Trust's Delay in Registration Appeal Dismissed: Ignorance of Law No Excuse

Full News

Trust's Delay in Registration Appeal Dismissed: Ignorance of Law No Excuse

Trust's Delay in Registration Appeal Dismissed: Ignorance of Law No Excuse

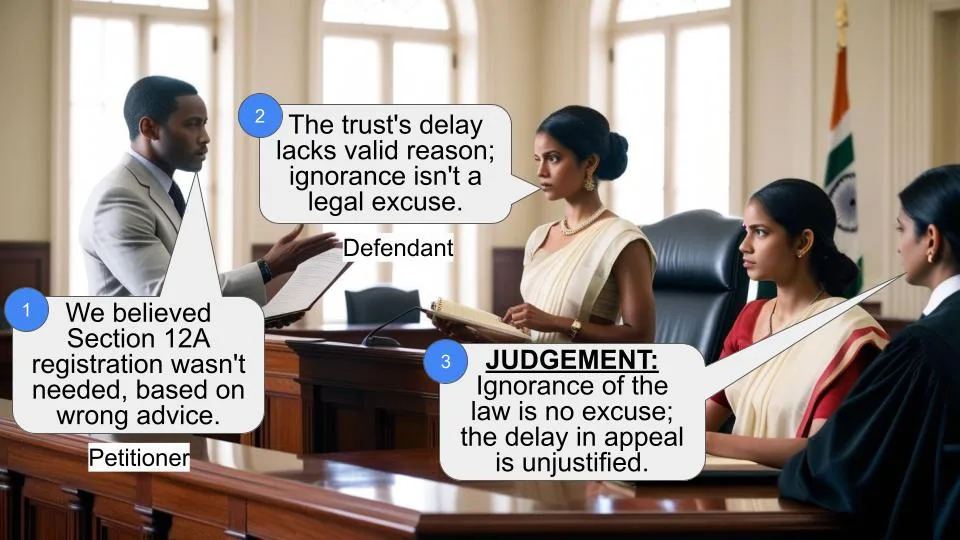

The case involves a trust that appealed against the Income Tax Appellate Tribunal's decision, which dismissed their appeal due to a significant delay in filing. The trust claimed they were under the impression that registration under Section 12A (of Income Tax Act, 1961) was not necessary for tax exemption. The court upheld the Tribunal's decision, emphasizing that ignorance of the law is not a valid excuse for the delay.

Get the full picture - access the original judgement of the court order here

Case Name:

Spporthi Sadan Convent Vs Commissioner of Income Tax (High Court of Karnataka)

ITA No. 100066 of 2015

Date: 17th February 2016

Key Takeaways:

- Ignorance of the law is not a valid excuse for failing to meet legal deadlines.

- The trust failed to provide evidence or substantiate claims of being misadvised.

- The court emphasized the importance of adhering to procedural timelines in legal matters.

Issue

Was the trust's delay in filing the appeal excusable due to their claimed ignorance of the legal requirement for registration under Section 12A (of Income Tax Act, 1961)?**

Facts

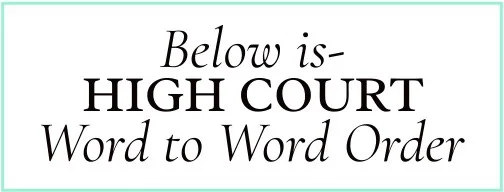

- The appellant, a trust, filed an application for registration under Section 12A (of Income Tax Act, 1961), which was rejected.

- The trust appealed the rejection to the Income Tax Appellate Tribunal with a delay of 997 days.

- The trust claimed they were under the impression that registration was not necessary for tax exemption and that they were wrongly advised.

Arguments

- Appellant (Trust): Argued that they were under a bona fide impression that registration under Section 12A (of Income Tax Act, 1961) was not required and that they were misadvised. They failed to provide evidence or the source of this advice.

- Respondent (Commissioner of Income Tax): Argued that the trust did not provide a valid reason for the delay and that ignorance of the law is not an excuse.

Key Legal Precedents

- The court referenced the case of The Swadeshi Cotton Mills Co. Ltd. vs. The Government of U.P., which established that ignorance of the law is not an excuse for failing to take appropriate steps within the limitation period.

Judgement

The court dismissed the appeal, agreeing with the Tribunal that the trust did not provide sufficient grounds for condoning the delay. The court reiterated that ignorance of the law is not a valid excuse and upheld the Tribunal's decision.

FAQs

Q1: Why was the trust's appeal dismissed?

A1: The appeal was dismissed because the trust failed to provide a valid reason for the 997-day delay in filing the appeal. Ignorance of the law was not accepted as an excuse.

Q2: What was the trust's main argument?

A2: The trust argued that they were under a bona fide impression that registration under Section 12A (of Income Tax Act, 1961) was not necessary for tax exemption and that they were misadvised.

Q3: What does this case mean for other trusts?

A3: This case underscores the importance of understanding legal requirements and adhering to procedural timelines. Trusts must ensure they are properly registered and meet all legal obligations to avoid similar issues.

1. The appellant has called in question the order dated 7/1/2015 in ITA No.168/2014 passed by the Income Tax Appellate Tribunal, Panaji Bench, Panaji (ITAT for short), dismissing the appeal as having been barred by limitation.

