Tax Appeal Dismissed: Court Upholds Tribunal's Decision on Unexplained Income a…

Full News

Tax Appeal Dismissed: Court Upholds Tribunal's Decision on Unexplained Income and Expenditure

Tax Appeal Dismissed: Court Upholds Tribunal's Decision on Unexplained Income and Expenditure

This case involves an appeal by the Revenue (tax authorities) against a judgment of the Income Tax Appellate Tribunal (ITAT) regarding the assessment of unexplained income and expenditure of an individual assessee, Hassan Ali Khan. The High Court dismissed the appeal, affirming the Tribunal's decision to delete certain additions made by the Assessing Officer and reduce others.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax Vs Hassan Ali Khan (High Court of Bombay)

Income Tax Appeal No.1550 of 2016

Date: 18th February 2016

Key Takeaways:

1. The court emphasized the importance of concrete evidence in establishing unexplained income.

2. Presumptions under Section 292C (of Income Tax Act, 1961) don't automatically apply when documents are seized from third parties.

3. The court showed deference to the Tribunal's factual findings, highlighting the limited scope for interference in appeals on questions of law.

Issue:

Was the Income Tax Appellate Tribunal justified in:

a) Deleting the addition of Rs.8,57,00,000 on account of unexplained income appearing in the name of Pan Asian Distribution Ltd?

b) Restricting the addition on account of unexplained expenditure in lifestyle-related expenses from Rs.28.50 lacs to Rs.7.50 lacs?

Facts:

1. The case relates to the Assessment Year 2000-01.

2. During a search operation at the residence of Kashinath Tapuriah (a third party), three bank drafts from Union Bank of Switzerland were found and seized.

3. One draft was for 2 Million US$ in favor of Pan Asian Distribution Ltd, payable in Singapore.

4. Another draft was for 2 Million US$ in favor of the assessee (Hassan Ali Khan), payable in India.

5. The Assessing Officer added the Indian Rupee equivalent of these sums to the assessee's income.

6. The Tribunal confirmed the addition related to the draft in the assessee's name but deleted the addition related to Pan Asian Distribution Ltd.

Arguments:

Revenue's Arguments:

1. The document containing details of Pan Asian Distribution Ltd was seized during the search, triggering presumptions under Sections 132(4A) (of Income Tax Act, 1961) and 292C (of Income Tax Act, 1961).

2. The assessee admitted to Rs.28.50 lacs in lifestyle-related expenses in a statement recorded under Section 132(4) (of Income Tax Act, 1961).

Assessee's Arguments:

1. The search was not conducted at the assessee's premises, and the draft in question was not in the assessee's name.

2. There was no evidence linking the assessee to Pan Asian Distribution Ltd.

3. The assessee contested the amount of lifestyle-related expenses.

Key Legal Precedents:

The judgment doesn't explicitly cite any legal precedents. However, it refers to:

1. Section 292C (of Income Tax Act, 1961), regarding presumptions in cases where assets are found during a search.

2. Section 132(4) (of Income Tax Act, 1961), concerning statements made during a search operation.

Judgement:

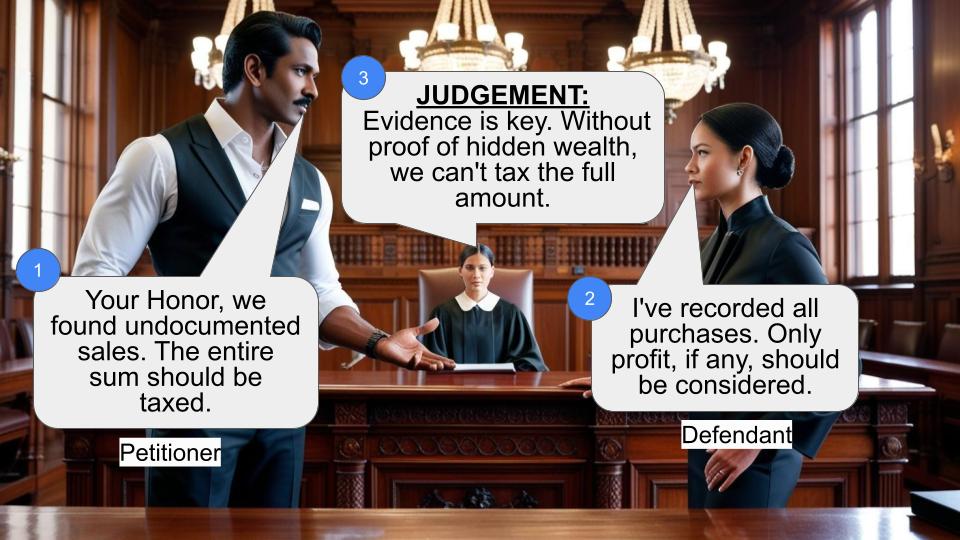

1. The court dismissed the appeal, upholding the Tribunal's decision.

2. Regarding the Pan Asian Distribution Ltd draft, the court agreed with the Tribunal that there was insufficient evidence to link it to the assessee.

