Full News

Court Upholds Dismissal of Tax Appeal Due to Inordinate Delay

Court Upholds Dismissal of Tax Appeal Due to Inordinate Delay

This case involves Ajmeer Sherriff and Co. (the appellant) challenging an order by the Income Tax Appellate Tribunal that dismissed their appeal due to a 754-day delay in filing. The High Court upheld the Tribunal's decision, finding no substantial question of law in the appellant's case.

Get the full picture - access the original judgement of the court order here.

Case Name:

Ajmeer Sherriff and Co. vs Income Tax Officer (High Court of Madras)

Tax Case (Appeal) No.529 of 2014

Key Takeaways:

1. Courts maintain a strict approach to inordinate delays in filing appeals.

2. The "sufficient cause" for delay must be substantiated with detailed explanations.

3. In partnership firms, the illness of one partner is not a sufficient excuse when other partners could have acted.

4. The court emphasizes the need for a balance between liberal interpretation and adherence to legal principles.

Issue:

Whether the Income Tax Appellate Tribunal was correct in dismissing the appeal on the ground of limitation despite the Managing Partner's alleged medical complications?

Facts:

1. The case relates to the assessment year 2007-2008.

2. Ajmeer Sherriff and Co. is a firm engaged in running lorries on a contract basis.

3. The Assessing Officer disallowed certain expenditures claimed by the assessee.

4. The Commissioner of Income Tax (Appeals) partially upheld the Assessing Officer's order.

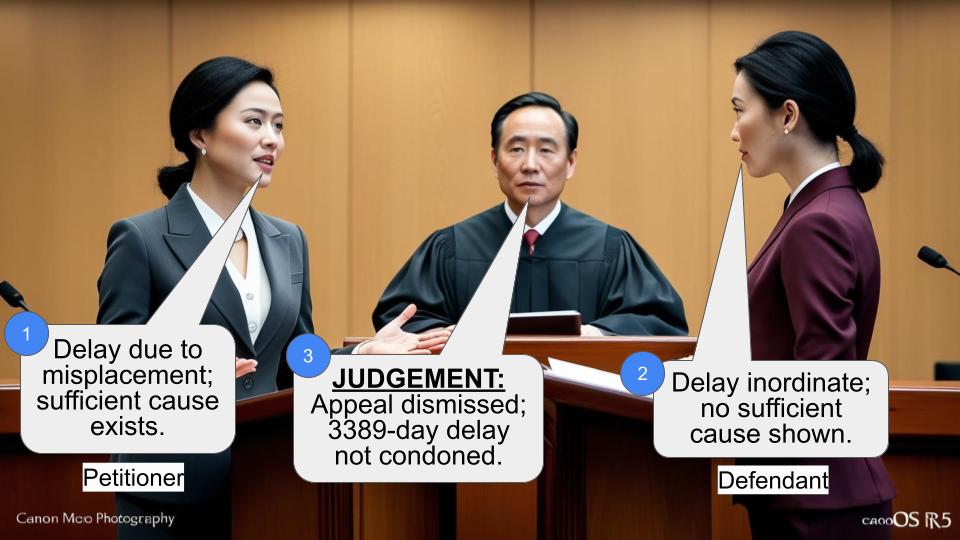

5. The assessee filed an appeal to the Income Tax Appellate Tribunal with a 754-day delay.

6. The Tribunal dismissed the appeal, declining to condone the delay.

7. The assessee then appealed to the High Court.

Arguments:

1. Appellant's Argument:

- The Managing Partner had multiple medical complications, justifying the delay.

- The term "sufficient cause" should receive liberal interpretation by the courts.

2. Respondent's Argument:

- The delay was inordinate and requires a strict approach.

Key Legal Precedents:

1. Esha Bhattacharjee v. Managing Committee of Raghunathpur, Nafar Academy and others (2013 (5) CTC 547):

- Outlined principles for considering applications for condonation of delay.

- Emphasized a balance between liberal interpretation and adherence to legal principles.

Judgement:

1. The High Court dismissed the appeal, finding no substantial question of law.

2. The court agreed with the Tribunal's decision not to condone the delay, citing:

- The appellant's lackadaisical approach and nonchalant manner in seeking condonation.

