High Court Upholds Tribunal’s Decision to Cancel Penalty on Bank for TDS Non-De…

Full News

High Court Upholds Tribunal’s Decision to Cancel Penalty on Bank for TDS Non-Deduction

High Court Upholds Tribunal’s Decision to Cancel Penalty on Bank for TDS Non-Deduction

This case involves an appeal by the revenue department against the Income Tax Appellate Tribunal’s decision to cancel a penalty imposed on State Bank of Patiala for failing to deduct tax at source (TDS) on interest payments. The High Court dismissed the appeal, agreeing with the Tribunal that the bank had reasonable cause for not deducting TDS.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax (TDS) Vs State Bank of Patiala (High Court of Punjab & Haryana)

ITA No. 400 of 2015

Date: 4th February 2016

Key Takeaways:

- The court affirmed that certain government-financed societies are exempt from TDS on interest payments.

- Genuine belief and reasonable cause can be valid grounds for non-deduction of TDS.

- Concurrent findings by lower authorities (CIT(A) and Tribunal) are generally not interfered with by higher courts unless perverse.

Issue:

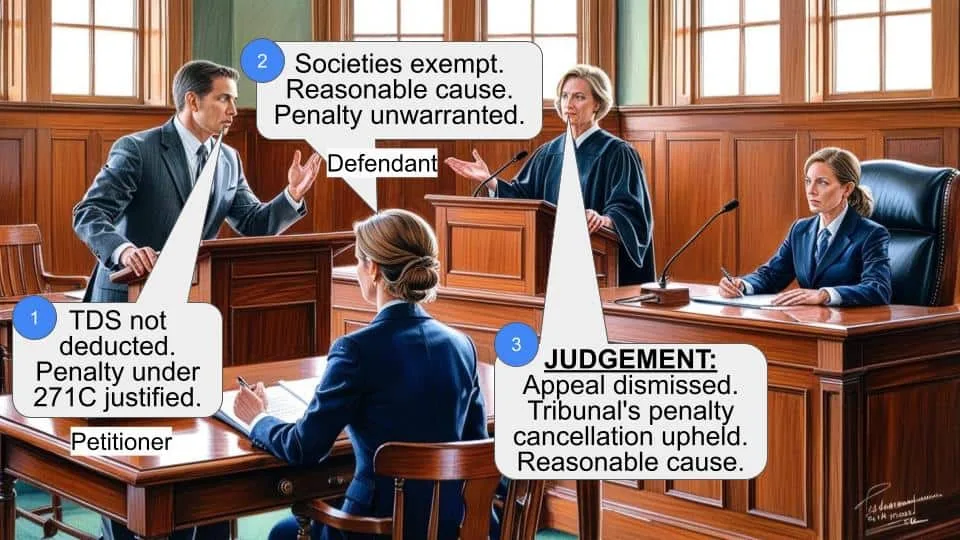

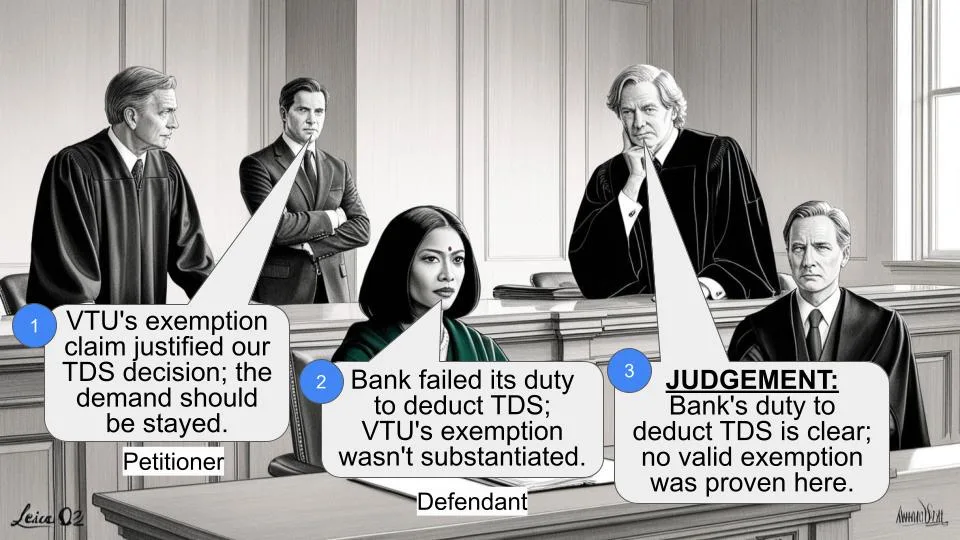

Was the Income Tax Appellate Tribunal correct in cancelling the penalty imposed on State Bank of Patiala under Section 271C (of Income Tax Act, 1961) for failure to deduct tax at source on interest payments?

