Full News

Court Upholds Genuine Diamond Sales, Rejects Tax Authority's Skepticism

Court Upholds Genuine Diamond Sales, Rejects Tax Authority's Skepticism

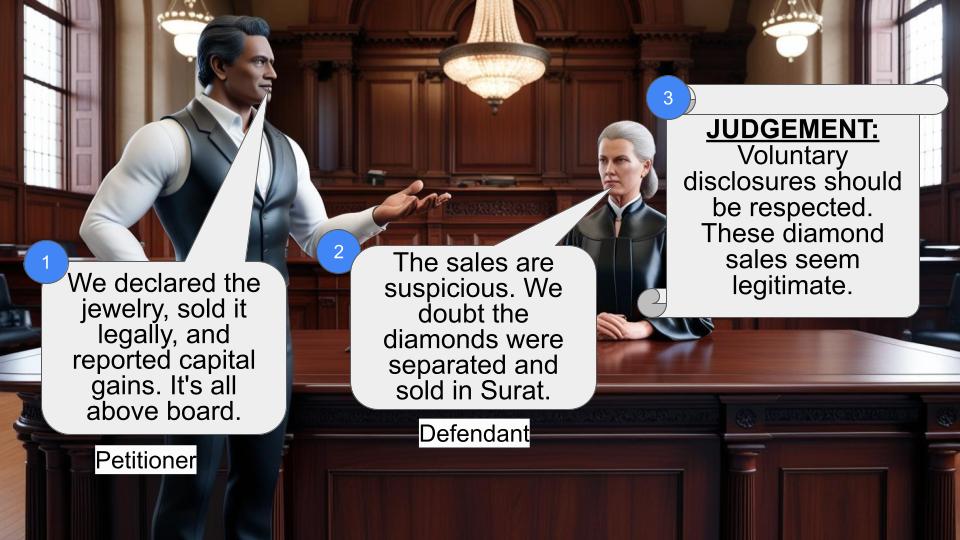

It's about three taxpayers from the same family who sold some diamonds they had previously declared under a voluntary disclosure scheme. The tax authority didn't believe the sales were genuine and tried to tax the proceeds as unexplained income. But guess what? The court sided with the taxpayers, saying the sales were legit. Pretty cool, right?

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Tilak Raj Kumar

I.T.T.A.Nos.120, 132 & 229 of 2003

Date: 16 September 2014

Key Takeaways:

1. The court emphasized that voluntary disclosures of wealth should be respected by tax authorities.

2. Showing sale proceeds as 'capital gains' adds credibility to the transaction.

3. Tax authorities shouldn't subject taxpayers to excessive scrutiny akin to criminal investigations.

4. The court highlighted the importance of reasonable assessment practices by tax authorities.

Issue:

The main question here was: Were the diamond sales claimed by the assessees genuine transactions, or could the proceeds be treated as unexplained cash credits under Section 68 (of Income Tax Act, 1961)?

Facts:

Alright, let's break this down:

1. Three family members (including an HUF) declared jewelry (gold and diamonds) under the Voluntary Disclosure of Income Scheme (VDIS).

2. They later sold this jewelry, with gold sold in Hyderabad and diamonds in Surat.

3. They reported the sale proceeds as 'capital gains' in their tax returns for the 1998-99 assessment year.

4. The Assessing Officer accepted the gold sales but doubted the diamond sales in Surat.

5. The officer treated the diamond sale proceeds as 'unexplained cash credits' under Section 68 (of Income Tax Act, 1961).

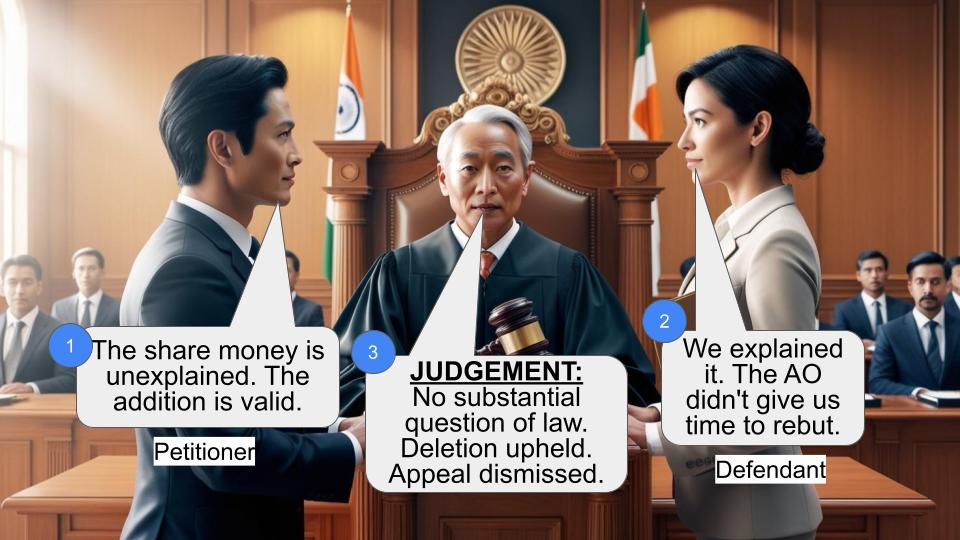

6. The taxpayers appealed, lost at the first level, but won at the Income Tax Appellate Tribunal.

7. The tax department then appealed to the High Court, which is what we're looking at now.

Arguments:

Tax Department's Side:

- Doubted the separation of diamonds from jewelry and the actual sale in Surat.

- Questioned the taxpayers' travel to Surat for the transactions.

- Treated the sale proceeds as unexplained cash credits under Section 68 (of Income Tax Act, 1961).

Taxpayers' Side:

- Claimed the sales were genuine and provided details of buyers and payment methods.

- Argued that the diamonds were part of the jewelry declared in VDIS.

- Pointed out that they had reported the proceeds as 'capital gains' in their tax returns.

Key Legal Precedents:

Interestingly, this judgment doesn't cite specific legal precedents. Instead, it focuses on the facts of the case and the principles of reasonable tax assessment.

Judgement:

The court ruled in favor of the taxpayers. Here's the gist:

1. The court found it reasonable that expensive jewelry would include diamonds.

2. It accepted that the diamonds were sold in Surat, a known diamond trading hub.

3. The court criticized the tax authority's excessive scrutiny, likening it to a criminal investigation.

4. It emphasized that voluntary disclosures and reporting of capital gains add credibility to the transactions.

5. The court dismissed the tax department's appeals, upholding the Tribunal's decision.

FAQs:

Q1: Why did the court side with the taxpayers?

A1: The court found the taxpayers' explanations reasonable and criticized the tax authority's excessive scrutiny.

Q2: What's the significance of the Voluntary Disclosure of Income Scheme (VDIS) in this case?

A2: The VDIS declarations added credibility to the taxpayers' claims about owning and selling the diamonds.

Q3: Why was the sale of diamonds in Surat important?

A3: Surat is a major diamond trading hub, making it a logical place for such transactions.

Q4: What's the takeaway for tax authorities from this judgment?

A4: The court suggests that tax authorities should be more reasonable in their assessments and not subject taxpayers to excessive scrutiny.

Q5: Does this case set a precedent for similar situations?

A5: While it doesn't establish new legal principles, it does emphasize the importance of respecting voluntary disclosures and reasonable tax assessment practices.

These three appeals arise under similar circumstances, and the respondents are from the same family. Hence, they are disposed of through a common order.

The respondent in I.T.T.A.No.132 of 2003 is the Hindu Undivided Family (HUF). The respondent in I.T.T.A.No.229 of 2003 is the Karta of the family, who, in turn, is an independent assessee. Similarly, the respondent in I.T.T.A.No.120 of 2003 is a member of the HUF, and he is also an independent assessee. All the three assesses have availed the benefit under “Voluntary Disclosure of Income Scheme (VDIS)” and declared items, which are mostly of jewellery, namely gold and diamonds. For example, the value of gold declared by the Kartha of the Family, by name Harish Kumar, was Rs.2,64,040/-, and that of diamonds - Rs.16,38,700/-. Similarly, the value of the gold disclosed by the other assessee, Tilak Raj Kumar, was Rs.1,57,028/- and that of diamonds - Rs.1,16,000/-. Certificates of disclosure were also furnished to them.

All the three assesses are said to have sold away the jewellery declared by them under the VDIS. While the gold is said to have sold at Hyderabad, the diamonds are said to have been separated from the ornaments and sold at Surat. The sale proceeds of the jewellery were shown in the respective returns, as ‘capital gains’, for the assessment year 1998-99. The Assessing Officer believed the transaction of sale of gold at Hyderabad, but doubted the genuinity of sale of diamonds at Surat. After conducting a detailed enquiry, he disbelieved that, and treated the amount shown as sale proceeds of diamonds in all the three assessments, as ‘unexplained cash credit’, in the respective orders of assessment, passed by him. The respondents carried the matter in appeal to the Commissioner of Income Tax (Appeals)-V, Hyderabad. The appeals were dismissed through separate orders passed in the year 2002. Thereupon, the respondents filed I.T.A.Nos.212, 271 and 272/Hyd/2002, respectively, before the Hyderabad Bench ‘B’ of the Income Tax Appellate Tribunal (for short ‘the Tribunal’). The Tribunal allowed I.T.A.No.212 of 2002 through order, dated 31.05.2002, and I.T.A.Nos.271 and 272 through separate orders, dated 07.06.2002. Hence, these three appeals under Section 260A (of Income Tax Act, 1961) (for short ‘the Act’), by the Revenue.