- Insufficient explanation for the delay, with medical records showing only intermittent short-term treatments.

- The presence of other partners who could have filed the appeal in time.

FAQs:

Q1: Why did the court not accept the medical complications as a valid reason for delay?

A1: The medical records showed only intermittent short-term treatments, not continuous complications. Moreover, other partners could have filed the appeal.

Q2: What is the significance of "sufficient cause" in such cases?

A2: "Sufficient cause" is interpreted liberally, but must be substantiated with detailed explanations and cannot be used to cover gross negligence.

Q3: How does this judgment impact future cases involving delays in filing appeals?

A3: It reinforces the need for a balanced approach, considering both liberal interpretation and adherence to legal principles, especially in cases of inordinate delay.

Q4: What should taxpayers learn from this case?

A4: Taxpayers should be diligent in filing appeals within the stipulated time and provide comprehensive, genuine reasons if seeking condonation of delay.

This Tax Case (Appeal) has been filed by the assessee, challenging the order passed by the Income Tax Appellate Tribunal dated 09.10.2013 declining to condone the delay of 754 days in filing the appeal, raising the following substantial questions of law:

"1. Whether the Appellate Tribunal is correct in law in dismissing the appeal on the ground of limitation in spite of the Managing Partner's continuing multiple medical complications shown as the reason in the affidavit filed in support of the plea for condonation of delay in filing the said appeal before them?

2. Whether the Appellate Tribunal is correct in law for not condoning the delay in filing the appeal before them to challenge the unreasonable and wrong disallowances which resulted in additions in the computation of taxable total income by the respondent upon overlooking the binding principles laid down by the Apex Court reported in 167 ITR 461?

3. Whether the Appellate Tribunal is correct in law for not considering the grounds of appeal formed part of statutory Form No.36 in challenging the wrong addition made in the computation of taxable total income even though the said disallowances were challenged on various legal facets?"

2. The brief facts of the case are as follows:

The assessment in this case relates to the assessment year 2007-2008. The assessee is a firm engaged in the business of running of lorry on contract basis. The assessee had filed its return of income for the assessment year in question disclosing income of Rs.2,83,653/- The Assessing Officer while completing the assessment disallowed the entire freight expenditure and 50% of the miscellaneous expenditure claimed by the assessee. As against the said order of the Assessing Officer, the assessee filed an appeal before the Commissioner of Income Tax (Appeals), who, by order dated 27.12.2010, upheld the order of the Assessing Officer except reducing the disallowance of miscellaneous expenditure at 25%. As against the said order of the Commissioner of Income Tax (Appeals) dated 27.12.2010, the assessee preferred an appeal before the Income Tax Appellate Tribunal with a delay of 754 days. The Tribunal, by order dated 9.10.2013, dismissed the appeal holding that the explanation offered by the assessee was not satisfactory. Aggrieved by the said order of the Tribunal declining to condone the delay, the assessee is before this Court.

3. Heard learned counsel appearing for the assessee and the learned Standing Counsel appearing for the Revenue and perused the materials placed before this Court.

4. It is seen that as against the order passed by the Commissioner of Income Tax (Appeals) dated 27.12.2010, the assessee had filed an appeal before the Income Tax Appellate Tribunal along with a petition to condone the delay of 754 days in filing the appeal. The Tribunal, while dismissing the petition, has reasoned that, (a) the allegation regarding ill-health and multiple medical complications is bereft of details and as required by law, every days delay has not been explained; and (b) even assuming that the reason is true, the appellant is a firm containing four partners and therefore, even if one of the partner was not well, the other partners could have taken steps to file the appeal in time and therefore, there is no justification to condone the delay.

5. The justification of this order is under challenge in this appeal.

6. The contention of the learned counsel for the appellant is that the term “sufficient cause” has always received liberal interpretation by the Courts and sought indulgence of this Court in setting aside the order declining to condone the delay.

6.1. Per contra, the learned Standing Counsel for the respondent submitted that the delay is not of a short duration, but inordinate and therefore, strict approach is called for.

