Full News

Tax Deduction Dilemma: Court Rules Filing Form 15I/J is Directory, Not Mandatory

Tax Deduction Dilemma: Court Rules Filing Form 15I/J is Directory, Not Mandatory

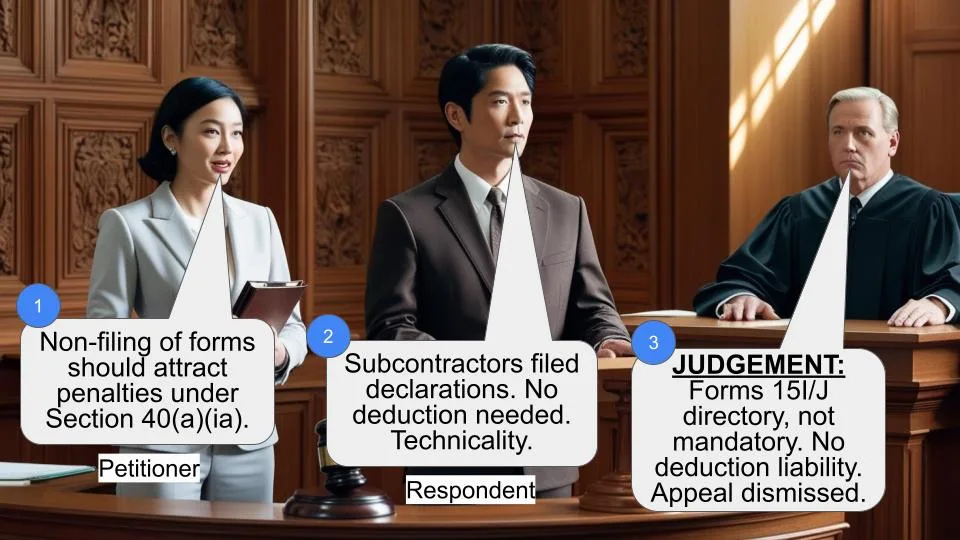

This case involves the Commissioner of Income Tax appealing against Sri Marikamba Transport Co. regarding the applicability of Section 40(a)(ia) (of Income Tax Act, 1961). The court ruled in favor of the assessee, stating that once declaration forms are filed by subcontractors, the liability to deduct tax doesn't arise, and filing Form 15I/J is directory, not mandatory.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Sri Marikamba Transport Co. (High Court of Karnataka)

ITA No. 553 of 2013

Date: 13th April 2015

Key Takeaways:

1. Filing Form 15I/J is directory, not mandatory for tax deduction purposes.

2. Once subcontractors file declaration forms, the assessee's liability to deduct tax ceases.

3. Non-filing of Form 15I/J is considered a technical default, not attracting Section 40(a)(ia) (of Income Tax Act, 1961).

4. The court's decision aligns with previous rulings, reinforcing the interpretation of Section 194C(3) (of Income Tax Act, 1961).

Issue:

Does the non-filing of Form No. 15-I/J within the prescribed time constitute a technical default, or does it attract the provisions of Section 40(a)(ia) (of Income Tax Act, 1961)?

Facts:

1. Sri Marikamba Transport Co. (assessee) filed a return for the Assessment Year 2009-10, declaring a total income of Rs.19,07,890/-.

2. The Assessing Officer completed a scrutiny assessment, computing the total income at Rs.17,82,64,920/-.

3. The officer added payments of Rs.17,63,57,030/- made to sub-contractors under Section 40(a)(ia) (of Income Tax Act, 1961).

4. The assessee appealed to the Commissioner of Income Tax (A), Hubli, who allowed the appeal.

5. The revenue then appealed to the Income Tax Appellate Tribunal (ITAT), Bangalore, which dismissed the appeal.

6. The revenue finally appealed to the High Court under Section 260A (of Income Tax Act, 1961).

Arguments:

The Revenue argued that non-filing of Form 15I/J within the prescribed time should attract the provisions of Section 40(a)(ia) (of Income Tax Act, 1961), making the assessee liable for tax deduction.