The following questions of law are urged:

1. Whether on the facts and in the circumstances of the case the Tribunal is correct in law in holding that the alleged sale transaction of diamonds worth Rs.12,73,028/- as claimed by the assessee is a genuine transaction?

2. Whether on the facts and in the circumstances of the case, the Tribunal is correct in law in holding that the amount of Rs.12,73,028/- cannot be added u/s.68 (of Income Tax Act, 1961)?

3. Whether on the facts and in the circumstances of the case the Tribunal is correct in directing the Assessing Officer not aggregate the sum of Rs.2,10,000/- being the assessee’s share from M/s. Basant Farms for rate purposes?”

1. Whether on the facts and in the circumstances of the case the Tribunal is correct in law in holding that the alleged sale transaction of diamonds worth Rs.51,92,750/- as claimed by the assessees, is a genuine transaction?

2. Whether on the facts and in the circumstances of the case, the Tribunal is correct in law in holding that the amount of Rs.51,92,750/- cannot be added u/s.68 (of Income Tax Act, 1961)?

3. Whether on the facts and in the circumstances of the case the Tribunal is correct in directing the Assessing Officer not to add aggregate the sum of Rs.3,75,000/-, each, being the assessees’ share from M/s. Basant Farms for rate purposes?”

Heard the learned counsel for the appellant and learned counsel for the respondents.

It is a matter of record that all the three assesses made separate voluntary disclosures of their income, in response to a scheme and they were also issued the certificates. Most of the items mentioned in the disclosures are jewellery of gold and diamonds. For one reason or the other, the family thought of selling away the jewellery. In the process, the diamonds were separated from gold and while the gold was sold at Hyderabad, diamonds were sold at Surat. The resultant sale proceeds were shown as ‘capital gains’ in the respective returns for the assessment year 1998-99. The Assessing Officer was satisfied as regards the proceeds from the sale of gold. The controversy is only about the sale of diamonds.

The starting point for the doubt of the Assessing Officer was as to the very separation of diamonds from jewellery. The next was about the actual sale at Surat. It may be true that the respondents did not declare the diamonds in their unused and unembedded form. When jewellery of such a huge value is declared, it is axiomatic that the items of jewellery are studded with diamonds and other precious stones. No effort was made to have a detailed account of the nature of jewellery that was declared. There is no dispute that what was declared by the respondents was in the form of ornaments. It is just unthinkable that the ornaments of such huge value and quantity would be in the form of pure gold.

There is ample evidence to show that all the three assesses have sold the diamonds, that are separated from the jewellery, at Surat. It is a place known for voluminous business in diamonds. Not only the particulars of the persons, who purchased the diamonds was furnished, but also the manner of payment was disclosed. The entire payments were through demand drafts. The cross verification undertaken by the Assessing Officer, did not result in noticing of any discrepancy. The bank accounts of the purchasers were verified and the demand drafts issued to the respondents, towards consideration, corresponded to the entries in the bank accounts.

Unable to find any discrepancy in such important aspects, the Assessing Officer started the verification of travel particulars of the respondents. The record discloses that the sale of diamonds did not take at a time and it was in a phased manner. The purchaser was undoubtedly a dealer in diamond. Even assuming that on certain occasions, the corresponding assessee did not proceed to Surat, it cannot be a factor to disbelieve the transaction. When not only the respondents have disclosed the wealth in VDIS, but also have shown sale proceeds as ‘capital gains’, it was far fetched, if not unreasonable, on the part of the Assessing Officer, to doubt their honesty in this behalf. For all practical purposes, the Assessing Officer subjected the respondents herein to a verification equivalent to the one which is made by the police officials vis-à-vis a person, who committed the crime. Though it is prerogative of the State to levy tax, referable to its sovereign power, it cannot be extended to the level of regulating the conduct of a citizen to such minute extents.

At any rate, the relief granted by the Tribunal is based its findings on pure question of fact. Even before us, no question of law is argued. Except that the Assessing Officer intended to treat the sale proceeds of jewellery under Section 68 (of Income Tax Act, 1961), no other provision of law is invoked, nor any principle is projected.

We, therefore, dismiss the appeals. There shall be no order as to costs.

The miscellaneous petitions filed in these appeals shall also stand disposed of.

L.NARASIMHA REDDY, J.

CHALLA KODANDA RAM, J.

×

Similar Ripples

Questions

Court Upholds Genuine Diamond Sales, Rejects Tax Authority's Skepticism

Write your CommentSimilar Posts

Generic

- Reportdata/4587.pdf