1971 valuation to determine the 1964 value was deemed reasonable.

5. The court noted that there was no evidence of the property being occupied by tenants, which could have affected the valuation method.

FAQs:

Q1: Why did the court favor the earlier valuation report?

A2: The court favored the earlier valuation report (1971) because it had been previously accepted and utilized by both the assessee and the Revenue department. There was no compelling reason provided to disregard this report entirely.

Q2: What is the capitalization method mentioned in the judgment?

A2: The capitalization method is a way of valuing property based on its potential income. In this case, it was deemed appropriate for determining the property's value as of January 1, 1964.

Q3: Why was the assessee's argument to use the 1979 valuation report rejected?

A3: The assessee's argument was rejected because they didn't provide any valid reason for completely disregarding the earlier 1971 report, which had been previously accepted and used for tax purposes.

Q4: What role did the lack of evidence about tenants play in the decision?

A4: The court noted that there was no evidence of tenants occupying the property. This lack of evidence supported the use of the capitalization method for valuation, as rental income wasn't a factor to consider.

Q5: What lesson can be learned from this case about property valuations for tax purposes?

A5: This case highlights the importance of consistency in property valuations for tax purposes. Once a valuation method or report has been accepted by both the taxpayer and the tax authorities, it can be difficult to completely disregard it in future assessments without strong justification.

1. The Income Tax Appellate Tribunal (Delhi Bench “E” Delhi) (in short as 'Tribunal') has referred the following question under Section 256(1) (of Income Tax Act, 1961) (in short as 'Act') for opinion of this Court:-

“Whether on the facts and in the circumstances of the case, the Income Tax Appellate Tribunal erred in not holding that the value of the properties as on 1st January, 1964 be taken by capitalisation method?”

2. The brief facts of the present case are that the Assessee who is an individual, acquired plot No.1 of 281 Sq.Yds and the well and another plot No.3 of 229 Sq. Yds. containing an old house of 695 Sq.ft. in partial partition of Sh.D.P.Aggarwal & Family (HUF) during the assessment year 1978-79. The said properties appear to have been sold by the Assessee.

The Income Tax Officer scrutinised the computation of capital gains filed by the Assessee. The Assessee claimed costs of acquisition of the property as on 1st January, 1964 at Rs.26,780/- for plot No.1 and well and at Rs.33,710/- for plot No.3 and the old house. The cost of acquisition was shown on the basis of the valuation report of Sh.Dinesh Krishna, registered valuer dated 30th March, 1979. It was noticed by the Income Tax Officer that for the assessment year 1971- 72, the same registered valuer has valued these very properties along with others vide valuation report dated 31st May, 1971. The land was valued at Rs.4 per Sq.ft. and the old house also at Rs. 4 per Sq.ft. The value in the case of HUF for assessment year 1971-72 declared on the basis of the said report of the registered valuer was accepted by the Department. Against this background, the Assessee was given an opportunity to explain this discrepancy. However, no explanation was given by the Assessee and under these circumstances, the Income Tax Officer computed the value of the property on 1stJanuary, 1964 taking the valuation report of the valuer dated 31st May, 1971. In 1971, the land was valued at Rs. 4 per Sq.ft. and the old house was valued at Rs. 4 per Sq.ft. or Rs.36 per Sq.Yd. Taking into account the appreciation in the value of the land from 1964 to 1971, the Income Tax Officer took the value of amount as on 1st January,1964 at Rs.20 per Sq.Yd. and the value of the old house at Rs.36 per Sq.Yd as on 1st January, 1964. Thus the capital gain was determined by the Income Tax officer on the basis of the cost of acquisition.

3. The Assessee contested the decision of the Income Tax Officer before the Assistant Commissioner of Income Tax. The Assistant Commissioner of Income Tax agreeing with the reasoning of Income Tax Officer, refused to interfere.

4. Thereafter, the matter was brought before the Tribunal by the Assessee and the Tribunal dismissed the appeal filed by the Assessee and thus, this reference has been made to this Court.

5. In the present case, the same registered valuer has valued the same properties twice, that is, first on 31st May, 1971 and subsequently on 30th March, 1979. The Assessee's case before the lower authorities was that the registered valuer's earlier report should be given a total go-by. However, the Assessee has not given any reason as to how it can be done.

6. With respect to these properties, the report of the registered valuer dated 31st May, 1971 was utilised by the Assessee and such utilisation was accepted by the Revenue. Against this background, it is not clear as to how for determining the costs of the property on 1 stJanuary, 1964, the first report of the registered valuer could not be relevant. No reason has been shown that the earlier report should be ignored altogether.

7. As per findings of the Tribunal, the Income Tax Officer had worked out the cost of acquisition relying upon the Assessee's own evidence. There is no evidence that the house property of plot No.3 was being occupied by any tenant on rent. Further, as per observation of the Tribunal, certain pages regarding rent are there in the paper book but the same were not considered as the same were not placed before the lower authorities.

8. Under these circumstances, we have no hesitation in holding that the Tribunal has not erred in holding that the value of the properties as on 1st January, 1964 be taken by capitalisation method.

9. Under these circumstances, we answer the question referred to us, in the negative, that is, in favour of the Revenue and against the Assessee.

10. The reference is disposed of accordingly.

(V. B. GUPTA)

JUDGE

(MADAN B. LOKUR)

JUDGE

January 18, 2008

×

Similar Ripples

Questions

Court Upholds Valuation Method in Property Tax Dispute

Write your CommentSimilar Posts

Generic

- Reportdata/4986.pdf