7. The contentions raised on both sides have to be considered in the light of the facts pleaded / placed.

8. Admittedly, the appellant is a partnership firm consisting of four partners. Moreover, one of the partner is stated to be the son of the Managing Partner. Though the medical terminology used in the affidavit, i.e., continuing multiple medical complications, gives an impression that the Managing Partner should have been under continuous treatment, the discharge summaries, dated 10.09.2010, 08.07.2011, 15.09.2011 and 22.7.2013 would show that the Managing Partner had been on treatment for a very short duration for an intermittent period. It would not have been difficult for the Managing Partner if really he had been diligent to file the appeal in time. Even assuming that he was on continuous medical treatment, the son or other partners should have been diligent in taking up the responsibility in filing the appeal in time. Therefore, when the conduct on the part of the appellant exhibited gross negligence / procrastinating attitude and incorrect grounds, the Income Tax Appellate Tribunal rightly dismissed the petition to condone the delay.

9. The principles involved and the approach needed while considering the application for condonation of delay has been highlighted in the decision reported in 2013 (5) CTC 547 (Esha Bhattacharjee V. Managing Committee of Raghunathpur, Nafar Academy and others, and the relevant portions are extracted for convenient reference:-

"15. From the aforesaid authorities the principles that can broadly be culled out are:

i) There should be a liberal, pragmatic, justice- oriented, non- pedantic approach while dealing with an application for condonation of delay, for the courts are not supposed to legalise injustice but are obliged to remove injustice.

ii) The terms "sufficient cause" should be understood in their proper spirit, philosophy and purpose regard being had to the fact that these terms are basically elastic and are to be applied in proper perspective to the obtaining fact situation.

iii) Substantial justice being paramount and pivotal the technical considerations should not be given undue and uncalled for emphasis.

iv) No presumption can be attached to deliberate causation of delay but, gross negligence on the part of the counsel or litigant is to be taken note of.

v) Lack of bona fides imputable to a party seeking condonation of delay is a significant and relevant fact.

vi) It is to be kept in mind that adherence to strict proof should not affect public justice and cause public mischief because the courts are required to be vigilant so that in the ultimate eventuate there is no real failure of justice.

vii) The concept of liberal approach has to encapsule the conception of reasonableness and it cannot be allowed a totally unfettered free play.

viii) There is a distinction between inordinate delay and a delay of short duration or few days, for to the former doctrine of prejudice is attracted whereas to the latter it may not be attracted. That apart, the first one warrants strict approach whereas the second calls for a liberal delineation.

ix) The conduct, behaviour and attitude of a party relating to its inaction or negligence are relevant factors to be taken into consideration. It is so as the fundamental principle is that the courts are required to weigh the scale of balance of justice in respect of both parties and the said principle cannot be given a total go by in the name of liberal approach.

x) If the explanation offered is concocted or the grounds urged in the application are fanciful, the courts should be vigilant not to expose the other side unnecessarily to face such a litigation.

xi) It is to be borne in mind that no one gets away with fraud, misrepresentation or interpolation by taking recourse to the technicalities of law of limitation.

xii) The entire gamut of facts are to be carefully scrutinized and the approach should be based on the paradigm of judicial discretion which is founded on objective reasoning and not on individual perception.

xiii) The State or a public body or an entity representing a collective cause should be given some acceptable latitude."

10. We find that the appellant in the present case has been lackadaisical in their approach and in a nonchalant manner they have tried to seek condonation of delay. The Supreme Court in the decision referred supra has deprecated the practice of showing leniency in unwarranted fact situation. The parameters laid down by the Supreme Court as to when the delay should not be condoned get squarely attracted to the facts of the present case and therefore, we find no reason to condone the delay. The Tribunal was correct in dismissing the appeal on that score.

11. In the light of the above, we find no question of law much less any substantial question of law arises for consideration in this appeal. Accordingly, this Tax Case (Appeal) stands dismissed. No costs.

Index: Yes / No (R.S.,J.) (S.V.,J.)

Internet: Yes / No 02.02.2015

To

1. The Income Tax Appellate Tribunal, Madras 'A' Bench.

R.SUDHAKAR,J.

AND

S.VIMALA, J.,

×

Similar Ripples

Questions

Court Upholds Dismissal of Tax Appeal Due to Inordinate Delay

Write your CommentSimilar Posts

Generic

- Reportdata/4052.pdf