Settlement Commission's Decision on Tax Disclosure Challenged

Full News

Settlement Commission's Decision on Tax Disclosure Challenged

Settlement Commission's Decision on Tax Disclosure Challenged

This case involves the Income Tax Department challenging a decision by the Income Tax Settlement Commission regarding Boyance Infrastructure Private Limited. The main issue was whether the company made a full and true disclosure of income in its application to the Settlement Commission. The court ultimately decided not to interfere with the Commission's decision to proceed with the application, leaving the question of disclosure to be examined in further proceedings.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs. Boyance Infrastructure Private Limited (High Court of Karnataka)

Writ Petitions No. 47042-47045 of 2015(T-IT)

Date: 16th December 2015

Key Takeaways:

- The court emphasized the role of the Settlement Commission in determining the maintainability of applications and the adequacy of income disclosures.

- The decision highlights the procedural aspects of tax settlement applications under Section 245D (of Income Tax Act, 1961).

- The case underscores the importance of full and true disclosure in tax settlement proceedings.

Issue

Did Boyance Infrastructure Private Limited make a full and true disclosure of its income in its application to the Income Tax Settlement Commission?

Facts

- A search was conducted on Boyance Infrastructure Private Limited under Section 132 (of Income Tax Act, 1961), revealing undisclosed income.

- The company admitted to undisclosed income for several assessment years and filed revised returns.

- The Settlement Commission allowed the application to proceed, despite the Department's contention that the disclosure was not full and true.

- The Department challenged this decision, arguing it set a dangerous precedent.

Arguments

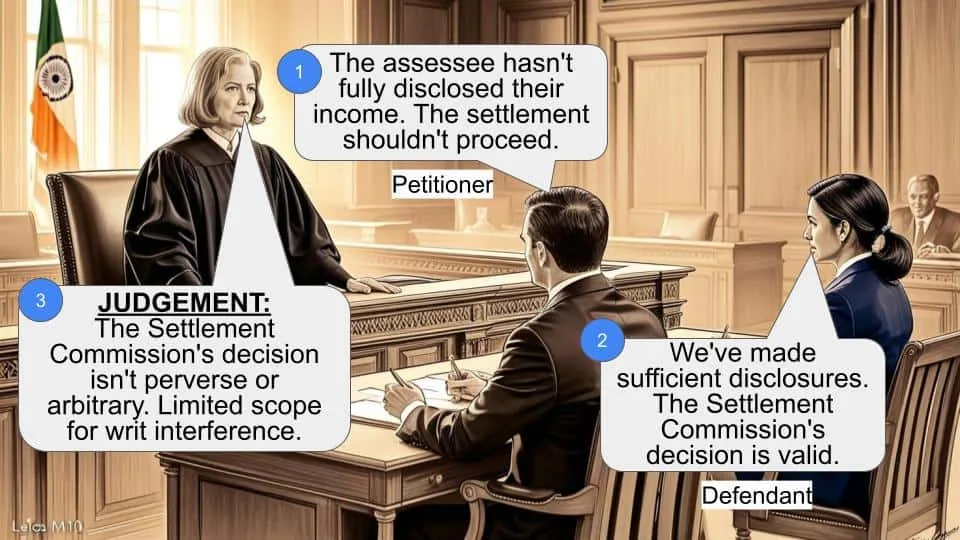

- Income Tax Department: Argued that the company failed to make a full and true disclosure initially, which is a prerequisite for the Settlement Commission to entertain an application.

- Boyance Infrastructure: Maintained that the Settlement Commission's decision to proceed was valid and that the issue of disclosure could be examined in further proceedings.

Key Legal Precedents

- Ajmera Housing Corporation & Anr. vs. Commissioner of Income Tax (2010) 326 ITR 0642: Emphasized the necessity of full and true disclosure at the initial stage of settlement applications.

- Commissioner of Income Tax vs. K. Jayaprakash Narayanan (2009) 184 Taxman 85 (SC): Discussed the role of the Settlement Commission in examining the maintainability of applications and disclosures.

