No Capital Gains Tax on Land Acquired Through Punjab Occupancy Tenants Act

Full News

No Capital Gains Tax on Land Acquired Through Punjab Occupancy Tenants Act

No Capital Gains Tax on Land Acquired Through Punjab Occupancy Tenants Act

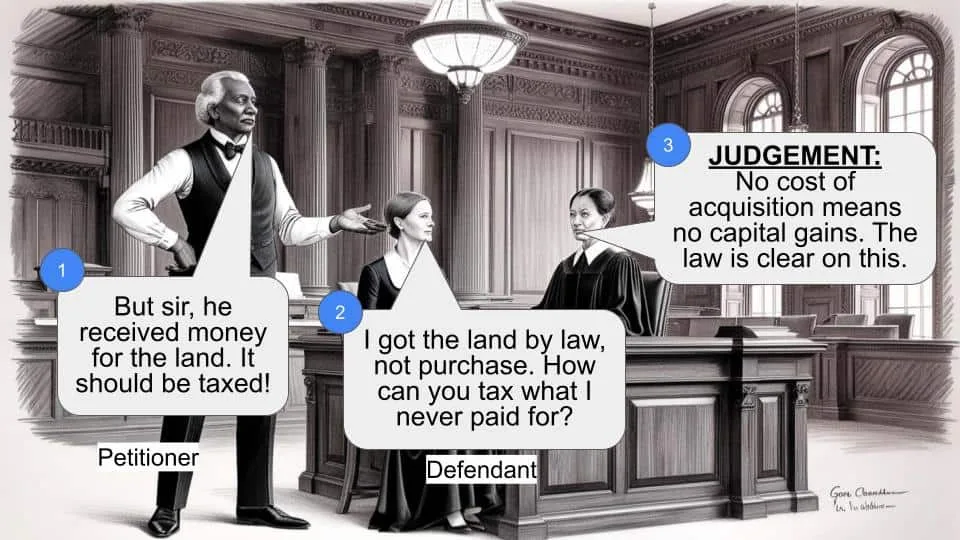

This case involves a dispute between the Commissioner of Income Tax and Amrik Singh (the assessee) regarding the liability of capital gains tax on land acquired through the Punjab Occupancy Tenants (Vesting of Proprietary Rights) Act, 1952. The court ruled in favor of the assessee, stating that no capital gains tax was applicable as the cost of acquisition was nil.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Amrik Singh (High Court of Punjab & Haryana)

ITR No.36 of 1984

Date: 6th February 2008

Key Takeaways:

1. Land acquired through the Punjab Occupancy Tenants Act is not subject to capital gains tax if there's no cost of acquisition.

2. The charging section and computation provisions of capital gains tax form an integrated code.

3. Assets acquired at no cost through operation of law may not be subject to capital gains tax.

Issue:

Whether the assessee is liable to pay capital gains tax on land acquired through the Punjab Occupancy Tenants (Vesting of Proprietary Rights) Act, 1952, when the cost of acquisition was nil?

Facts:

Let's chat about what happened in this case. So, our guy Amrik Singh (the assessee) entered into an agreement with someone named Surjan Singh on February 14, 1970. This agreement recognized Surjan Singh as an occupancy tenant for some land.

Fast forward to January 31, 1972, and a court passes a declaratory decree. This decree basically gave the court's stamp of approval to that earlier agreement, in line with Section 3 (of Income Tax Act, 1961) of the Punjab Occupancy Tenants (Vesting of Proprietary Rights) Act, 1952.

Here's the interesting part - through this process, Amrik Singh became the owner of the land. Before, he just had tenancy rights, but now he had full ownership. And here's the kicker - he got this ownership by operation of law, not by buying it or inheriting it. There's no record of him or anyone before him paying for this land.

Later, when this land was acquired (probably by the government), Amrik Singh received some money for it. The tax folks thought this should be taxed as capital gains, but Amrik Singh disagreed. That's what kicked off this whole legal battle.

Arguments:

Okay, so here's where things get a bit heated. The tax department (the revenue) is saying, "Hey, you got money for this land, so you should pay capital gains tax on it." They're pointing to some earlier court decisions from Gujarat and Calcutta to back up their claim.

On the other side, Amrik Singh is saying, "Hold up! I didn't pay anything for this land in the first place. I got it through this special law. How can you tax me on gains when I had no cost to begin with?" He's basically arguing that you can't calculate capital gains if there was no initial capital investment.

Key Legal Precedents:

Now, this is where things get really interesting. The court looked at a super important case from the Supreme Court: Commissioner of Income Tax, Bangalore v. B.C. Srinivasa Setty (1981) 128 ITR 294. This case said something crucial - the charging section and the computation provisions for capital gains tax are like two peas in a pod. They work together as an integrated code.

