Tenants' Rights Upheld: Court Quashes Notice Under Income Tax Act

Full News

Tenants' Rights Upheld: Court Quashes Notice Under Income Tax Act

Tenants' Rights Upheld: Court Quashes Notice Under Income Tax Act

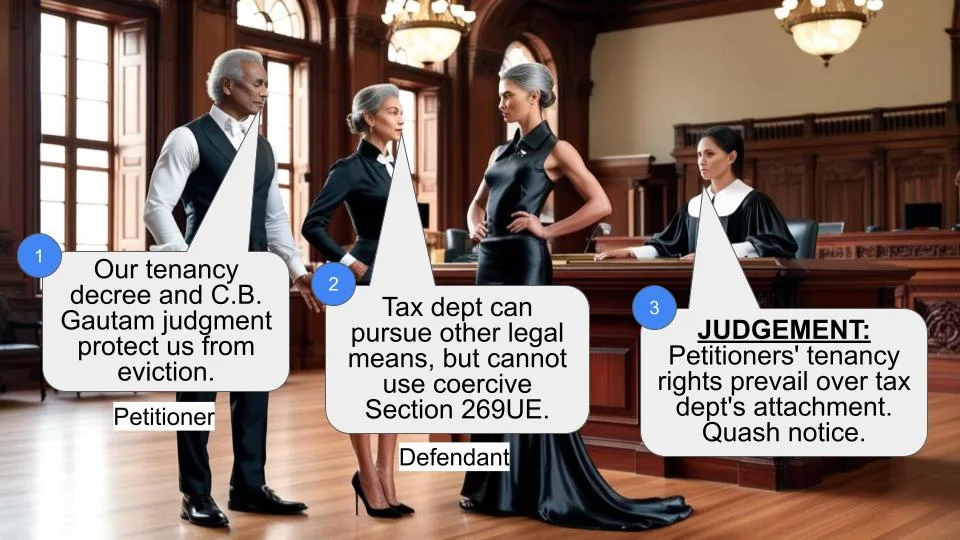

This case involves petitioners claiming tenancy rights in a flat, challenging a notice served under Section 269UE (of Income Tax Act, 1961). The court ruled in favor of the petitioners, stating that the notice was without jurisdiction, considering their established tenancy and a previous court decree in their favor.

Get the full picture - access the original judgement of the court order here

Case Name:

C.B. Methodex Systems (P) Ltd. & Ors. Vs Union of India & Ors. (High Court of Bombay)

Writ Petition No.2542 of 1992

Date: 8th January 2008

Key Takeaways:

1. The court upheld tenants' rights even in cases of property acquisition by the government.

2. Previous court orders (like the Small Causes Court decree) carry significant weight in such disputes.

3. The judgment in C.B. Gautam vs. Union of India & Ors. was applied, emphasizing the protection of existing encumbrances on properties.

Issue:

Could the respondents (government) invoke powers under Section 269UE(2) (of Income Tax Act, 1961) to direct the petitioners (claiming tenancy rights) to vacate the premises, given the existing court decree and tenancy claim?

Facts:

1. The petitioners claimed tenancy rights in Flat No. 54-A, "Mira-Mar" building, Napean Sea Road, Mumbai.

2. They had a leave and license agreement from November 28, 1969, with Mrs. Gopibai Gopaldas.

3. The petitioners filed a suit (R.A.E. & E. Suit No. 80/490 of 1976) against their former employee, Ravindra Sahai, who occupied the flat and claimed ownership.

4. The Small Causes Court decreed in favor of the petitioners on March 4, 1991.

5. Despite this, the government attempted to auction the property and later served a notice under Section 269UE (of Income Tax Act, 1961).

6. The petitioners were eventually put in possession of the flat by court order.

Arguments:

Petitioners:

- They have established tenancy rights and a court decree in their favor.

- The notice under Section 269UE (of Income Tax Act, 1961) is without jurisdiction due to their existing rights.

- The judgment in C.B. Gautam vs. Union of India & Ors. protects their rights as tenants.

Respondents:

- The order under Section 269UD (of Income Tax Act, 1961) supersedes other court orders.

- The C.B. Gautam judgment is prospective and doesn't affect orders passed before November 17, 1992.

Key Legal Precedents:

1. C.B. Gautam vs. Union of India & Ors. (1993) 1 SCC 78:

This judgment struck down the phrase "free from all encumbrances" in Section 269UE(1) (of Income Tax Act, 1961), protecting existing encumbrances and leasehold interests.

Judgement:

The court ruled in favor of the petitioners, stating that:

1. The notice served under Section 269UE (of Income Tax Act, 1961) was without jurisdiction.

2. The judgment in C.B. Gautam applies to this case.

3. The petition was allowed, quashing the notice dated November 11, 1992, and the order dated October 30, 1991.

4. The respondents can take other legal steps but cannot use coercive processes under Section 269UE (of Income Tax Act, 1961) for recovery of possession.

FAQs:

Q1: What was the main issue in this case?

A1: The main issue was whether the government could use Section 269UE (of Income Tax Act, 1961) to evict tenants who had a court decree in their favor.

