Revenue's appeal dismissed: Sub-license fee ruled as revenue expenditure

Full News

Revenue's appeal dismissed: Sub-license fee ruled as revenue expenditure

Revenue's appeal dismissed: Sub-license fee ruled as revenue expenditure

This case involves an appeal by the Revenue (tax authorities) against a decision made by the Income Tax Appellate Tribunal (ITAT) in favor of Western Agri Seeds Ltd. The main dispute was about the classification of certain expenses, particularly a sub-license fee, as revenue expenditure. The High Court dismissed the Revenue's appeal, agreeing with the ITAT's decision.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax Vs Western Agri Seeds Ltd. (High Court of Gujarat)

R/Tax Appeal No.835 of 2019

Date: 20th January 2020

Key Takeaways:

1. Sub-license fees for using technology can be treated as revenue expenditure if they don't create a capital asset.

2. The court relied on previous judgments to support the classification of such fees as revenue expenditure.

3. The decision reinforces the principle that expenses incurred for business purposes, even if non-refundable, can be considered revenue expenditure.

Issue:

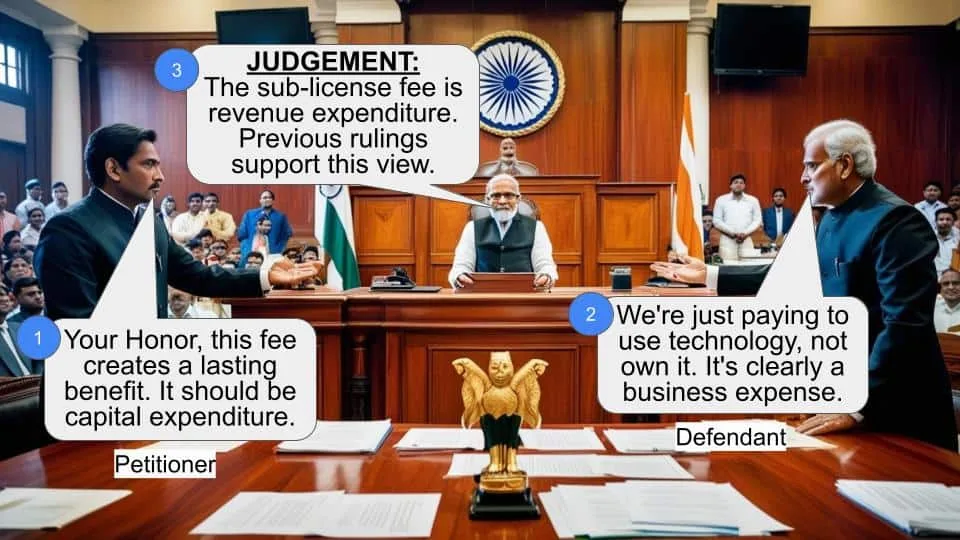

The main question was whether the sub-license fee of Rs. 27,57,500/- paid by Western Agri Seeds Ltd. should be classified as revenue expenditure or capital expenditure for tax purposes.

Facts:

Western Agri Seeds Ltd. paid a sub-license fee to use Monsanto technology for producing and selling genetically modified hybrid cotton plant seeds. The tax authorities initially didn't agree with how the company classified this expense, but the CIT(Appeals) and then the ITAT sided with the company. The Revenue wasn't happy with this and took it to the High Court.

Arguments:

The Revenue's main argument was that the ITAT made a mistake in agreeing with the CIT(Appeals) decision to allow the sub-license fee as a revenue expense. They thought it should be treated differently for tax purposes.

On the other hand, Western Agri Seeds Ltd. argued that this fee was a business expense. They said it didn't create any new asset for the company, it just helped them do their business better.

Key Legal Precedents:

The court relied on a couple of important previous cases here:

1. CIT vs. J K Synthetic Ltd. (309 ITR 371):

This Delhi High Court case said that if a company gets technical assistance or information related to manufacturing, but doesn't actually own the know-how, it's treated as revenue expenditure.

2. The case of Urja Products Ltd.:

The ITAT mentioned this case too, which had a similar issue and was decided in favor of the taxpayer.

Judgement:

They agreed with the ITAT's decision. They said that the sub-license fee paid by Western Agri Seeds Ltd. should be treated as revenue expenditure. Why? Because the company didn't actually own the technology - they were just paying to use it for their business. The court thought this made sense based on previous similar cases.

FAQs:

Q1: What's the difference between revenue and capital expenditure?

A1: Revenue expenditure is a regular business expense that provides short-term benefits, while capital expenditure creates or improves a long-term asset.

