Unexplained Income: Tribunal Upholds ₹14.2 Lakh Addition

Full News

Unexplained Income: Tribunal Upholds ₹14.2 Lakh Addition

Unexplained Income: Tribunal Upholds ₹14.2 Lakh Addition

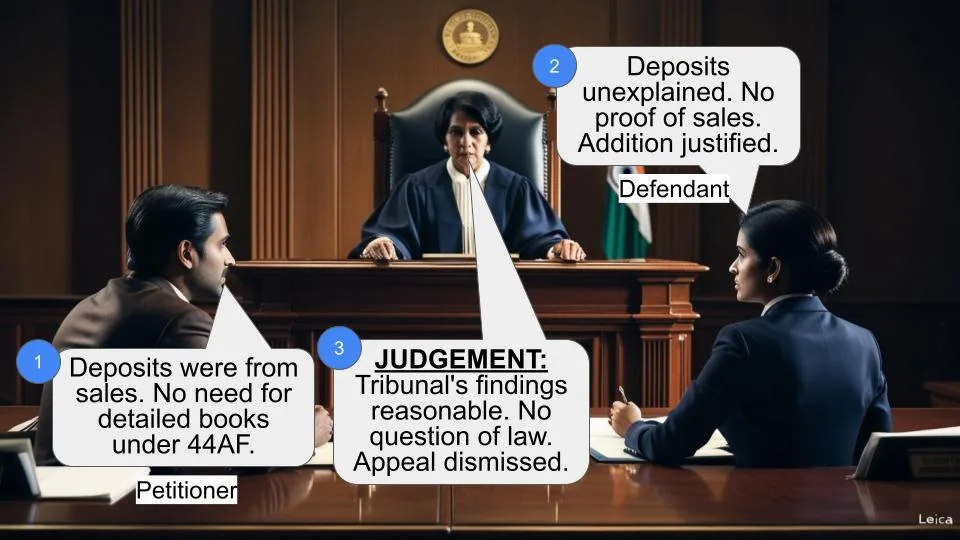

In the case of Kavita Chandra vs. Commissioner of Income Tax (Appeals), the court dealt with the issue of unexplained cash deposits. The Tribunal upheld the addition of ₹14,20,212 as unexplained income, dismissing the assessee’s appeal. The court found that the cash deposits could not be linked to prior withdrawals, as they were made after a significant gap, making them improbable for redeposit.

Get the full picture - access the original judgement of the court order here

Case Name:

Kavita Chandra Vs. Commissioner of Income Tax (Appeals) (High Court of Punjab & Haryana)

ITA No.421 of 2016 (O&M)

Date: 7th March 2017

Key Takeaways:

- The Tribunal upheld the addition of ₹14,20,212 as unexplained income.

- The court emphasized the importance of linking cash withdrawals to deposits.

- The decision highlights the scrutiny on cash flow statements and the necessity for clear documentation.

Issue

Was the addition of ₹14,20,212 as unexplained income justified given the lack of linkage between cash withdrawals and deposits?

Facts

- The assessee, Kavita Chandra, filed a return declaring an income of ₹3,38,680.

- The Assessing Officer assessed the income at ₹45,49,310, including unexplained income.

- The CIT(A) accepted some deposits but rejected others, leading to an addition of ₹14,20,212 as unexplained.

- The Tribunal upheld this addition, noting the improbability of redepositing cash after a gap of two to three months.

Arguments

- Assessee’s Argument: The cash deposits were linked to prior withdrawals and should not be treated as unexplained income.

- Revenue’s Argument: The deposits were made after a significant gap, and the assessee failed to provide a clear linkage, justifying the addition as unexplained income.

Key Legal Precedents

The judgment did not explicitly cite other case laws but relied on the principles of linking cash withdrawals to deposits and the scrutiny of cash flow statements under the Income Tax Act, 1961.

Judgement

The Tribunal dismissed the assessee’s appeal, upholding the addition of ₹14,20,212 as unexplained income. The court found that the cash deposits could not be linked to prior withdrawals due to the time gap, and the cash flow statement lacked relevance without detailed expense documentation.

FAQs

Q1: Why was the cash deposit considered unexplained?

A1: The deposits were made after a significant gap from the withdrawals, and the assessee could not provide a clear linkage or detailed expense documentation.

Q2: What was the outcome for the assessee?

A2: The assessee’s appeal was dismissed, and the addition of ₹14,20,212 as unexplained income was upheld.

Q3: What does this case mean for future tax assessments?

A3: It underscores the importance of maintaining clear documentation and linkage between cash withdrawals and deposits to avoid additions as unexplained income.

1. This appeal has been preferred by the appellant-assessee under Section 260A (of Income Tax Act, 1961) (in short, “the Act”) against the order dated 14.6.2016, Annexure A.4, passed by the Income Tax Appellate Tribunal, Division Bench, Chandigarh (in short, “the Tribunal”) in ITA No.1458/CHD/2010 for the assessment year 2007-08, claiming following substantial questions of law:-

“i) Whether in the present facts and circumstances of the case, the learned ITAT was justified in upholding the addition of 14,20,212/-?

ii) Whether manifest and grave injustice have been done to the appellant by the AO, CIT(A) and/or the ITAT by way of delivering unreasoned and vague order causing him the damage both in terms of monetary as well as non monetary terms, though, earlier, a different decision has been given by ITAT in the similar situation?

iii) Whether the Tribunal to pass judgments/orders on the basis of probability and assumptions?

iv) Whether in the present facts and circumstances of the case, the order of the learned ITAT is perverse?

v) Whether onus be shifted upon the Tribunal or the AO/department for proving that where and in which manner the sum of 14,20,212/- was utilized by the appellant/assessee?

vii) Whether the learned CIT(A) is not justified in upholding addition of ` 14,20,212/- on account of undisclosed sources under section 68 (of Income Tax Act, 1961)/69A of I.T.Act?”