2. Heard Sri. S. Parthasarathi, the learned counsel appearing for the appellant and Sri. Y.V. Raviraj, learned counsel appearing for the respondent.

3. It is submitted by the learned counsel for the appellant that, the appellant had filed an application under Section 12A (of Income Tax Act, 1961), for registration of trust. The said application had been rejected vide order dated 24/6/2011 by the Commissioner of Income Tax. This order was challenged before the ITAT. The said appeal was presented with the delay of 997 days. The Tribunal on consideration of the material on record with regard to the delay in filing the appeal has recorded a finding which reads follows:

“The learned AR though vehemently

contended that it was under bonafide impression

that Registration u/s 12A (of Income Tax Act, 1961) was not a condition

precedent for the relief by way of exemption u./s

11 of the Act and that it had been advised

accordingly, but when questioned could not give

the name of the counsel who had advised in this

regard. Even when we asked for the Affidavit of

the concerned person, the ld. AR expressed his

inability to file the same. We were also surprised

to see that the Trust Deed has been notarized

even though the Trust has been created as per the

history given in the Trust Deed for the purpose of

properties of school. In our opinion, a Trust

cannot hold/acquire immovable properties until

and unless it is registered with the Sub-Registrar.

It is not a case where a person has put his

property in the Trust. Although the Trust was

created on 15/3/2010 but the led. AR could not

produce any Income & Expenditure Account and

Balance sheet, audited or otherwise, for the year

ended 31/3/2010, 31/3/2011, 31/3/2012,

31/3/2013 and 31/3/2014. Rather, he explained

his inability to submit the same. If the Assessee

has applied for condonation of delay, the onus is

on the Assessee to explain the reason for each and

every day of the delay. Except submitting that the

Assessee was not aware of the law, he could not

explain the reason for the delay occurred in filing

the appeal”.

4. After recording the aforementioned finding and

adverting to the judgement in the case of Surinder Kumar

Boveja Vs. CWT, 287 ITR 52 (Delhi), the tribunal dismissed

the appeal as having been barred by limitation.

5. A careful perusal of the findings recorded by the

Tribunal clearly points to the fact that the delay was sought

to be explained on two grounds. Firstly, that the trust was

under the bonafide impression that such a registration was

not condition precedent for seeking relief under Section 11 (of Income Tax Act, 1961) of

the Income Tax Act 1961 (‘Act’ for short). Secondly, that the

appellant Trust was advised wrongly. In order to

substantiate the said contention, no material was placed

before the Tribunal. The Tribunal has given sufficient

opportunity to the appellant to substantiate its claim that it

was ill advised by the consultants. With regard to the

requirement of registration, the trust has apparently not

shown any reasonable cause nor answered the queries raised

by the Tribunal during the course of hearing.

6. The learned counsel for the appellant before this Court

has contended that the Tribunal was not justified in

dismissing the application on the ground of limitation and

ought to have noted that to meet ends of substantial justice,

the delay ought to have been liberally construed.

7. This is not a case wherein the appellant is an illiterate

person, who may not know the repercussion in law. Further,

it is the specific case of the appellant that the Trust was

under banafide impression that Registration under Section

12A was not a condition precedent and such impression was

based on advise. But, nonetheless, the appellant neither

chose to reveal the source of such advice nor replied to the

questions posed by the Tribunal. In such circumstances, the

appeal challenging the order of the Tribunal is only a

reiteration of grounds urged before the Tribunal.

8. The learned counsel for the appellant contended that

though the counsel appearing for the appellant offered to

furnish the details sought for by the Tribunal, no time was

granted by the Tribunal. No specific ground is urged in this

behalf in the pleadings either in the form of statement of

facts or affidavit to substantiate such contention.

9. Ignorance of law is no excuse. We may usefully refer to

the judgement of the Hon’ble Supreme Court in the case of

The Swadeshi Cotton Mills Co.Ltd. vs. The Government of

U.P. and Others reported in (1975) 4 SCC 378, wherein it is

held as follows:-

“......But we are in agreement with the High

Court on the other two grounds. As mentioned

earlier, the impugned assessments were made in

1949. The writ petition was filed in 1956. The

explanation given by the petitioner for this long

delay is that he did not know the correct legal

position and he came to know about the same

after the decision of the Allahabad High Court in

the Commissioner of Sales Tax, U.P. Vs. Modi

Food Products Ltd. Every individual is deemed to

know the law of the land. The courts merely

interpret the law and do not make law. Ignorance

of law is not an excuse for not taking appropriate

steps within limitation. Therefore the argument

that the appellant did not know the true legal

position is not one that can be accepted in law.

10. In the circumstances, we are of the considered view

that the appellant has not made out any ground for

condonation of delay of 997 days before the Tribunal. We see

no error in the order passed by the Tribunal. Accordingly,

the appeal fails and stands dismissed.

Sd/-

JUDGE

Sd/-

JUDGE

×

Similar Ripples

Questions

Trust's Delay in Registration Appeal Dismissed: Ignorance of Law No Excuse

Write your CommentSimilar Posts

Generic

- Reportdata/3079.pdf