Q2: Why is this decision important?

A2: It clarifies how certain technology licensing fees should be treated for tax purposes, which can affect many businesses using licensed technologies.

Q3: Does this mean all license fees will be treated as revenue expenditure?

A3: Not necessarily. Each case is unique, and the specific terms of the license agreement and how it's used in the business are important factors.

Q4: What impact does this have on Western Agri Seeds Ltd.?

A4: It allows them to deduct the full amount of the sub-license fee as a business expense, potentially reducing their taxable income.

Q5: Could this decision be appealed further?

A5: While it's possible, the High Court's agreement with lower authorities makes a successful appeal less likely.

1. This Tax Appeal under Section 260A (of Income Tax Act, 1961) (for short, 'the Act, 1961') is at the instance of the Revenue and is directed against the order passed by the Income Tax Appellate Tribunal, Ahmedabad 'B' Bench, dated 27th March 2019 in the ITA No.2796/Ahd/2014 for A.Y. 201112.

2. The Revenue has proposed the following questions as the substantial questions of law involved in this appeal:

“[A] Whether the Appellate Tribunal has erred considering the facts and circumstances of the case and in law, in upholding the order of the CIT(A) for deleting disallowance on account of discount and rate difference to Rs.2,31,95,051/?

[B] Whether the Appellate Tribunal has erred considering the facts and circumstances of the case and in law, in upholding the order of the CIT(A) for deleting disallowance made u/s 40(A)(2) (of Income Tax Act, 1961) to Rs.1,55,06,080/?

[C] Whether the Appellate Tribunal has erred considering the facts and circumstances of the case and in law, in upholding the order of the CIT(A) for deleting addition of Sub License Free Expenses of Rs.27,57,500/?”

3. For the reasons recorded by us today, while dismissing the Tax No.834 of 2019, this Tax Appeal stands dismissed so far as the questions Nos.2[A] and 2[B] respectively, as proposed by the Revenue, is concerned. The question No.2[C], as proposed, is one relating to deletion of addition of Sub License Fee Expenses to the tune of Rs.27,57,500/. In this regard, the Tribunal, while concurring with the finding recorded by the CIT(Appeals) held as under:

“Heard the respective parties, perused the relevant materials available on record. It appears that the appellant has acquired sublicense for using Monsanto technology and such sublicense is nontransferable. Such license is provided to the assessee to test produce and sell genetically modified hybrid cotton plant seeds in the territory of the appellant for effectively increasing its business; no asset, however, is created. While holding such expenses as revenue expenditure the Ld. CIT(A) relied upon the judgment passed by the Hon'ble Delhi High Court in the matter of CIT vs. J K Synthetic Ltd. reported at 309 ITR 371 wherein it was held that since under the agreement the assessee has obtained a technical assistance and acquired some technical information which was a knowhow related to process of manufacture, then it is not a transfer of the ownership of the knowhow and to be treated as revenue expenditure. The judgment passed by the Coordinate Bench, in the case of Urja Products Ltd. was also mentioned in the order passed by the Ld. CIT(A) wherein similar issue has been decided in favour of the appellant. The nonrefundable upfront fee itself does not mean a capital expenditure but the same is required to be paid for acquiring license from the main company which is used for the purposes of business and hence the entire expenditure incurred by the appellant is treated as revenue expenditure. We, therefore, find no infirmity in the order passed by the Ld. CIT(A) in deleting such addition of Rs.27,57,500/ as made by the Ld. AO. We, therefore, do not hesitate to confirm the same. So, as to warrant inference. The question is accordingly answered in the affirmative that is in favour of the assessee and against the Revenue. Consequently the appeal fails and is accordingly dismissed.”

4. Thus, we take notice of the fact that the Tribunal has relied upon the decision of the Delhi High Court in the case of CIT vs. J K Synthetic Ltd reported in 309 ITR 371, wherein the Delhi High Court has taken the view that no under the agreement the assessee has obtained a technical assistance and acquired some technical information which was a knowhow related to process of manufacture, then it is not a transfer of the ownership of the knowhow and to be treated as revenue expenditure.

5. We are in complete agreement with the finding recorded by the Tribunal as regards the proposed question No.2[C] is concerned.

6. In the result, this appeal fails and is hereby dismissed so far as the third question, as proposed by the Revenue, is concerned.

(J. B. PARDIWALA, J)

(BHARGAV D. KARIA, J)

×

Questions

Revenue's appeal dismissed: Sub-license fee ruled as revenue expenditure

Write your CommentSimilar Posts

Generic

- Reportdata/6112.pdf