Q2: How did the C.B. Gautam judgment affect this case?

A2: The C.B. Gautam judgment protected existing encumbrances on properties, which supported the petitioners' claim to tenancy rights.

Q3: Does this judgment mean the government can never acquire such properties?

A3: No, the judgment clarifies that the government can take other legal steps, but cannot use coercive processes under Section 269UE (of Income Tax Act, 1961) in such cases.

Q4: What's the significance of the Small Causes Court decree in this case?

A4: The decree established the petitioners' rights as tenants, which the High Court considered crucial in its decision.

Q5: Does this judgment apply to all similar cases?

A5: While it sets a precedent, each case would be judged on its own merits. However, it emphasizes the importance of existing tenancy rights and court orders in such disputes.

According to the petitioners by an Agreement of 28th November, 1969 executed with Mrs. Gopibai Gopaldas they took on leave and licence basis Flat No.54-A on the 5th Floor of the building "Mira-Mar" at Napean Sea Road, Mumbai. One Shri Ravindra Sahai was in the employment of petitioner No.2 and he was allowed to occupy the said flat. It is the petitioners case that considering the amendment to the Bombay Rent Act giving protection to licensees they became protected tenants. Petitioner No.1 from 1995 onwards was paying the rent/compensation of the flat to the landlady. Their employee Ravindra Sahai resigned from the employment on 5th March, 1995. Though the employee was called upon to vacate the flat he chose not to vacate. The petitioners, therefore, filed R.A.E. & E. Suit No.80/490 of 1976 against Ravindra Sahai in the Court of Small Causes for recovery of possession of the flat along with arrears of compensation from 1st May, 1975 till the date of filing of the suit. Ravindra Sahai on 3rd August, 1976 filed written statement and claimed ownership of the suit premises. The petitioners then have averred that the petitioner No.1 was incorporated to take over the entire assets and liabilities of the petitioner No.2. Issues were framed by the Court of Small Causes. One of the issues was whether Ravindra Sahai was the owner of the premises and whether he had purchased the flat from the original landlady and whether he was liable to hand over possession of the plaintiffs.

According to the petitioners the suit was decreed exparte against Ravindra Sahai on 4th March, 1991.

. They made various attempts to execute the decree, but having failed to do so applied to the Court of Small Causes for braking open the lock in execution of the decree. The Court on receipt of the application which was numbered as Misc. Notice No.242 of 1991 Amongst the respondents was the Union of India. The respondents appeared through their representative and sought time to file affidavit. Thereafter the respondents remained absent in the said proceedings. On 13th December, 1991 as the respondents remained absent an order was passed for executing the decree by breaking open the lock, if necessary.

2. It is the petitioners’ case that an advertisement appeared in the Times of India on 24th July, 1991 putting up for sale various properties which included the flat which was the subject matter of the proceedings before the Small Causes Court. The petitioners addressed an Advocate’s letter dated 21st August, 1991 pointing out as to how the advertisement could be given when there was ad-interim order of injunction issued by the Small Causes Court at Bombay and which was operative. They received a reply on 29th August, 1991 stating that at the time of auction on 22nd August, 1991 an announcement was made indicating to all the parties who attended the auction that the petitioner No.2 has moved the Small Causes Court at Bombay praying for restoration of their tenancy and the Court of Small Causes at Bombay has decreed the said suit in favour of the Petitioner No.2.

3. Inspite of the order of 13th December, 1991 the respondents did not hand over possession of the suit premises to the petitioners, but instead on 28th October, 1991 purported to hand over the possession of the flat to the auction purchaser. On 23rd January, 1991 the Court of Small Causes passed an order to break open the lock and put the petitioners in possession. Accordingly the petitioners were put in possession. The auction purchaser according to the petitioners broke open the lock of the flat illegally, consequent to which a Criminal Complaint came to be filed. The auction purchaser one Mr. Shah field a Writ Petition No.1870 of 1992 before this Court. On 6th September, 1992 an order came to be passed by this Court setting aside the auction sale held on 28th October, 1991 as it was held in defiance of the prohibitory order passed by the Small Causes Court and a direction was issued to refund to the auction purchaser the purchase price with interest at 18% per annum from 26th November, 1991. According to the petitioners the Society accepted the petitioners possession and the society has been accepting the maintenance charges and other outgoings.

3. It may be mentioned that subsequent to the purchase of the flat by Sahai by another agreement he had agreed to sell the flat. AT the relevant time the provisions of Chapter XX-C of the Income Tax Act applied to all such transfers. Consequently that Agreement was filed before the Appropriate Authority. Proceedings were initiated under Section 269UD (of Income Tax Act, 1961) and the Appropriate Authority came to the conclusion that the flat was undervalued and consequently passed the order for purchase of the flat.

. The present petition was filed by the petitioners seeking a relief amongst others for a writ of mandamus or a writ in the nature of mandamus quashing and/or setting aside the letter dated 11th November, 1992 along with the order dated 30th October, 1991 being contrary to the provisions of law, equity and good conscience. The notice dated 11th November, 1992 is purported to be in exercise of the powers of the Respondents under Section 269U(2) (of Income Tax Act, 1961). That notice was issued pursuant to the order dated 30th October, 1990 passed under Section 269UD (of Income Tax Act, 1961).