Facts:

- A TDS inspection at State Bank of Patiala revealed that the bank hadn’t deducted tax on interest paid to certain parties.

- The bank admitted the default and deposited the TDS along with interest.

- The Joint Commissioner of Income Tax imposed a penalty of ₹22,58,086 under Section 271C (of Income Tax Act, 1961).

- The bank appealed, and both the CIT(A) and the Tribunal cancelled the penalty.

- The revenue department then appealed to the High Court.

Arguments:

Revenue’s Argument:

- The bank failed to deduct TDS as required under Section 194A (of Income Tax Act, 1961).

- This failure warranted a penalty under Section 271C (of Income Tax Act, 1961).

Bank’s Argument:

- The interest payments were made to societies exempt from TDS under Section 194A(3)(iii)(f) (of Income Tax Act, 1961).

- The bank had a genuine belief that TDS wasn’t required for these societies.

- There was reasonable cause for the failure to deduct TDS, falling under Section 273B (of Income Tax Act, 1961).

Key Legal Precedents:

- ITA No. 17 of 2014 (Commissioner of Income Tax (TDS), Chandigarh v. State Bank of Patiala Sectt. Shimla) - This Himachal Pradesh High Court decision held that no TDS is required on payments to societies wholly financed by the Government, as per Section 194A(3)(iii)(f) (of Income Tax Act, 1961).

- Income Tax Officer v. State Bank of Patiala, Kusumpti, Shimla, ITA No. 271/CHD/2014 - The Tribunal dismissed the revenue’s appeal and confirmed the cancellation of penalty under Section 271C (of Income Tax Act, 1961).

Judgement:

The High Court dismissed the revenue’s appeal, agreeing with the Tribunal’s decision. Key points:

- The CIT(A) and Tribunal had concurrently found that the penalty wasn’t leviable.

- Three of the four societies were exempt from TDS under Section 194A(3)(iii)(f) (of Income Tax Act, 1961).

- For the fourth society (Shri Aurobindo Society), the bank had reasonable cause to believe TDS wasn’t required.

- The court found no perversity in the lower authorities’ findings to warrant interference.

FAQs:

Q: What is Section 194A(3)(iii)(f) (of Income Tax Act, 1961)?

A: It’s a provision that exempts certain government-notified institutions from TDS on interest payments.

Q: Why wasn’t the bank required to deduct TDS for three of the societies?

A: These societies were registered under the Societies Registration Act, 1860, and wholly financed by the government, making them exempt under the relevant notification.

Q: What is the significance of “reasonable cause” in this case?

A: Under Section 273B (of Income Tax Act, 1961), penalties aren’t imposed if the assessee proves there was reasonable cause for the failure to comply.

Q: Does this judgment set a precedent for similar cases?

A: While it reinforces existing interpretations, each case would still be judged on its own merits and specific circumstances.

Q: What lesson can other banks or financial institutions learn from this case?

A: It’s crucial to be aware of TDS exemptions and maintain proper documentation to support any non-deduction of TDS.

1. This appeal has been preferred by the revenue under Section 260A (of Income Tax Act, 1961) (in short “the Act”) against the order dated 27.2.2015 (Annexure A-4) passed by the Income Tax Appellate Tribunal, Chandigarh Bench “A”, Chandigarh (hereinafter referred to as “the Tribunal”) in ITA No. 1129/CHD/2014, for the assessment year 2011-12, claiming the following substantial questions of law:-

(i) Whether the ITAT was right in law in deleting the penalty imposed by the AO u/s 271C (of Income Tax Act, 1961) read with Section 274 (of Income Tax Act, 1961) for failure to deduct tax at source out of interest paid/credited to four deductees as required u/s 194A (of Income Tax Act, 1961)?

(ii) Whether on the facts and circumstances of the present case and in law, the Hon'ble ITAT is right in holding that the assessee was not liable to deduct tax at source, as required u/s 194A (of Income Tax Act, 1961)?

(iii) Whether in the facts and circumstances of the case and in law the Hon'ble ITAT is right in holding that assessee has a genuine belief that it was not required to deduct tax at source, as required u/s 194A (of Income Tax Act, 1961)?