Judgement

The court decided not to interfere with the Settlement Commission's decision to proceed with the application. It left the question of whether the disclosure was full and true to be examined in further proceedings under Section 245D(4) (of Income Tax Act, 1961). The court found no prejudice to the Department since the company had paid taxes on a significant amount.

FAQs

Q1: What was the main legal question in this case?

A1: Whether Boyance Infrastructure made a full and true disclosure of its income in its application to the Settlement Commission.

Q2: Why did the court not interfere with the Settlement Commission's decision?

A2: The court believed the Settlement Commission was in the best position to examine the disclosure issue in further proceedings and found no immediate prejudice to the Department.

Q3: What does this case mean for future tax settlement applications?

A3: It reinforces the importance of full and true disclosure in settlement applications and clarifies the procedural role of the Settlement Commission in such matters.

Heard the learned counsel for the petitioner.

The petitioner is the Income Tax Department seeking to question an order passed by the Income Tax Settlement Commission. The background to the present petition is, there was a search conducted under Section 132 (of Income Tax Act, 1961) (hereinafter referred to as ‘the IT Act’, for brevity) of the Company called Boyance Infrastructure Private Limited on 11.10.2012.

The statement made under Section 132(4) (of Income Tax Act, 1961) of the Chief Executive Officer and the Managing Director of the assessee company was recorded on 11.10.2012. It was admitted that the payments made to various subcontractors was without actual work being done and the genuineness of payments could not be substantiated. On 22.10.2012, the statement under Section 132(4) (of Income Tax Act, 1961) of the Director of the assessee company and the Director of several other companies of the Boyance group was recorded. It was admitted in the statement that a sum of Rs.130,54,97,928/- was undisclosed income. This was admitted for the Assessment year 2010-11, 2011-12 and 2012-13.

On 8.12.2013, the further statement of the Director of the assessee company was recorded under Section 132(4) (of Income Tax Act, 1961) admitting that a sum of Rs.300,69,69,246/- was the undisclosed income and it was admitted for the very assessment years referred to above.

Hence, notice under Section 153A (of Income Tax Act, 1961) was issued calling upon the assessee to file a return of income within a period of 30 days from the date of service of notice, for the assessment years 2009-10, 2010-11, 2011-12 and 2012-13. In response to the notice, the assessee filed return of income for the assessment years 2010-11, 2011-12 and 2012-13, admitting total income of Rs.40,63,90,380/- for the assessment year 2010-11, Rs.195,41,53,360/- for the assessment year 2011-12 and Rs.108,28,25,530/- for the assessment year 2012-13.

Notice under Section 142(1) (of Income Tax Act, 1961) was issued on 8.7.2014, as the provisions of Section 153A (of Income Tax Act, 1961) was not applicable for the assessment year 2013-14.

On 24.03.2015, the assessee had thereafter filed revised

return of income for the assessment years 2010-11, 2011-12,

2012-13 and 2013-14. In the revised return for the said years,

the assessee had offered the same income which was offered in

the returns filed under Sections 139(1) (of Income Tax Act, 1961), 139(4) and 139(5) of

the IT Act. For the assessment year 2013-14, the income

offered in the return filed under Section 139(1) (of Income Tax Act, 1961) was reduced

considerably. The total income declared in the revised returns

of income for the assessment year 2010-11 is Rs.70,53,040/-,

for the assessment year 2011-12 is Rs.27,21,82,040/- and for

the assessment year 2012-13 is Rs.52,23,44,370/-.

The assessee had then filed an affidavit dated 26.03.2015

through its Managing Director, withdrawing the admission

made in the statement recorded under Section 132(4) (of Income Tax Act, 1961) and withdrawing the declaration made in the returns of

income filed under Section 153A (of Income Tax Act, 1961), though the

same is not permissible under the IT Act.