3. The court noted that the presumption under Section 292C (of Income Tax Act, 1961) wouldn't apply as the documents were seized from a third party.

4. On the lifestyle expenses, the court viewed the Tribunal's reduction of the addition as a factual determination, not warranting interference.

5. The court emphasized that the issues were primarily factual and didn't give rise to questions of law.

FAQs:

Q1: Why did the court dismiss the Revenue's appeal?

A1: The court found that the issues raised were primarily factual, and there was no substantial question of law to warrant interference with the Tribunal's decision.

Q2: What was the significance of the bank drafts being found at a third party's residence?

A2: This fact weakened the Revenue's case as it meant that the presumptions under Section 292C (of Income Tax Act, 1961) wouldn't automatically apply.

Q3: Why didn't the court accept the Revenue's argument about the bank's letter?

A3: The court felt that a mere letter from the bank wasn't sufficient to establish a connection between the draft amount and the assessee, especially when the draft was in favor of a limited company.

Q4: What does this judgment suggest about the burden of proof in tax cases?

A4: It suggests that the tax authorities need to provide concrete evidence to establish unexplained income, especially when documents are seized from third parties.

Q5: How did the court view the Tribunal's decision on lifestyle expenses?

A5: The court saw it as a factual determination based on the material evidence, and thus not a matter for the court to interfere with in an appeal on questions of law.

1. The Revenue is in Appeal against the Judgment of the Income Tax Appellate Tribunal (in short “the Tribunal”), raising the following questions for our consideration:

“(a) Whether on the facts and circumstances of the case and in law, the Tribunal was justified in deleting addition of Rs.8,57,00,000/ on account of unexplained income appearing in the name of Pan Asian Distribution Ltd by not appreciating the document containing the details was seized during the course of search and therefore the presumptions envisaged in the provisions of Section 132(4A) (of Income Tax Act, 1961) as well as provision of Section 292C (of Income Tax Act, 1961) are squarely applicable in the case of the assessee and consequently the AO was justified in treating the said amount as the assessee's unexplained income?

(b) Whether on the facts and circumstances of the case and in law, the Tribunal was justified in restricting the addition on account of unexplained expenditure in lifestyle related expenses from Rs.28.50 lacs as admitted by the assessee in his statement recorded on oath u/s. 132(4) (of Income Tax Act, 1961) to Rs.7.50 lacs, without appreciating the fact that the assessee had failed to furnish any evidence to the contrary either before the Assessing Officer or the CIT(A) or before the Tribunal itself?”

2. The Respondent Assesssee is an individual. Appeal relates to Assessment Year 200001. During the search operation at the residence of one Kashinath Tapuriah, three bank drafts of Union Bank of Switzerland were found and seized. One bank draft was for payment of 2 Million US$ drawn in favour of one Pan Asian Distribution Ltd, payable at Singapore. Another draft was for a sum of Rs.2 Million US$ drawn in favour of the the RespondentAssessee, payable in India. The Assessing Officer added Indian Rupees, equivalent of such sums in the hands of the Assessee. The issue eventually reached to the Tribunal. The Tribunal by the impugned judgment, confirmed the addition in relation to bank draft in the name of the Assessee, whereas addition in connection with the bank draft in favour of the Pan Asian Distribution Ltd., was deleted.

3. Having heard the learned Counsel for the parties and having perused the documents on record, we notice that, the search was not conducted at the premises of the Assessee but at the residence of the third party from where, the bank drafts were recovered. The draft in question did not contain name of the Assessee as payee but of Pan Asian Distribution Ltd. It was in this background that, the Tribunal refused to accept the Revenue's contention that, the Assessee was beneficiary of this payment. The Tribunal noted that, there was no material on record to suggest that, such a company did not exist nor there was any evidence of any link between the said Company and the Assessee. The Tribunal, therefore, observed that the presumption as referred to in Section 292C (of Income Tax Act, 1961) (in short “the Act”) in such a case would not arise. Entire issue is thus factual.

4. Counsel for the Revenue, however, vehemently contended that, during the search operation, Revenue Authorities had found a document in the nature of letter from the bank, pointing out that, the last date for presentation of the draft in question had expired and that the Assessee should get the draft revalidated. He submitted that, no such letter would have been written by the bank, unless the assessee was the beneficiary of the payments.

5. In our opinion, mere letter from the bank would not established a relation between the payable amount and the assessee, particularly when the draft was in favour of a limited Company. As recorded, documents were not seized from the possession of the Assessee but during the raid from a third party. No question of law, therefore arises.

6. Question 2 relates to addition of the amount of the Assessee's unexplained expenditure. The Tribunal considered the material on record and reduced these additions made by the Assessing Officer under this head. The entire issue is factual.

7. In the result, Appeal dismissed.

(M.S.SANKLECHA,J.) (AKIL KURESHI,J.)

×

Similar Ripples

Questions

Tax Appeal Dismissed: Court Upholds Tribunal's Decision on Unexplained Income and Expenditure

Write your CommentSimilar Posts

Generic

- Reportdata/6036.pdf