Court Dismisses Appeal on Section 10B (of Income Tax Act, 1961) Tax Deduction D…

Full News

Court Dismisses Appeal on Section 10B (of Income Tax Act, 1961) Tax Deduction Dispute

Court Dismisses Appeal on Section 10B (of Income Tax Act, 1961) Tax Deduction Dispute

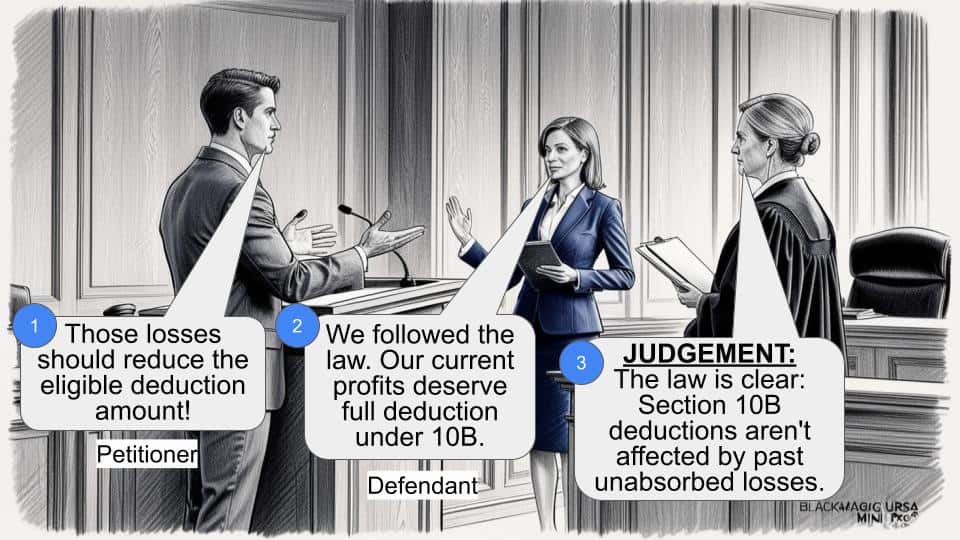

The case involves the Commissioner of Income Tax challenging a decision by the Income Tax Appellate Tribunal regarding the application of Section 10B (of Income Tax Act, 1961). The main issue was whether unabsorbed losses and depreciation from a 100% Export Oriented Unit (EOU) could be set off against current profits for tax deduction purposes. The court upheld the Tribunal’s decision, dismissing the appeal and siding with the taxpayer.

Case Name

Commissioner of Income Tax vs. Techno Tarp and Polymers Pvt. Ltd. (High Court of Bombay)

Income Tax Appeal No. 2134 of 2013

Date: 5th December 2015

Key Takeaways

- The court confirmed that changes in Section 10B (of Income Tax Act, 1961) from providing an exemption to a deduction affect how profits and losses are treated.

- The decision reinforces the precedent set by the case “CIT Vs. Black & Veatch Consulting § Ltd.”

- The ruling clarifies that unabsorbed losses from previous years cannot be set off against current profits for deduction under the amended Section 10B (of Income Tax Act, 1961).

Issue

Can unabsorbed losses and depreciation from a 100% EOU be set off against current profits for tax deduction under Section 10B (of Income Tax Act, 1961)?

Facts

- The case revolves around the interpretation of Section 10B (of Income Tax Act, 1961), which changed from providing an exemption to a deduction for profits from 100% EOUs.

- The dispute arose for the Assessment Year 2009-10.

- The Revenue challenged the Tribunal’s decision that favored the taxpayer, Techno Tarp and Polymers Pvt. Ltd.

Arguments

- Revenue’s Argument: The Revenue argued that the unabsorbed losses and depreciation should be set off against the current year’s profits, affecting the deduction under Section 10B (of Income Tax Act, 1961).

- Taxpayer’s Argument: The taxpayer, supported by the Tribunal’s decision, argued that the current profits should be eligible for deduction without being reduced by past unabsorbed losses.

Key Legal Precedents

- CIT Vs. Black & Veatch Consulting § Ltd.: This case was pivotal in the court’s decision, establishing that unabsorbed losses should not affect the deduction under the amended Section 10B (of Income Tax Act, 1961).

- Ganesh Polychem Ltd. Vs. ITO: Supported the same interpretation as Black & Veatch, reinforcing the taxpayer’s position.

Judgement

The court dismissed the appeal, siding with the taxpayer. It held that the Tribunal was correct in its interpretation that unabsorbed losses and depreciation should not be set off against current profits for the purpose of deduction under Section 10B (of Income Tax Act, 1961). The decision was based on the precedent set by “CIT Vs. Black & Veatch Consulting § Ltd.”

FAQs

Q: What does this decision mean for 100% EOUs?

A: It means that for tax purposes, current profits can be deducted under Section 10B (of Income Tax Act, 1961) without being reduced by past unabsorbed losses.

Q: Why was the Revenue’s appeal dismissed?

A: The appeal was dismissed because the court found that the Tribunal’s decision was consistent with established legal precedents.

Q: How does this affect future tax assessments?

A: This decision clarifies the application of Section 10B (of Income Tax Act, 1961), ensuring that similar cases will follow the same interpretation regarding deductions and unabsorbed losses.

1. This Appeal under Section 260 (of Income Tax Act, 1961)A of the Income Tax Act,1961 (the Act), challenges the order dated 1 March 2013 passed by the Income Tax Appellate Tribunal (the Tribunal) for the Assessment year 2009-10.