The assessee had approached the Settlement Commission

for the Assessment years 2010-11 to 2013-14. The additional

income offered for the assessment years 2010-11 to 2013-14

was Rs.86,85,77,281/- which is less than the amount offered in

the returns filed under Section 153A (of Income Tax Act, 1961) for the

assessment years 2010-11 to 2012-13 of Rs.344,33,69,270/-.

The income offered for the assessment year 2013-14 in the

original return of income was Rs.34,91,31,080/-, whereas in the

revised return of income the same has been reduced to

Rs.16,86,32,187/-.

The Settlement Commission it transpires, has passed an

order on 7.4.2014 under Section 245D(1) (of Income Tax Act, 1961) by

allowing the application to be proceeded further. The

Settlement Commission had then called for a report under

Section 245D(2B) (of Income Tax Act, 1961) from the petitioner, vide notice dated

17.04.2015. The Commissioner of Income Tax had submitted a

report as required under the said section, vide letter dated

26.05.2015. Thereafter, the Settlement Commission has passed

an order dated 4.6.2015 under Section 245D(2C) (of Income Tax Act, 1961)

and proceeded to declare the application filed by the assessee as

not valid, by keeping open the issue regarding full and true

disclosure of income to be examined in the course of the

proceedings under Section 245D(4) (of Income Tax Act, 1961). It is this

which is sought to be challenged in the present petitions.

3. The learned counsel for the petitioner would submit

that the procedure adopted by the Settlement Commission

would set a very dangerous precedent, as the law as laid down

by the Supreme Court is completely violated in the case of

Ajmera Housing Corporation & Anr. Etc. vs. Commissioner

of Income Tax (2010) 326 ITR 0642, wherein according to the

learned counsel for the petitioner, the Supreme Court while

considering the very issue as to the procedure to be followed in

an application being filed before the Settlement Commission,

had observed that the requirement of making a full and true

disclosure of the income at the initial stage, was a precondition

to entertainment of any such application. This has been laid

down in Paragraph 26 of the judgment, which has been totally

overlooked by the Settlement Commission. Therefore, he

would seek intervention by this court.

4. While on the other hand, the learned Senior Advocate

Shri Udaya Holla appearing for the learned counsel for

Respondent No.1 would point out that there is no infirmity

committed by the Settlement Commission. The judgment

sought to be relied upon was a judgment rendered against a

final order of the Settlement Commission. On the other hand,

the irregularity sought to be complained of is no irregularity at

all. The Supreme Court has recognized this position in a

reported judgment in the case of Commissioner of Income Tax

vs. K. Jayaprakash Narayanan (2009) 184 Taxman 85 (SC),

wherein the Supreme Court has observed that the case of the

Department that the assessee had failed to make full and true

disclosure in the first instance and the said declaration by way

of second declaration, could not be a ground for admitting the

application under Section 245D (of Income Tax Act, 1961) and since the petition was filed

only against an order of the Settlement Commission admitting

the application of the assessee under Section 245D (of Income Tax Act, 1961), the court

did not feel it proper to interfere at that stage. But, it was made

clear that the point of maintainability of the application could

be raised as a contention by the Department before the

Settlement Commission and the Settlement Commission would

be entitled to examine that question at the final hearing.

On the other hand, if this court were to issue rule and to

admit the case to file and take it up for final hearing several

years down the line, it would cause prejudice to the

Department. Therefore, since the Settlement Commission

would be in a position to decide the application along with the

point as regards the maintainability in the first instance, there is

no prejudice caused to the Department.

Since it is also an admitted fact that the respondent has

paid the entire tax on a sum exceeding Rs.300 crore, there is

absolutely no prejudice caused to the Department. The

petitions are misconceived. The submission that it would lay

down a wrong precedent if the petitions are dismissed, is also

not correct, since the Supreme Court has already laid down the

precedent. Therefore, the petitions are disposed of.

Interim order granted earlier stands vacated.

Sd/-

JUDGE

×

Similar Ripples

Questions

Settlement Commission's Decision on Tax Disclosure Challenged

Write your CommentSimilar Posts

Generic

- Reportdata/3228.pdf