Bank of Baroda's TDS Dispute: Court Upholds Tax Demand

Full News

Bank of Baroda's TDS Dispute: Court Upholds Tax Demand

Bank of Baroda's TDS Dispute: Court Upholds Tax Demand

The case involves the Bank of Baroda challenging an order by the Commissioner of Income Tax (Appeals) that rejected the bank's request to stay a tax demand. The dispute arose from the bank's failure to deduct Tax Deducted at Source (TDS) on interest payments to Visveswarayya Technological University (VTU), which claimed tax exemption. The court upheld the tax demand, dismissing the bank's petition.

Get the full picture - access the original judgement of the court order here

Case Name:

Bank of Baroda Vs. Income Tax Officer & Anr. (High Court of Karnataka)

Writ Petition No. 114181-184 of 2015 (T-IT)

Date: 18th December 2015

Key Takeaways:

- The court emphasized the statutory duty of banks to deduct TDS unless a valid exemption is proven.

- The decision highlights the importance of raising all relevant contentions at the appropriate stages in tax proceedings.

- The court clarified that exemptions under Section 201(1) (of Income Tax Act, 1961) require clear evidence of tax payment by the recipient.

Issue

Did the Bank of Baroda have a valid reason to not deduct TDS on interest payments to VTU, and should the tax demand be stayed pending appeal?

Facts

- The Income Tax Officer issued summons to the Bank of Baroda to provide details of fixed deposits and interest payments to VTU for the years 2010-2014.

- The bank did not deduct TDS, relying on VTU's claim of exemption under Section 10(23C)(iiiab) (of Income Tax Act, 1961).

- The ITO treated the bank as an assessee in default and raised a tax demand.

- The bank's appeal for a stay on the demand was rejected by the Commissioner (Appeals), leading to this court petition.

Arguments

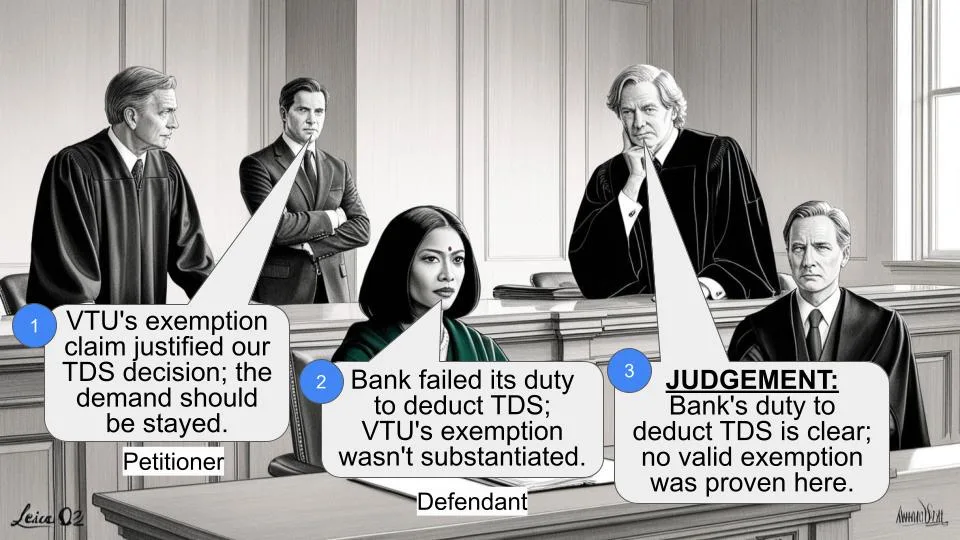

- Bank of Baroda: Argued that VTU's exemption claim justified not deducting TDS and that the tax demand should be stayed as the issue was previously decided in their favor.

- Income Tax Department: Maintained that the bank failed to fulfill its statutory duty to deduct TDS and that the exemption claim was not substantiated.