3. A few facts relevant for the decision of the controversy involved as narrated in the appeal may be noticed. The assessee filed her return declaring income at ` 3,38,680/- . The Assessing Officer framed assessment under section 143(3) (of Income Tax Act, 1961) at an income of ` 45,49,310/-after making disallowances on account of telephone and car expenses, difference in the account of Shri Prabhat Chandra, on account of ESI and PF and addition on account of unexplained income. Aggrieved by the order, the assessee filed an appeal before the Commissioner of Income Tax (Appeals)[CIT(A)]. Vide order dated 30.11.2010, Annexure A.3, the CIT(A) deleted the addition on ESI and PF amounting to 14,527/-. With regard to disallowance out of telephone and car expenses of ` 70,884/-, the CIT(A) reduced the amount to 10% amounting to ` 35,442/-. The appeal was rejected qua disallowance of 5000/- as difference in the account of Shri Prabhat Chandra. Out of 41,20,212 on account of unexplained income, the CIT(A) accepted 27 lacs deposited by the assessee. However, balance cash flow statement was rejected on the ground that ` 14,20,200/- had been deposited after a gap of 2-3 months so the same could not be available for redeposit. Thus, the appeal was partly allowed. Aggrieved by the order, both the assessee and the department filed appeals before the Tribunal. Vide order dated 14.6.2016, the Tribunal dismissed the appeal filed by the assessee. The appeal filed by the revenue was dismissed as not pressed. Hence the instant appeal by the assessee.

4. We have heard learned counsel for the appellant-assessee.

5. After examining the entire evidence on record, the Tribunal has upheld the finding recorded by CIT(A) with regard to cash deposit to the tune of ` 14,20,212/- as unexplained. It has been categorically recorded by the Tribunal that out of the 33 withdrawals, only two withdrawals of 2 lacs each from Bank of Rajasthan and ICICI Bank were made in cash. The rest were all withdrawals by cheque – small amounts made mostly by an employee of the assessee. Similarly, in many cases, small amounts were withdrawn two or three times on a single day by different persons.

Further,the deposits in Bank were made after a gap of two-three instances of withdrawals. Taking the totality of facts and circumstances of the case, the Tribunal concurred with the findings recorded by the CIT(A) that the withdrawals were for the purpose of business and not available for redeposit.

Further, the withdrawals were re-deposited after a gap of two or three months which was not probable. Thus, the assessee was not able to link the cash withdrawn from the bank with the cash deposit. Consequently, the finding of the CIT(A) with regard to treating the cash deposit of 14,20,212/- as unexplained income of the assessee was upheld by the Tribunal. Thus, the appeal of the assessee was dismissed. With regard to deleting the addition of ` 2 lacs, the appeal filed by the revenue was dismissed as not pressed as according to the CBDT circular dated 10.12.2015, the appeals before the Tribunal below the specified tax limit i.e. 10 lacs were to be withdrawn. The relevant findings recorded by the Tribunal read thus:-

“15. It is evident from the above that the learned CIT(A) has lucidly brought out that the cash deposits remained unexplained. As per the cash flow statement submitted by the assessee and reproduced at page 7-8 of the CIT(A) order, there were in all 14 instances of cash deposited in the two banks and in the books of CBM Engineering on various dates, while withdrawals from banks was shown in 33 instances. Out of the 33 withdrawals, only two withdrawals of ` 2 lacs each from bank of Rajasthan and ICICI Bank was made in cash. The rest were all withdrawals by cheque small amounts made mostly by Shri Dushyant Singh an employee of the assessee. Moreover, as pointed out by the learned CIT(A) in many cases small amounts were withdrawn 2 or 3 times on a single day by different persons. Further the deposits in Bank were made after a gap of 2-3 instances of withdrawals.

Considering the totality of facts of the case and the surrounding circumstances we concur with the learned CIT(A) that the withdrawals were for the purpose of business and not available for redeposit.

16. Moreover, we also agree with the learned CIT(A) that in the absence of any detail of expenses incurred by the assessee in this period the cash flow statement has no relevance and the entire withdrawal cannot be said to have been redeposited. Moreover as held by the learned CIT(A) the withdrawals have been found to be subsequently redeposited after a gap of two or three months which is not probable. The assessee therefore we find has not been able to link the cash withdrawn from the bank with cash deposit we therefore uphold the order of the learned CIT(A) treating the cash deposit of ` 14,20,212/- as unexplained income of the assessee.

17. In view of the above, ground No. 1 and 2 of the assessee are dismissed.”

6. The findings recorded by the CIT(A) as well as the Tribunal are pure findings of fact which have not been shown to be illegal or perverse by the learned counsel for the appellant-assessee warranting interference by this Court. In the light of the conclusion recorded hereinbefore, the judgment of this Court in Shiv Charan Dass vs. CIT, (1980) 126 ITR 263 relied upon by the learned counsel for the appellant being based on individual fact situation involved therein does not come to the rescue of the appellant. Thus, no substantial question of law arises. Consequently, the appeal stands dismissed. In view of dismissal of the appeal on merits, the issue of condonation of 40 days delay in filing the appeal is left open.

(Ajay Kumar Mittal)

Judge

March 07, 2017 (Ramendra Jain)

‘gs’ Judge

Whether reasoned/speaking order Yes/No

Whether reportable Yes/No

×

Similar Ripples

Questions

Unexplained Income: Tribunal Upholds ₹14.2 Lakh Addition

Write your CommentSimilar Posts

Generic

- Reportdata/HC-PH-421-2016.pdf