Full News

Transfer Pricing Adjustments Limited to International Transactions

Transfer Pricing Adjustments Limited to International Transactions

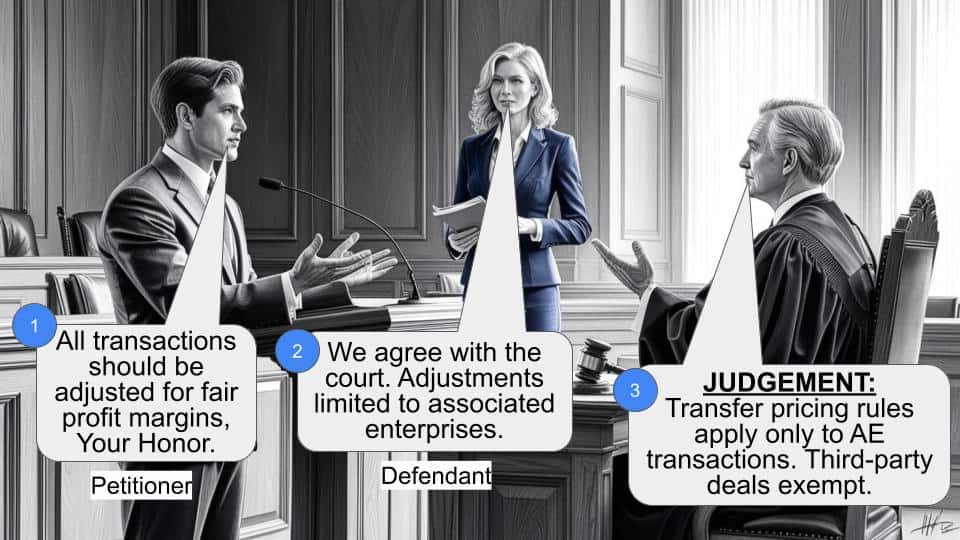

The case involves the Commissioner of Income Tax and Thyssen Krupp Industries India Pvt. Ltd. The main dispute was whether transfer pricing adjustments should apply only to transactions with associated enterprises (AEs) or also to transactions with independent third parties. The court decided that adjustments should only apply to international transactions with AEs, not with unrelated third parties.

Get the full picture - access the original judgement of the court order here

Case Name

Commissioner of Income Tax vs. Thyssen Krupp Industries India Pvt. Ltd. (High Court of Bombay)

Income Tax Appeal No. 2201 of 2013

Date: 2nd December 2015

Key Takeaways

- Scope of Chapter X: The court clarified that Chapter X of the Income Tax Act is applicable only to international transactions with AEs.

- Transfer Pricing Adjustments: Adjustments are not required for transactions with independent third parties as there is no tax avoidance issue.

- Precedent: The decision aligns with previous rulings, reinforcing the limited scope of transfer pricing adjustments.

Issue

Should transfer pricing adjustments be applied to transactions with independent third parties, or are they limited to transactions with associated enterprises?

Facts

Thyssen Krupp Industries India Pvt. Ltd. engaged in international transactions with its AEs, including the import of spares and equipment, royalty payments, and project engineering fees. The Transfer Pricing Officer (TPO) proposed adjustments to the profit margins of all transactions, including those with non-AEs, which the company contested.

Arguments

- Revenue’s Argument: The Revenue argued that the profit margin adjustment should apply to all transactions, not just those with AEs.

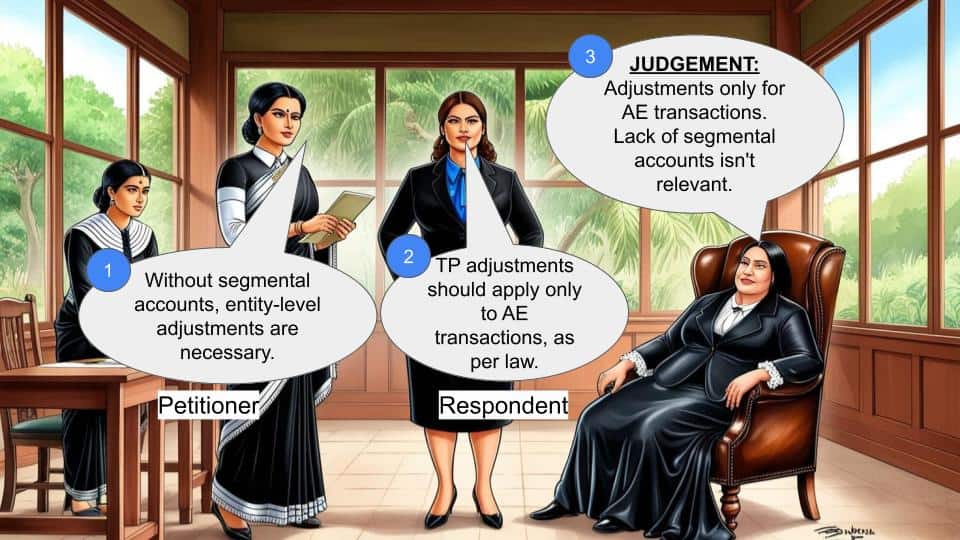

- Assessee’s Argument: Thyssen Krupp contended that adjustments should only apply to transactions with AEs, as per Chapter X of the Income Tax Act.