2. Briefly stated, the facts necessary for adjudication of the instant appeal as narrated therein may be noticed. A TDS Inspection/ Survey under Section 133A (of Income Tax Act, 1961) was carried out at the business premises of the assessee on 27.2.2013. During the course of said survey, it was noticed that the assessee had not deducted tax on interest paid to different parties who claimed to be exempt from the income tax under Sections 12A (of Income Tax Act, 1961) and 10(23C) of the Act. The Person Responsible(PR) of the Bank admitted the default on his part and deposited the Tax Deducted at Source (TDS) along with interest on 1.3.2013. On asking to furnish the details and proof of deposit of TDS into Government account, the PR furnished the same vide letter dated 1.3.2013 and as per the details, the total TDS of ` 22,58,086/- along with interest under Section 201(1A) (of Income Tax Act, 1961) amounting to ` 2,14,732/-, thus, totalling 24,72,818/- was deposited. The assessee had filed its e-TDS statements late for the financial year 2010-11. The matter regarding initiation of penalty proceedings under Section 272A(2)(k) (of Income Tax Act, 1961) was referred to the Joint Commissioner of Income Tax (TDS), Range,Chandigarh. Since the PR had failed to deduct tax at source under Section 194A (of Income Tax Act, 1961) @ 10% on the payments made on account of interest paid to different parties and deposit the same in the Central Government account, the Deputy Commissioner of Income Tax (TDS), Chandigarh vide order dated 28.3.2013 (Annexure A-1) under Section 201(1) (of Income Tax Act, 1961)/201(1A) of the Act separately referred to the office of Joint Commissioner of Income Tax (TDS), Range, Chandigarh regarding initiation of penalty proceedings under Section 271C (of Income Tax Act, 1961). Accordingly, a notice dated 15.4.2013 was issued to the PR to show cause as to why penalty under Section 271C (of Income Tax Act, 1961) read with Section 274 (of Income Tax Act, 1961) be not levied for failing to pay the amount of TDS. The Joint Commissioner of Income Tax (TDS), Range, Chandigarh vide order dated 16.8.2013 (Annexure A-2) imposed a penalty of ` 22,58,086/- under Section 271C (of Income Tax Act, 1961) which was equal to the amount of TDS. Feeling aggrieved, the assessee filed an appeal before the Commissioner of Income Tax (Appeals) [for brevity “the CIT(A)”]. The CIT(A) vide order dated 30.10.2014 (Annexure A-3) allowed the appeal of the assessee and deleted the penalty. Against the order, Annexure A- 3, the revenue filed an appeal before the Tribunal who vide order dated 27.2.2015 (Annexure A-4) upheld the order of the CIT(A) and dismissed the appeal. Hence, the present appeal.

3. We have heard learned counsel for the revenue and are not impressed with the argument raised by him.

4. Section 194A (of Income Tax Act, 1961) relates to deduction of tax at source on interest other than “interest on securities”. Sub-section (3) of Section 194A (of Income Tax Act, 1961) provides where the provisions of sub-section (1) relating to deduction of tax at source do not apply. According to sub clause (f) of Clause (iii) thereunder, the provisions of tax deducted at source are not applicable to such income credited or paid to any institution, association or body or class by institutions, associations or bodies where the Central Government after recording the reasons in writing notifies them in the Official Gazette. Section 194A(3)(iii)(f) (of Income Tax Act, 1961) reads thus:-

“194A. Interest other than “interest on securities”.

(3) The provisions of sub-section (1) shall not apply-

(iii) to such income credited or paid to-

(f) such other institution, association or body or class of institutions, associations or bodies which the Central Government may, for reasons to be recorded in writing, notify in this behalf in the Official Gazette.”

5. The Central Government had issued notification no. S.O.3489 [No. 170 (F.No. 12/164/68-ITCC/ITJ).] dated 22.10.1970 under Section 194A(3)(iii)(f) (of Income Tax Act, 1961) notifying Corporations, Undertakings, Societies etc. thereunder which reads thus:-

“In pursuance of sub-clause (f) of clause (iii) of sub- section (3) of section 194A (of Income Tax Act, 1961) (43 of 1961), the Central Government hereby notify the following for the purposes of the said sub- clause:-

(i) any corporation established by a Central, State or Provincial Act;

(ii) any company in which all the shares are held (whether singly or taken together) by the Government or the Reserve Bank of India or a Corporation owned by that Bank; and

(iii) any undertaking or body, including a society registered under the Societies Registration Act, 1860 (21 of 1860), financed wholly by the Government.”