5. The petitioners as set out earlier are claiming right in the premises as tenants of Ravindra Sahai. Petitioner was put in possession pursuant to the proceedings in execution initiated by the petitioners against the respondents. The respondents were served. They chosen not to challenge the order putting the petitioner back in the premises nor have they taken out any other proceedings in the Court of Small Causes for setting aside the order of putting the petitioners in possession.

4. The case of the petitioners is that as they are a tenant, it is an encumbrance on the property and considering that the words "free from all encumbrances" in Section 269UE (of Income Tax Act, 1961) were struck down by the Supreme Court in C.B. Gautam vs. Union of India and Ors. (1993) 1 SCC 78 the petitioners are entitled to continue in occupation of the premises until evicted by due process of law.

. On the other hand on behalf of the respondents learned Counsel submits that once an order was passed under Section 269UD (of Income Tax Act, 1961) no court could have jurisdiction to pass an order contrary to the order of purchase. Even otherwise it is submitted that the judgment in C.B. Gautam (supra) is prospective and it will not affect the order passed before November, 17, 1992 which is the dated of the judgment.

6. The question for our consideration is whether the respondents could have invoked the power conferred on them under Section 269UE(2) (of Income Tax Act, 1961) and other provisions to direct the petitioners to vacate the premises. For that purpose the judgment in C.B. Gautam (supra) would have a great bearing. The Supreme Court after considering the language of the Section and the contentions urged on behalf of the Union of India by the learned Attorney General to read down the language of Section 269UE(1) (of Income Tax Act, 1961) held that it is not so possible and observed as under:-

"In the result the expression "free from all encumbrances" in sub-section (1) of Section 269-UE (of Income Tax Act, 1961) is struck down and sub-section (1) of Section 269-UE (of Income Tax Act, 1961) must be read without the expression "free from all encumbrances" with the result the property in question would vest in the Central Government subject to such encumbrances and leasehold interests as are subsisting thereon except for such of them as are agreed to be discharged by the vendor before the sale is completed. ...."

The Court also noted that holders of the encumbrances and lease hold interest were persons interested as contemplated in Clause (e) of sub-section (2) of Section 269-UA (of Income Tax Act, 1961). In paragraph 37 the Court noted that in case of monthly tenancies such tenancy would continue even on an order of purchase by the Central Government being made by the appropriate authority concerned under Section 269UD(1) (of Income Tax Act, 1961). But such tenant will lose the protection given to the tenants under the rent protection laws because such laws are not made applicable to properties owned by the Central Government with the result that their tenancies could be terminated by the Central Government.

7. Our attention, however, is invited to paragraph 43 of the judgment which we shall reproduce and reads as under:-

"43. We may clarify that as far as completed transactions are concerned, namely, where after the order for compulsory purchase under Section 269-UD (of Income Tax Act, 1961) was made and possession has been taken over, compensation paid to the owner of the property ad accepted without protest, we see no reason to upset those transactions and hence, nothing we have said in the judgment will invalidate such purchases.

The same will be the position where public auctions have been held of the properties concerned and they are purchased by third parties. In those cases also nothing which we have stated in the judgment will invalidate the purchases."

Based on this judgment, it is sought to be contended by the respondents that as the proceedings were completed before November 17, 1992 and as the amendment to Section 269-UE(1) (of Income Tax Act, 1961) was also brought into effect from the same date the concluded proceedings cannot be reopened. This is one such case and consequently the petition has to be dismissed.

. We have considered the said contention. The Supreme Court in the said paragraph has noted that it is in those cases where the order for compulsory purchase under Section 269-UD (of Income Tax Act, 1961) was made and possession has been taken over, the compensation paid to the owner of the property and accepted without protest, those transactions need not be upset. In our opinion this would not apply to the facts of the present case. Admittedly the petitioners have been claiming right in the suit flat as tenant pursuant to the proceedings initiated by them in the Small Causes Court. The petitioners had a decree in their favour on 4th March, 1991. The said paragraph does not deal with the cases of such persons who had encumbrances on the property and who are also interested persons. The reading of the said paragraph would indicate that it is only those cases where the owner accepted the compensation without protest and possession has been taken would that the judgment in Gautam’s case not apply. In the instant case the judgment in Gautam would squarely apply. Once that be the case, the notice served on the petitioners under Section 269UE (of Income Tax Act, 1961), is clearly without jurisdiction and consequently the petition will have to be allowed. We may, however, make it clear that this would not prevent the respondents considering the observations in Gautam’s case to take steps which in law they are entitled to other than the coercive process under Section 269UE (of Income Tax Act, 1961) for recovery of possession and any other relief.

8. In the light of the above Rule made absolute in terms of prayer clause (b) subject to what we have set out earlier. In the circumstances of the case there shall be no order as to costs.

(R.S.MOHITE, J.) (F.I.REBELLO, J.)

×

Questions

Tenants' Rights Upheld: Court Quashes Notice Under Income Tax Act

Write your CommentSimilar Posts

Generic

- Reportdata/5041.pdf