Key Legal Precedents

- Section 201(1) (of Income Tax Act, 1961): Discusses the consequences of failing to deduct TDS, with a proviso for cases where the tax liability is paid by the recipient.

- Section 249(4) (of Income Tax Act, 1961): Requires payment of advance tax for an appeal to be admitted, with discretionary power for exemption by the Commissioner.

Judgement

The court dismissed the Bank of Baroda's petition, upholding the tax demand. It found no evidence that the bank's situation fell under the exceptions that would justify a stay of the demand. The court noted the bank's failure to adequately raise the exemption contention before the ITO and emphasized the statutory duty to deduct TDS.

FAQs

Q1: Why did the court dismiss the bank's petition?

A1: The court found that the bank did not provide sufficient evidence to justify not deducting TDS and did not meet the criteria for a stay of the tax demand.

Q2: What is the significance of Section 201(1) (of Income Tax Act, 1961) in this case?

A2: It outlines the consequences for failing to deduct TDS, with an exception if the tax is paid by the recipient, which the bank failed to prove.

Q3: Can the bank appeal this decision?

A3: Yes, the bank can appeal to a higher court, but it must address the issues identified in this judgment.

Q4: What does this mean for other banks?

A4: Banks must ensure compliance with TDS obligations and thoroughly document any claims of exemption to avoid similar disputes.

1. The petitioner, Bank of Baroda, has challenged the order dated 15.04.2015, passed by the Commissioner of Income Tax (Appeals), Belagavi, whereby the learned Commissioner has rejected the petitioner’s prayer for stay of demand dated 16.03.2015.

2. Briefly, the facts of the case are that the Income Tax

Officer, respondent No.1 (the ‘ITO', for short), had issued

summons on 15.12.2014 under Section 131 (of Income Tax Act, 1961) along with notice

under Section 133(6) (of Income Tax Act, 1961) (‘the Act’, for

short), calling upon the petitioner-Bank to submit details of

the Fixed Deposits held by the Visveswarayya Technological

University, Belagavi (‘the VTU’, for short) and the interest paid

on such deposits during the financial years 2010-2011 to

2013-2014, and the Tax Deducted at Source (‘TDS’, for short)

on such payment, and to show reasons as to why these

deductions have not been made, and quarterly statements filed

under Section 194A (of Income Tax Act, 1961), in respect of such payments.

By letter dated 26.12.2014, the petitioner Bank informed the

ITO that it did not deduct any TDS on the interest paid to the

VTU, because by letter dated 03.09.2014, the VTU had

informed the Bank that the University is exempted from filing

the returns under Section 10(23C)(iiiab) (of Income Tax Act, 1961) Section 139 (of Income Tax Act, 1961).

The Bank further claimed that since it had no reason to

disbelieve the assertion made by the payee-VTU, it did not

deduct the TDS.

3. Not satisfied by the explanation offered by the

petitioner-Bank, on 29.12.2014, the ITO issued a show cause

notice to the petitioner, calling upon it to explain why it should

not be considered as an assessee in default, for failing to make

the TDS under Section 194A (of Income Tax Act, 1961). Subsequently, on

16.01.2015, the ITO issued summons under Section 131 (of Income Tax Act, 1961) of the

Act, and also sent a letter to the petitioner-Bank calling upon

the Bank to appear before him on 22.01.2015. The Bank was

directed to produce the additional documents related to

interest payments made to the VTU, without deducting TDS.

Consequently, on 19.01.2015, the Bank filed a written

submission explaining the reasons why the TDS was not made

on interest paid to the VTU. The Bank further explained the

reason why it should not be treated as an assessee in default.

4. Notwithstanding the explanation given by the

petitioner-Bank, on 19.02.2015, the Income Tax Officer passed

four separate, but identical orders, and treated the petitioner-

Bank as an assessee in default, and raised an aggregate

interest payment of Rs.15,22,963/- under Section 201(1) (of Income Tax Act, 1961)/(1A)

of the Act, for the assessment year 2011-12 to 2014-2015.