2. Although numerous questions of law have been formulated in the Memo of Appeal, Mr. Suresh Kumar, learned Counsel for the Revenue urges only the following reframed question of law for our consideration as under:

“(i) Whether on the facts and in the circumstances of the case and in law, the Tribunal was justified in holding that the brought forward unabsorbed loss/ depreciation of the assessee's 10B unit was not liable for set off against the current year's profit of the same 10B unit ?”

2. We find that the impugned order of the Tribunal has allowed the respondent Assessee's appeal by following the decision of this Court in “CIT Vs. Black & Veatch Consulting (P) Ltd., ((2012) 208 Taxman 144)”. Further the impugned order also placed reliance upon its own decision in the case of “Ganesh Polychem Ltd. Vs. ITO” decided in ITA No.8515/Mum/2010 on 10 August 2012 for the Assessment Year 200607 following the decision of this Court in Black & Veatch Consulting(P) Ltd.(supra).

3. The Revenue had carried the decision of the Tribunal in “Ganesh Polychem Ltd. Vs. ITO” (supra) to this Court being Income Tax Appeal (Lodg) No.2083 of 2012 raising the following question of law:

“Whether on the facts and in the circumstances of the case and in law the Tribunal was right in holding that the brought forward unabsorbed depreciation and losses of the unit, the income of which is not eligible for deduction u/s.10B (of Income Tax Act, 1961) cannot be set off against the current profit of the eligible unit for computing the deduction u/s.10B (of Income Tax Act, 1961) ?”

This Court by order dated 25 February 2013 dismissed the Revenue's above appeal as it was agreed that the issue raised therein stands concluded against the Revenue by the decision of this Court in Black & Veatch Consulting(P) Ltd.(supra).

4. Mr.Suresh Kumar, learned Counsel for the Revenue does not dispute that the question as framed is covered by the decision of this Court in Black & Veatch Consulting(P) Ltd.(supra) & “Ganesh Polychem Ltd. Vs. ITO” (supra). However, he submits that the question as framed would require consideration as the contrary view taken by Karnataka High Court in “CIT Vs. Himatasingike Seide Ltd., ((2006)156 Taxman 151 (Kar.))” has now been upheld by the Apex Court in its order dated 19 September 2013 as under:

“1. We have heard the learned Counsel for the parties to the lis.

2. Having perused the records and in view of the facts and circumstances of the case, we are of the opinion that the Civil Appeal being devoid of any merit deserves to be dismissed and is dismissed accordingly. Ordered accordingly.”

5. We find that the decision of the Karnataka High Court in Himatasingike Seide Ltd. (supra) which was undisturbed by the Apex Court was in resepct of Assessment Year 199495. Thus it dealt with the provisions of Section 10B (of Income Tax Act, 1961) as existing prior to 1 April 2001 which was admittedly different from Section 10B (of Income Tax Act, 1961) as in force during Assessment Year 200910 involved in this appeal. Section 10B (of Income Tax Act, 1961) as existing prior to 1 April 2001 provided for an exemption in respect of profits and gains derived from export by 100% Export Oriented Undertakings and now it provides for deduction of profits and gains derived from a 100% Exported Oriented Units..

6. In any view of the matter, the decision of the Karnataka High Court in Himatasingike Seide Ltd. (supra) which was undisturbed by the Apex Court dealt with the provision of law different from that which was dealt with in the impugned Order. A decision has to be considered in the context of the law as arising for consideration and a change in law would render the decision under the old law inapplicable while considering the amended law.

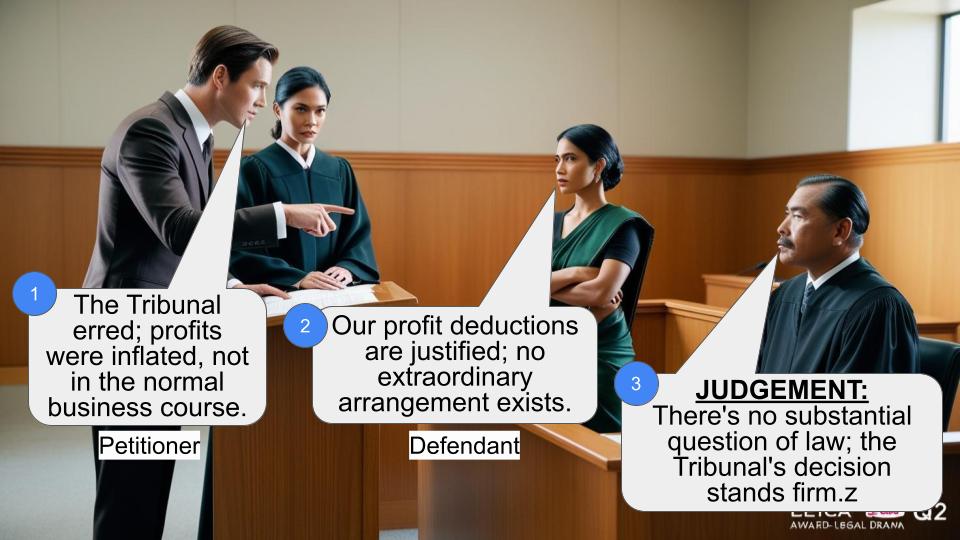

7. The issue as raised stands concluded by the decision of this Court in Black & Veatch Consulting(P) Ltd.(supra) and “Ganesh Polychem Ltd. Vs. ITO” against the Revenue. Therefore, the question of law as proposed for our consideration does not give rise to any substantial question of law.

8. Accordingly, the appeal is dismissed. No order as to costs.

(G.S.KULKARNI, J.) (M.S. SANKLECHA, J.)

×

Similar Ripples

Questions

Court Dismisses Appeal on Section 10B (of Income Tax Act, 1961) Tax Deduction Dispute

Write your CommentSimilar Posts

Generic

- Reportdata/3262.pdf