What does this mean? Well, if you can't apply the computation provisions to a case (like when there's no cost of acquisition), then that case shouldn't fall under the charging section either. In simpler terms, if you can't calculate the gain, you can't tax it.

The court also mentioned another case they had previously decided: Commissioner of Income-tax v. New Suraj Transport Corporation (P.) Ltd. (1992) 194 ITR 458. This case followed the same principle as the Srinivasa Setty case.

Judgement:

The court sided with Amrik Singh. They said, "Look, this guy got the land through a special law. He didn't pay for it. There's no record of anyone paying for it. So, the cost of acquisition is zero, nil, nada."

The court agreed that when you have an asset with no acquisition cost, and you sell it, you can't really calculate capital gains. And if you can't calculate it, you can't tax it. They said the tax tribunal was right to dismiss the revenue's appeal and say Amrik Singh doesn't owe any capital gains tax.

FAQs:

Q1: Does this mean all land acquired through special laws is exempt from capital gains tax?

A1: Not necessarily. This case specifically deals with land acquired under the Punjab Occupancy Tenants Act where there was no cost of acquisition. Other situations might be different.

Q2: What if there had been a small cost of acquisition?

A2: The judgment might have been different. The key here was that the cost was nil, making it impossible to compute capital gains.

Q3: Could this principle apply to other types of assets?

A3: Potentially, yes. The principle is about assets acquired at no cost through operation of law, so it could apply to similar situations with other types of assets.

Q4: Does this mean the government can never tax such transactions?

A4: Not exactly. The judgment is based on the current structure of capital gains tax law. If the law changes, the tax treatment could change too.

Q5: What's the broader impact of this judgment?

A5: It reinforces the principle that capital gains tax provisions should be read as an integrated code, and highlights a limitation in taxing assets acquired at no cost through operation of law.

The Income-tax Appellate Tribunal, Chandigarh, vide order dated 30.4.1984 passed in RA No.141 of 1983 arising out of ITA No.760 of 1981 for the assessment year 1974-75 has referred the following question to this Court for its opinion:-

“Whether, on the facts and in the circumstances of the case, the Appellate Tribunal erred in law in holding that the assessee was not liable to pay capital gains tax?” The brief facts, out of which the present reference has arisen, are as under:-

The assessee-respondent filed a return declaring taxable income of Rs.6,110/- on 13.12.1977. In response to the notice under Section 143(2) (of Income Tax Act, 1961), the assessee through his counsel attended the assessment proceedings. It is the case of the assessee that the assessee acquired the land through Court Decree dated 12.1.1972 and claimed that he got this land under the provisions of Punjab Occupancy Tenants Act, 1952 and no amount was paid in lieu of the acquisition of land. It was contended that the rights of ownership of the land were, thus, acquired by the assessee by operation of law, namely, Section 3 of the Punjab Occupancy Tenants (Vesting of Proprietory Rights) Act, 1952 and not by purchase or inheritance and therefore, the assessee was not liable to pay any capital gains for the said land. However, the ITO did not agree with the assessee and the amount received by the assessee from the acquisition of the said land was added to the income of the assessee. The said order for assessment was made under Section 143(3) (of Income Tax Act, 1961) on 30.6.1978.

The assessee carried an appeal under Section 250(6) (of Income Tax Act, 1961) before the Commissioner of Appeals who vide his order dated 1.9.1981 allowed the appeal of the assessee holding that no taxable capital gains arise in this case because the capital assets did not cost anything to the assessee in terms of money but had been acquired merely by operation of law. The appeal filed by the revenue before the Income-tax Appellate Tribunal, Chandigarh was also dismissed vide order dated 30.7.1983. The appeal of the revenue was dismissed by the Tribunal relying upon its own decision in the case of Sh. Baldev Singh (ITA Nos.462(ASR)/1979 and 694(ASR)/1979 dated 29.4.1981.

It is relevant to mention here that Baldev Singh's case (supra) was on identical facts and he had also acquired the land on the basis of same Court decree dated 31.1.1972 vide which the present appellant had acquired land.

The revenue filed a reference application under Section 256(1) of the Income Tax Act, 1961 with a prayer for referring the questions mentioned in the application, said to be a question of law and arising out of Tribunal's order dated 1.9.1981.

It has been contended by the counsel for the revenue that the profits or gains arising from the acquisition of the assesses's land is assessible under the head capital gains. Counsel for the revenue has relied upon the judgements of the Gujarat High Court in the case of Commissioner of Income Tax, Gujarat v.Mohanbhai Parabhai (1973) 91 ITR 393 and the Calcutta High Court judgement in the case of K.N. Daftary v. Commissioner of Income Tax, West Bengal (1977) 106 ITR 998.

We have heard learned counsel for the applicant and perused the record.