5. Since the petitioner-Bank was aggrieved by the

assessment order dated 19.02.2015, it filed an appeal under

Section 246A(1)(ha) (of Income Tax Act, 1961) and filed the petition under Section 220(6) (of Income Tax Act, 1961)

of the Act before the Commissioner of Income Tax (Appeals).

6. On 19.03.2015, the Income Tax Officer issued an

order under Section 220(6) (of Income Tax Act, 1961), directing the petitioner

to pay 50% of the disputed demand before 27.03.2015.

However, by letter dated 27.03.2015, the petitioner-Bank

expressed its strong objections to the said order, and

requested the ITO to grant stay of recovery of the disputed

demand until disposal of the appeal pending before the

Commissioner (Appeals).

7. On 06.04.2015 and on 10.04.2015, the petitioner-

Bank filed two written submissions before the Commissioner

(Appeals) and prayed that the disputed demand be stayed and

that the ITO should be directed not to treat the petitioner as an

assessee in default until disposal of the appeals pending before

the Commissioner (Appeals). However, by order dated

15.04.2015, the learned Commissioner (Appeals) has rejected

the application for stay, but has assured the petitioner-Bank

that its appeal would be considered on priority basis. Hence

the present petition before this Court.

8. Mr. B. S. N. Prasad, the learned counsel for the

petitioner, has contended that, while Section 201 (of Income Tax Act, 1961)

lays down the consequence of failure to deduct the tax at

source, the proviso attached to Section 201(1) (of Income Tax Act, 1961)

creates an exception in favour of the deductor. According to

the proviso, in case the tax liability imposed upon the VTU

were paid by the VTU, then the petitioner-Bank is not required

to deduct the TDS.

Secondly, in the impugned order, the learned

Commissioner (Appeals) is unjustified in claiming that the

petitioner-Bank does not fall within the illustrations

enumerated in para-C of the Instruction No.1914. According

to the learned counsel, the petitioner-Bank clearly falls within

the first illustration, namely “if the demand in dispute relates to

issues that have been decided in assessee’s favour by an

Appellate Authority or the Court earlier”, then the demand

should be stayed by the learned Commissioner. However, the

learned Commissioner has ignored the illustration (a)

contained in para-C of Instruction No.1914. Therefore, the

impugned order deserves to be set aside by this Court.

9. Heard the learned counsel for the petitioner, and

perused the impugned order.

10. This Court has asked a pointed question to the

learned counsel for the petitioner: whether the petitioner-Bank

had raised the contention before the ITO with regard to the

benefit granted to the petitioner Bank under the proviso

attached to Section 201(1) (of Income Tax Act, 1961) or not? To this pointed

query, the learned counsel has given a very evasive answer.

According to him, the said contention was, indeed, raised

before the Income Tax Officer. However, when this Court

asked him to point out where the said contention was recorded

in the Assessment Order, the learned counsel could not show

that such contention had, indeed, been raised before the ITO.

Therefore, this Court is of the opinion that the said contention

was not raised before the ITO, although it may have been

mentioned in the written submission filed by the Bank. In

catena of cases, the Hon’ble Supreme Court has opined that, if

any contention is contained in the written submission, but

unless and until it is recorded and reflected in the impugned

order, the Court shall presume that the said contention was

not raised before the concerned authority or the Court.

11. A bare perusal of the assessment order clearly

reveals, that the stand taken by the petitioner-Bank was that

since they were informed by the VTU that they were exempted

from filing the return under Section 10(23C)(iiiab) (of Income Tax Act, 1961) Section 139 (of Income Tax Act, 1961)

of the Act, the Bank never deducted the TDS.