6. The CIT(A) had noticed that the action was initiated for levy of penalty under Section 271C (of Income Tax Act, 1961) for not deducting tax at source in respect of the following four societies:-

“1. Haryana Rural Roads and Infrastructure Development Agency (HARRIDA);

2. Punjab ICT Education Society (Director General School Education Punjab);

3. Haryana State Council for Science & Technology;

4. Shri Aurobindo Society.

7. It was observed that in the case of three societies, i.e. Haryana Rural Roads and Infrastructure Development Agency, Punjab ICT Education Society and Haryana State Council for Science and Technology, the assessee was not liable to deduct TDS on interest paid to the said parties in view of the provisions of Section 194A(3)(iii)(f) (of Income Tax Act, 1961) read with notification No. S.O.3489 dated 22.10.1970 since they were registered under the Societies Registration Act, 1860 and financed by the Government. Further, it was recorded that in the similar matter in Income Tax Officer v. State Bank of Patiala, Kusumpti, Shimla, ITA No. 271/CHD/2014, the Tribunal had dismissed the appeal of the revenue and confirmed the ordered of the CIT(A) in cancelling the penalty under Section 271C (of Income Tax Act, 1961) on the ground that in such circumstances the assessee would have genuine belief that it was not required to deduct tax at source. In the case of Shri Aurobindo Society, the CIT(A) again noticed that the exemption certificate under Section 80G(5)(vi) (of Income Tax Act, 1961) valid for assessment year 2011-12 and a copy of return of income of Shri Aurobindo Society where total income declared was 'nil', was also filed and, therefore, the assessee had a reasonable cause for failure to deduct tax at source under Section 201(1) (of Income Tax Act, 1961). Accordingly, the CIT(A) cancelled the penalty levied by the department under Section 271C (of Income Tax Act, 1961) .

8. On appeal the said findings were affirmed by the Tribunal holding that the assessee had a genuine belief that it was not required to deduct TDS. Further, the Tribunal observed that the penalty was not leviable as the case of the assessee fell under Section 273B (of Income Tax Act, 1961) and it had been able to prove that there was a reasonable cause for the said failure. The relevant findings recorded by the Tribunal read us:-

“4. We have heard ld. Representative of both the parties and perused the findings of authorities below. The ld. DR relied upon order of the Assessing Officer. On the other hand, ld. Counsel for the assessee reiterated the submission made before authorities below. He has relied upon order of ITAT Chandigarh Bench in ITA No. 267 to 271/CHD/2014 in the case of ITO Vs. State Bank of atiala, Kusumpti, Shimla (supra) and relied upon judgment of Hon'ble Himachal Pradesh in the case of CIT(TDS) Chandigarh Vs. State Bank of Patiala, Shimla in ITA No. 17/2014 dated 31.12.2014.

5. On consideration of the facts of the case, in the light of the findings of ld. CIT (Appeals) and the above decisions, we do not find any merit in the appeal of revenue. The ld. CIT(Appeals) found that in case of three of the societies, the assessee was not liable to deduct tax at source. In the case of Shri Aurobindo Society, the exemption certificate under section 80G(5)(vi) (of Income Tax Act, 1961) was also filed. It would, therefore, prove that assessee had a reasonable cause for failure to deduct tax at source under section 201(1) (of Income Tax Act, 1961). In the case of State Bank of Patiala, Kunsumpti, Shimla (supra), ITAT Chandigarh Bench dismissed the department appeal confirming the order of the ld. CIT (Appeals) in canceling the penalty under section 271C (of Income Tax Act, 1961). The facts are identical in the case of State Bank of Patiala, Shimla (supra). Hon'ble Himachal Pradesh High Court dismissed departmental appeal finding no substantial question of law. These facts would clearly support the findings of ld. CIT(Appeals) that assessee had a genuine belief that it would not require to deduct tax at source. The case of the assessee, therefore, squarely falls under the provisions of Section 273B (of Income Tax Act, 1961) and penalty is not leviable because assessee is able to prove that there was a reasonable cause for the said failure.”

9. The CIT(A) and the Tribunal on appreciation of material on record have concurrently recorded that the penalty under Section 271C (of Income Tax Act, 1961) was not leviable upon the assessee and cancelled the said penalty. Further, the Himachal Pradesh High Court in ITA No. 17 of 2014 (Commissioner of Income Tax (TDS), Chandigarh v. State Bank of Patiala Sectt. Shimla) decided on 31.12.2014 had held that no tax at source is required to be deducted in view of Section 194A(3)(iii)(f) (of Income Tax Act, 1961) in respect of payments made to any societies which are wholly financed by the Government and the Central Government had issued notification exempting those societies. Learned counsel for the revenue was not able to demonstrate that the approach of the CIT(A) and the Tribunal was erroneous or perverse or that the findings of fact recorded were based on misreading or misappreciation of evidence on record warranting interference by this Court.

10. In view of the above, no substantial question of law arises in this appeal. Accordingly, the instant appeal is dismissed.

(AJAY KUMAR MITTAL)

JUDGE

February 4, 2016 (RAJ RAHUL GARG)

×

Similar Ripples

Questions

High Court Upholds Tribunal’s Decision to Cancel Penalty on Bank for TDS Non-Deduction

Write your CommentSimilar Posts

Generic

- Reportdata/3123.pdf