It is useful to reproduce Section 45 (of Income Tax Act, 1961) as it existed at the relevant time:

“45. (1) Any profits or gains arising from the transfer of a capital asset effected in the previous year shall, save as otherwise provided in sections 53 and 54, be chargeable to income-tax under the head “Capital gains', and shall be deemed to be the income of the previous year in which the transfer took place.”

After perusing the record and considering the various submissions made by the counsel for the revenue, this Court is unable to accept the argument raised by the counsel for the applicant-revenue. We find that the Hon'ble Supreme Court in the case of Commissioner of Income Tax, Bangalore v. B.C. Srinivasa Setty (1981) 128 ITR 294 has held with regard to capital gains that the charging section and the computation provision together constitute an integrated code. When there is a case to which the computation provisions cannot apply at all it is evident that such a case was not entitled to fall within the charging section. It is further held that all the transaction encompassed by Section 45 (of Income Tax Act, 1961) must fall under the governance of its computation provisions. A transaction to which those provisions cannot be applied must be regarded as never intended by Section 45 (of Income Tax Act, 1961) to be the subject of the charge. What is contemplated by Section 48(ii) (of Income Tax Act, 1961) is an asset in the acquisition of which it is possible to envisage a cost. It must be an asset which possesses the inherent quality of being available on the expenditure of money to a person seeking to acquire it. None of the provisions pertaining to the head 'capital gains' suggests that they include an asset in the acquisition of which no cost at all can be conceived.

This Court has also followed the above ratio of law in the case of Commissioner of Income-tax v. New Suraj Transport Corporation (P.) Ltd.(1992) 194 ITR 458 .

A perusal of the facts of the present case would show that the assessee entered into an agreement with Sh. Surjan Singh vide agreement dated 14.2.1970 recognising him to be the occupancy Tenant in respect of certain land. A declaratory decree was subsequently passed by the Court on 31.1.1972 whereby agreement dated 14.2.1970 was given the Court’s sanction in terms of Section 3 (of Income Tax Act, 1961) of the Punjab Occupancy Tenant’s (Vesting of Proprietory Rights) Act, 1952 in the following words:-

“In the terms of the statement of the parties and counsel for the parties present, decree for declaration declaring the plaintiff No.1 to 4 to be the owners of land measuring 196 kanals 1 marla to the extent of 1⁄2 share jointly while plaintiffs No.5 to 6 to be the owners of the remaining half share more fully described in the heading of the plaintiff situated at Village Jamalpur Awana, Tehsil & Distt Ludhiana is passed in favour of the plaintiff and against the defendant.”

Thus, the assessee became the owner of the land in respect of which he had earlier acquired only the tenancy rights. Thus, the assessee had acquired the ownership rights in the land by operation of law and not by purchase or inheritance. It is also useful to refer to the order of the Tribunal passed in ITA No.462/ASR/1979 filed by Baldev Singh and ITA No.694/ASR/1979 filed by the revenue against said Sh.Baldev Singh.

“The case before us is one of a promise never to eject in view of the written agreement dated 14.2.1970. This agreement got approval of the Court of Senior Sub Judge Ludhiana as per order dated 31.1.1972 which we have abstracted supra. The historical background of the acquisition of the land by Sh. Surjan Singh also shows that there is no record of any payment made for the acquisition of the land. In any case , the assessee acquired the land in view of the right of occupancy etc. under Section 8 of the Punjab Tenancy Act read with Section 3 of the Punjab Occupancy Tenants (vesting of propreitory Rights) Act, 1952 without payment of anythings. In other words, the cost of the acquisition of the land to the assessee was nil. When such a situation arises and an asset acquired by the assessee is sold, our view is that no capital gains is assessable to tax under the Act arising out of such a transaction.”

From the above facts, it is clearly established that there is no record of any payment made for the acquisition of the land in question either by the assessee or his predecessor-in-interest. Therefore, the cost of acquisition in this case has been rightly taken as Nil. Even otherwise, the revenue has never taken stand to say that the cost of acquisition of the land at the hands of the assessee or his predecessor-in-interest was not Nil and they had made any payment of compensation/price for the acquisition of the said land. Thus, the cost of the land as Nil at the hands of the assessee has been taken correctly by the Tribunal. Thus, in view of the authoritative pronouncements of the Hon’ble Supreme Court in the case of Commissioner of Income Tax, Bangalore v. B.C. Srinivasa Shetty (supra), the Tribunal was right while dismissing the appeal of the revenue in the case of the assessee holding that the assessee was not liable to pay any capital gains tax.

In view of the above, the question of law is answered in the negative and against the revenue. Thus, the reference is answered accordingly.

(RAKESH KUMAR GARG)

JUDGE

(SATISH KUMAR MITTAL)

JUDGE

×

Similar Ripples

Questions

No Capital Gains Tax on Land Acquired Through Punjab Occupancy Tenants Act

Write your CommentSimilar Posts

Generic

- Reportdata/4881.pdf