The assessee contended that since the subcontractors had filed Form 15I, the liability to deduct tax didn't arise, and non-filing of Form 15J was merely a technical default.

Key Legal Precedents:

1. Valibhai Khanbai Mankad vs DCIT (OSD) (ITA No.2228/Ahd/2009 dated 29.04.2011): The ITAT Ahmedabad Bench ruling, which was later upheld by the Gujarat High Court.

2. (2013) 216 Taxman 18 (Guj): The Gujarat High Court judgment upholding the ITAT Ahmedabad Bench decision.

Judgement:

The court ruled in favor of the assessee, holding that:

1. Once declaration forms (Form 15I) are filed by subcontractors, the assessee's liability to deduct tax ceases.

2. Filing of Form 15I/J is directory, not mandatory.

3. Non-filing of Form 15J is only a technical default and doesn't attract Section 40(a)(ia) (of Income Tax Act, 1961).

4. The court agreed with the ITAT's decision and dismissed the revenue's appeal.

FAQs:

1. Q: What is the significance of Form 15I and 15J?

A: Form 15I is filed by subcontractors, while Form 15J is filed by the assessee. These forms are related to tax deduction requirements under Section 194C(3) (of Income Tax Act, 1961).

2. Q: What does it mean that filing Form 15I/J is "directory, not mandatory"?

A: It means that while it's recommended to file these forms, failure to do so doesn't automatically result in penalties or tax liabilities if other conditions are met.

3. Q: How does this judgment affect taxpayers?

A: It provides relief to taxpayers by clarifying that technical defaults in form filing don't necessarily attract punitive measures under Section 40(a)(ia) (of Income Tax Act, 1961) if the substantive requirements of Section 194C(3) (of Income Tax Act, 1961) are met.

4. Q: What is the importance of Section 194C(3) (of Income Tax Act, 1961) in this case?

A: Section 194C(3) (of Income Tax Act, 1961) provides exclusions from tax deduction liability under certain conditions. This case reinforces the interpretation that meeting these conditions is more important than the procedural aspect of form filing.

5. Q: Does this judgment set a precedent for similar cases?

A: Yes, this judgment aligns with and reinforces previous rulings, particularly from the Gujarat High Court, potentially influencing future decisions in similar cases across India.

1. This appeal is filed by the revenue challenging the order passed by the Income Tax Appellate Tribunal, Bangalore Bench ‘B, Bangalore, dated 26.07.2013 for the Assessment Year 2009-10.

2. The brief facts of the case are that the assessee has filed the return of income for the Assessment Year 2009-10 declaring the total income of Rs.19,07,890/-. Srutiny assessment was completed under Section 143(3) (of Income Tax Act, 1961) (hereinafter referred to as the ‘Act’ for short) on 28.12.2011 by computing the total income of Rs.17,82,64,920/- and while doing the said assessment, the Assessing Officer had added payments made to sub-contractors towards freight charges of Rs.17,63,57,030/- under Section 40(a)(ia) (of Income Tax Act, 1961). Aggrieved by the same, the assessee carried the matter in appeal before the Commissioner of Income Tax (A), Hubli, which was allowed by the Appellate Authority, against which, the revenue preferred an appeal before the ITAT, Bangalore. The Tribunal following the Judgment of Ahmedabad Bench in the case of Valibhai Khanbai Mankad –vs- DCIT (OSD) reported in ITA No.2228/Ahd/2009 dated 29.04.2011, dismissed the appeal filed by the revenue. Aggrieved by the same, the Revenue is in appeal before this Court under Section 260A (of Income Tax Act, 1961).

3. We have heard Sri K.V.Aravind, learned counsel appearing for the Revenue as well as Sri A.Shankar, learned counsel appearing for the assessee. After hearing the parties and perusing the records, the only question that arises for our consideration is:

“Whether non-filing of Form No.15-I/J within the prescribed time is only a technical default or the Provisions of Section 40(a)(ia) (of Income Tax Act, 1961) are attracted?”