Key Legal Precedents

- CIT v/s. M/s. Tara Jewels Exports Pvt. Ltd.: This case supported the view that adjustments are limited to transactions with AEs.

- CIT v/s. Keilin Panalfa Ltd.: Another case reinforcing the same principle.

Judgement

The court ruled in favor of Thyssen Krupp Industries, stating that transfer pricing adjustments should only apply to international transactions with AEs. The court emphasized that there is no need for adjustments in transactions with independent third parties as there is no tax avoidance concern.

FAQs

Q: What is the significance of this case?

A: It clarifies that transfer pricing adjustments under Chapter X are limited to transactions with AEs, preventing unnecessary adjustments for transactions with unrelated parties.

Q: Why are transactions with independent third parties excluded?

A: Because there is no issue of tax avoidance in such transactions, making adjustments unnecessary.

Q: How does this decision impact other companies?

A: It provides a clear guideline that only transactions with AEs are subject to transfer pricing adjustments, which can help companies in similar disputes.

1. This Appeal under Section 260 (of Income Tax Act, 1961)A of the Income Tax Act, 1961 (the Act) challenges the order dated 27th November, 2011 passed by the Income Tax Appellate Tribunal (the Tribunal) for the Assessment Year 2007-08.

2. Mr. Kotangale, learned Counsel appearing for the Revenue urges the following reframed questions of law for our consideration:

“(a) Whether on the facts and the circumstance of the case and law, the Tribunal was justified in law in restricting the Transfer Pricing (TP) adjustment only to the transaction between the Associated Enterprises (AEs.)?

(b) Whether on the facts and circumstances of the case and in law, the Tribunal was justified in allowing the payment of royalty, project engineering and manufacturing drawing fees of Rs.11,27,16,302/ disallowed by the Transfer Pricing Officer (TPO).?

(c) Whether on the facts and circumstances of the case and in law, the Tribunal was justified in allowing the payment of liquidated damages of Rs.2,70,38,000/ disallowed by the TPO?”.

3. Re: Question (a)

(a) The Respondent is in the business of execution of turnkey contracts involving design, manufacture, supply, erection and commissioning of sugar plants, cement plants, etc. During the subject Assessment Year, the RespondentAssessee had International Transaction with its Associated Enterprises (AE) in respect of import of spares and equipments, royalty and project engineering, manufacturing drawings, settlement for liquidated damages and interest on delayed payments.

(b) The TPO on selection of comparables arrived at the margin at 6.29% as against 5.19% arrived at by the RespondentAssesse in its Form 3CEB. However, the TPO proposed to make adjustment on account of enhancement of profit margin on all transactions of the RespondentAssessee. This in spite of the RespondentAssessee's objection to the application of the margin applicable to arrive at ALP at 6.29% on transactions with third party i.e. nonAE transactions. The Assessing Officer passed an order in accordance with the above order of the TPO.

(c) Being aggrieved, the assessee carried the above issue in Appeal to the Tribunal. The Tribunal by the impugned order held that only transactions entered into by an assessee with its AE are subject to transfer pricing adjustment and not otherwise. Thus, allowing the Assessee's appeal before it.

(d) The grievance of the Revenue before us is that the adjustment is not to be restricted only in respect of transactions entered into with the AE. All the transactions of the RespondentAssessee would have necessarily be varied/ adjusted by the margin arrived at by the TPO to arrive at the ALP.

(e) We find that in terms of Chapter X of the Act, redetermination of the consideration is to be done only with regard to income arising from International Transactions on determination of ALP. The adjustment which is mandated is only in respect of International Transaction and not transactions entered into by assessee with independent unrelated third parties. This is particularly so as there is no issue of avoidance of tax requiring adjustment in the valuation in respect of transactions entered into with independent third parties. The adjustment as proposed by the Revenue if allowed would result in increasing the profit in respect of transactions entered into with nonAE. This adjustment is beyond the scope and ambit of Chapter X of the Act.

4. A similar view has been taken by this Court in Income Tax Appeal No. 1814 of 2013 (CIT v/s. M/s. Tara Jewels Exports Pvt.Ltd.) decided on 5th October, 2015 as well as by the Delhi High Court in CIT v/s. Keilin Panalfa Ltd. (ITA No.11/2015) decided on 9th September, 2015.

5. In the above view, as the provisions of the Act in respect of transfer pricing are self evident, Question No.(a) as proposed does not give rise to any substantial question of law. Thus, not entertained.

6. Appeal admitted on Question Nos. (b) and (c).

7. Registry is directed to communicate copy of this order to the Tribunal. This would enable the Tribunal to keep papers and proceedings relating to the present appeal available, to be produced when sought for by the Court.

( Dr. SHALINI PHANSALKAR JOSHI,J.) (M.S.SANKLECHA,J.)

×

Similar Ripples

Questions

Transfer Pricing Adjustments Limited to International Transactions

Write your CommentSimilar Posts

Generic

- Reportdata/3269.pdf