High Court Rules in Favor of McDowell & Co. Ltd. on Sales Tax Deferral Scheme

Full News

High Court Rules in Favor of McDowell & Co. Ltd. on Sales Tax Deferral Scheme

High Court Rules in Favor of McDowell & Co. Ltd. on Sales Tax Deferral Scheme

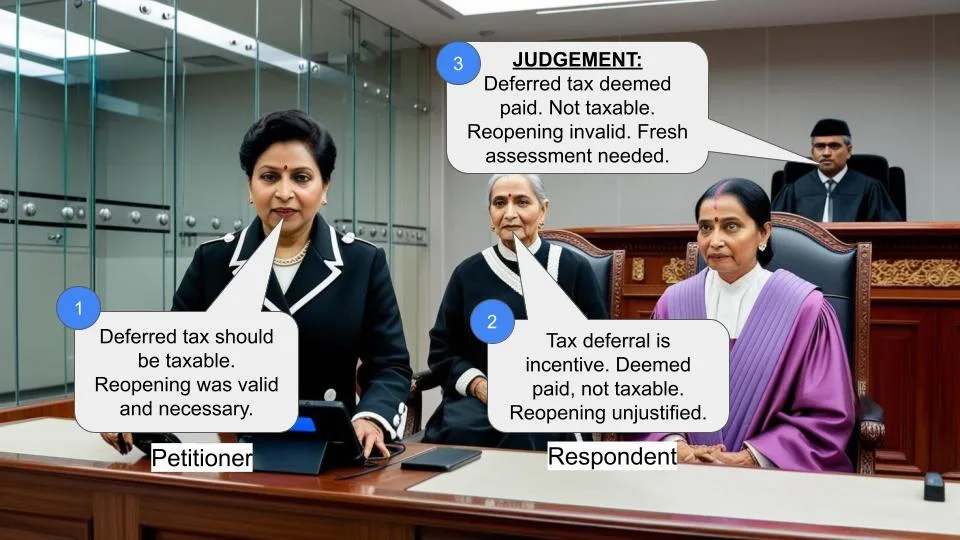

The High Court ruled in favor of McDowell & Co. Ltd., holding that the sales tax deferred under the sales tax deferral loan incentive scheme is deemed as paid and therefore not taxable. The court also addressed issues related to the reopening of assessments and the application of Section 43B (of Income Tax Act, 1961).

Get the full picture - access the original judgement of the court order here.

Case Name:

Commissioner of Income Tax and Another vs. McDowell and Co. Ltd. (High Court of Karnataka)

ITA No.434/2009

Key Takeaways

- The High Court upheld the Tribunal's decision that the sales tax deferred under the incentive scheme is considered paid and not taxable.

- The court found that the reasons for reopening the assessments lacked a nexus and were invalid.

- The Tribunal's decision to remand the case for fresh adjudication was upheld, excluding points already concluded in this judgment.

Issue

Whether the sales tax deferred under the sales tax deferral loan incentive scheme should be deemed as paid and therefore not taxable, and whether the reopening of assessments was valid.

Facts

- The revenue appealed against the Tribunal's order, which held that the deferred sales tax is deemed as paid and not taxable.

- The Tribunal also found that the reopening of assessments was without jurisdiction and invalid.

- The Tribunal remanded the matter back to the assessing authority for fresh adjudication.

Arguments

- Appellant (Revenue):

Argued that the deferred sales tax should be taxable and that the reopening of assessments was valid.

- Respondent (McDowell & Co. Ltd.):

Contended that the deferred sales tax is deemed as paid under the incentive scheme and should not be taxable. They also argued that the reopening of assessments was invalid.

Key Legal Precedents

- The court referred to its own decision in Income Tax Appeal No.899/2008, decided on 02.09.2014, where a similar question was answered in favor of the assessee and against the revenue.

Judgement

The High Court ruled in favor of McDowell & Co. Ltd., holding that the sales tax deferred under the incentive scheme is deemed as paid and not taxable. The court also found that the reopening of assessments was invalid and remanded the matter back to the assessing authority for fresh consideration, excluding points already concluded in this judgment.

FAQs

Q1: What was the main issue in this case?

A1: The main issue was whether the sales tax deferred under the sales tax deferral loan incentive scheme should be deemed as paid and therefore not taxable, and whether the reopening of assessments was valid.

Q2: What did the court decide about the deferred sales tax?

A2: The court decided that the deferred sales tax is deemed as paid and therefore not taxable.

Q3: Was the reopening of assessments considered valid?

A3: No, the court found that the reopening of assessments was without jurisdiction and invalid.

Q4: What will happen next in this case?

A4: The matter has been remanded back to the assessing authority for fresh consideration, excluding points already concluded in this judgment.

Q5: What precedent did the court refer to in its decision?

A5: The court referred to its own decision in Income Tax Appeal No.899/2008, decided on 02.09.2014.

1. Smt. S.R. Anuradha, learned counsel takes notice to the respondent.

2. The revenue has preferred this appeal against the order passed by the Tribunal, which held that the amount representing sales tax deferred under the sales tax deferred loan incentive scheme is to be deemed as paid and therefore not taxable.

3. The following substantial questions of law are raised in this appeal.

“1. Whether the Tribunal was correct in holding that the reasons recorded for reopening of assessments had no nexus and the entire information was available with the Assessing Officer and therefore the reopened assessments was without jurisdiction, invalid and consequently was cancelled?

2. Whether the Tribunal was correct in holding that the assessee was not given sufficient opportunity to establish their case and the order passed u/s.144 (of Income Tax Act, 1961) was required to be set aside and the matter remitted back for fresh adjudication became academic in view of the reassessment being set aside?

3. Whether the Tribunal was correct in holding that a sum of Rs.13,78,41,600/- sales tax amount collected and not paid during the current assessment year will not be hit by Section 43B (of Income Tax Act, 1961) in view of the Board circular and the Bombay Sales Tax Act?”

4. Dealing with the liability of the sales tax, this Court had an occasion to consider the said question of law in the assessee’s case itself in Income Tax Appeal No.899/2008 decided on 02.09.2014, where the said question was answered in favour of the assessee and against the revenue.

5. Insofar as reopening of the assessment is concerned, as the assessee is succeeding on merits, the said question has become purely academic and it is not necessary to answer. It is made very clear that the Tribunal has remanded the matter to the assessing authority for fresh consideration.

6. The assessing authority shall consider it afresh excluding the point, which was concluded in this judgment.

7. Smt. S.R. Anuradha, is permitted to file power within four weeks, from today.

Sd/-

JUDGE

Sd/-

JUDGE

×

Questions

High Court Rules in Favor of McDowell & Co. Ltd. on Sales Tax Deferral Scheme

Write your CommentSimilar Posts

Generic

- Reportdata/4078.pdf