Section 40(a)(ia) (of Income Tax Act, 1961) and Section 194C(3) (of Income Tax Act, 1961) reads thus:

“Section 40(a)(ia) (of Income Tax Act, 1961) : Any interest, commission or brokerage, rent, royalty, fees for professional services or fees for technical services payable to a resident, or amounts payable to a contractor or sub-contractor, being resident, for carrying out any work (including supply of labour for carrying out any work), on which tax is deductible at source under Chapter XVII-B and such tax has not been deducted or, after deduction, has not been paid on or before the due date specified in sub-section(1) of Section 139 (of Income Tax Act, 1961)”.

Section 194C(3) (of Income Tax Act, 1961): No deduction shall be made under sub-section(1) or sub-section(2) from –

(i) the amount of any sum credited or paid or likely to be credited or paid to the account of or to the contractor or sub- contractor, if such sum does not exceed twenty thousand rupees: Provided that where the aggregate of the amounts of such sums credited or paid or likely to be credited or paid during the financial year exceeds fifty thousand rupees, the person responsible for paying such sums referred to in sub-s.(1) or as the case may be sub-s.(2) shall be liable to deduct income-tax under this section: Provided further that no deduction shall be made under sub-s.(2) from the amount of any sum credited or paid or likely to be credited or paid during the previous year to the account of the sub-contractor during the course of business of plying, hiring or leasing goods carriages, on production of a declaration to the person concerned paying or crediting such sum in the prescribed form and verified in the prescribed manner and within such time as may be prescribed, if such sub-contractor is an individual who has not owned more than two goods carriages at any time during the previous year: Provided also that the person responsible for paying any sum as aforesaid to the sub-contractor referred to in the second proviso shall furnish to the prescribed IT authority or the person authorized by it such particulars as may be prescribed in such form and within such time as may be prescribed: or

(ii) any sum credited or paid before the 1st day of June, 1972; or

(iii) any sum credited or paid before the 1st day of June, 1973, in pursuance of a contract between the contractor and a co-operative society or in pursuance of a contract between such contractor and the sub-contractor in relation to any work (including supply of labour for carrying out any work) undertaken by the contractor for the co-operative society.”

4. The combined reading of these two provisions make it clear that if there is any breach of requirements of Section 194C(3) (of Income Tax Act, 1961), the question of applicability of Section 40(a)(ia) (of Income Tax Act, 1961) arises. The exclusion provided in Sub-Section(3) of Section 194C (of Income Tax Act, 1961) from the liability to deduct tax at source under sub-section(2) would be complete, the moment the requirements contained therein are satisfied. Once, the declaration forms are filed by the sub- contractor, the liability of the assessee to deduct tax on the payments made to the sub-contractor would not arise. As we have examined, the sub-contractors have filed Form No.15I before the assessee. Such being the case, the assessee is not required to deduct tax under Section 194C(3) (of Income Tax Act, 1961) and to file Form No.15J. It is only a technical defect as pointed out by the Tribunal in not filing Form No.15J by the assessee. This matter was extensively considered by the ITAT, Ahmedabad Bench in Valibhai Khandbai Mankad’s case (supra) and the said Judgment has been upheld by the High Court of Gujarat reported in (2013) 216 Taxman 18 (Guj) wherein it is held that once the conditions of Section 194C(3) (of Income Tax Act, 1961) were satisfied, the liability of the payee to deduct tax at source would cease and accordingly, application of Section 40(a)(ia) (of Income Tax Act, 1961) would also not arise. The Tribunal, placing reliance on the judgment of the ITAT, Ahmedabad Bench, has dismissed the appeal filed by the Revenue. We agree with the said propositions and hold that filing of Form No.15I/J is only directory and not mandatory.

5. In the circumstances, no interference is warranted with the well considered order passed by the Tribunal. Accordingly, no substantial questions of law arises for our consideration and for the forgoing reasons, we dismiss the appeal filed by the Revenue.

Sd/-

JUDGE

Sd/-

JUDGE

×

Similar Ripples

Questions

Tax Deduction Dilemma: Court Rules Filing Form 15I/J is Directory, Not Mandatory

Write your CommentSimilar Posts

Generic

- Reportdata/3859.pdf