12. The issue whether the VTU is exempted under

Section 10(23C)(iiiab) (of Income Tax Act, 1961) or not, the issue whether the

petitioner-Bank was statutorily bound to deduct the TDS, has

been discussed threadbare by the ITO. Since it would not be

correct for this Court to express any opinion about the findings

of the ITO, this Court restrains itself from expressing any

opinion on these two issues. For, expression of any opinion on

these two points may adversely affect the appeal pending

before the Commissioner (Appeals).

13. The moot question before this Court is whether the

petitioner-Bank can claim the right to be exempted from

depositing the tax liability or not, prior to its appeal being

admitted for hearing?

14. According to Section 249(4) (of Income Tax Act, 1961), no appeal

in the chapter shall be admitted, unless at the time of filing an

appeal, the assessee has paid an amount equal to the amount

of advance tax, which was payable by him. Thus, Section

249(4) of the Act clearly stipulates that the assessee is duty

bound to pay the amount equal to the amount of advance tax.

However, the proviso bestows a discretionary power upon the

Commissioner (Appeals) to exempt the assessee from the

portion of the provisions of clause-B mentioned above.

15. Therefore, the question before this Court is whether

the Commissioner(Appeals) has exercised his discretion legally

or illegally? According to the proviso, in case the

Commissioner were to grant any exemption from the payment

of the amount equal to the amount of advance tax, he should

record his good and sufficient reason in writing.

16. A bare perusal of the impugned order clearly

reveals that the learned Commissioner has opined that, since

the petitioner-Bank does not fall within any of the illustrations

contained in para C of the Instruction No.1914, the benefit of

staying the demand cannot be given to the petitioner-Bank.

17. Of course the learned counsel for the petitioner has

pleaded that the petitioner-Bank does fall within the

illustration (a) of para C of instruction No.1914 which is as

under:

(a) if the demand in dispute relates to issues that have

been decided in assessee’s favour by an appellate

authority or court earlier;.........

it is clarified that in these situations also, stay may be

granted only in respect of the amount attributable to such

dispute points. Further, where it is subsequently found

that the assessee has not cooperated in the early disposal

of appeal or where a subsequent pronouncement by a

higher appellate authority or court alters the above

situation, the stay order may be reviewed and modified. “

18. According to the illustration (a), the demand can be

stayed by the learned Commissioner, provided that demand in

dispute relates to issues that have been decided in assessee’s

favour by an Appellate Authority, or the Court earlier.

However, the learned counsel for the petitioner has not been

able to show this Court as to which Appellate Authority, or by

which Court the issues involved in the present case have

already been decided, that, too, in favour of the petitioner-

Bank. Thus, obviously, the petitioner-Bank cannot claim that

it falls under illustration (a) of para-C of Instruction No.1914.

19. The learned counsel has further pleaded that, since

the petitioner-Bank is a public sector undertaking, it should

not be imposed with the liability to deposit the entire tax

liability. However, the said contention is unacceptable. For a

statutory duty has been imposed upon the Bank to deduct the

TDS. In case the Bank does not deduct the TDS, it has to face

the consequences as mentioned in Section 201 (of Income Tax Act, 1961).

Since Section 249(4) (of Income Tax Act, 1961) imposes a duty upon the

assessee to deposit the entire amount, before that appeal can

be admitted, the Bank cannot escape from its liability to follow

the mandate of Section 249(4) (of Income Tax Act, 1961). Although Instruction

No.1914 does create exception to Section 249(4) (of Income Tax Act, 1961), as

mentioned above, the petitioner-Bank cannot take any benefit

from Instruction No.1914, as it does not come within the ambit

and scope of the said instruction.

20. For the reasons stated above, this Court does not

find any illegality or perversity in the impugned order. These

petitions, being devoid of any merit, are hereby dismissed.

Sd/-

JUDGE

×

Similar Ripples

Questions

Bank of Baroda's TDS Dispute: Court Upholds Tax Demand

Write your CommentSimilar Posts

Generic

- Reportdata/3223.pdf