Full News

Court allows full depreciation claim on agricultural assets under IT Act

Court allows full depreciation claim on agricultural assets under IT Act

This case involves Rehabilitation Plantations Ltd., a company engaged in rubber manufacturing, appealing against the Income Tax Department's decision to restrict their depreciation claim. The High Court ruled in favor of the company, allowing them to claim depreciation on the full cost of agricultural assets under the Income Tax Act, despite previous claims under the Agricultural Income Tax Act.

Get the full picture - access the original judgement of the court order here.

Case Name:

Rehabilitation Plantations Ltd. Vs Commissioner of Income Tax (High Court of Kerala)

ITA.No. 29 of 2008

Key Takeaways:

1. The court allowed the company to claim depreciation on the full cost of agricultural assets under the Income Tax Act.

2. The judgment highlights a legislative oversight in handling the transition of agricultural income taxation from state to central laws.

3. The court emphasized that it cannot fill legislative gaps through judicial interpretation.

Issue:

Whether the Income Tax Appellate Tribunal was justified in restricting the depreciation allowed to the amount worked out on the written down value of the assets as against the original cost of the assets claimed by the assessee?

Facts:

1. The case concerns the assessment year 2002-2003 when Rule 7A (of Income Tax Rules, 1962) was introduced in the Income Tax Rules, 1962.

2. The appellant's income, previously assessed under the Kerala Agricultural Income Tax Act, 1991, became assessable under the Income Tax Act, 1961 to the extent of 35% of such income.

3. The company claimed depreciation on the entire cost of plant and machinery to the extent of 35%.

4. The Assessing Officer found that the company had been providing depreciation on assets used for agricultural operations in their profit and loss accounts for over two decades.

Arguments:

The appellant argued that:

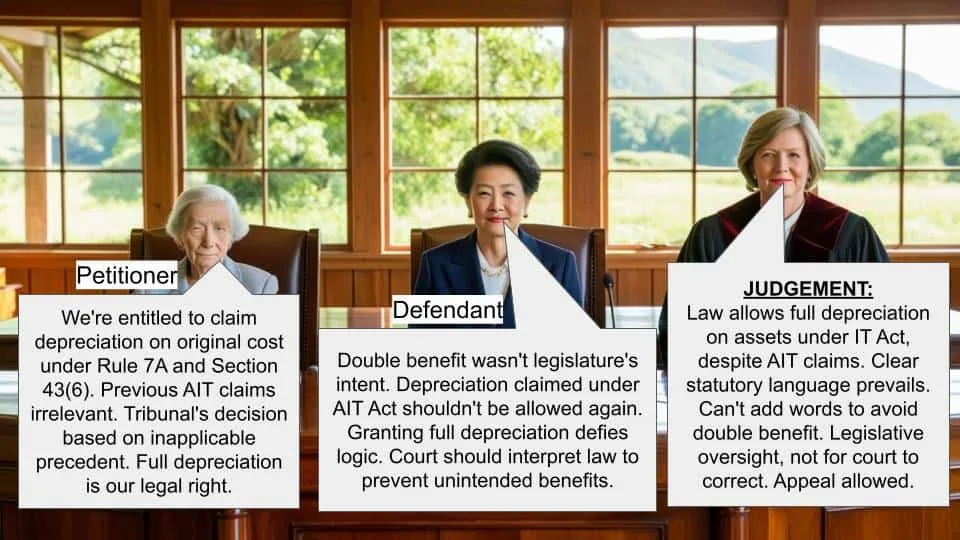

1. They should be allowed to claim depreciation on the original cost of assets under Rule 7A (of Income Tax Rules, 1962) and Section 43(6) (of Income Tax Act, 1961).

2. The decision relied on by the Tribunal was not applicable as it was rendered under a different section (80HHC) of the IT Act.

The Revenue contended that:

1. The legislature would not have contemplated granting a double benefit.

2. Depreciation already claimed under the AIT Act should not be granted again under the IT Act.

Key Legal Precedents:

1. Commissioner of Income Tax v. Doom Dooma India Ltd. [(2009) 310 ITR 392 (SC)]:

This case defined "actual cost to the assessee" as the actual cost incurred in acquiring the plant and machinery, regardless of when it was acquired.

2. Madeva Upendra Sinai v. Union of India and Others [1975 (98) ITR 209 (SC)]:

This case established that when no depreciation was computed or allowed in the past, the "written-down value" may be the actual cost of the assets to the assessee.

Judgement:

The High Court ruled in favor of the assessee, stating that:

1. The deeming provision in Section 43(6)(b) (of Income Tax Act, 1961) is clear and does not exclude depreciation allowed under the AIT Act from the computation of the cost of assets.

2. The court cannot add words to the statute to avoid a double benefit, as this would digress from the unambiguous intention of the law.

3. The Assessing Officer should employ the deeming provision for computing the written down value, disregarding the depreciation granted under the AIT Act, and take 35% of the cost of the total assets as written down value.

FAQs:

Q1: Why did the court allow the company to claim depreciation on the full cost of assets?

A1: The court found that the law, as it stood at the time, did not explicitly exclude depreciation claimed under the AIT Act when calculating depreciation under the IT Act.

Q2: Did the government address this issue later?

A2: Yes, the government introduced Explanation 7 to Section 43(6) (of Income Tax Act, 1961) through the Finance Act, 2009, effective from 1.4.2010, to prevent such double benefits in the future.

Q3: Why couldn't the court interpret the law to prevent double benefits?

A3: The court emphasized that it cannot fill legislative gaps through judicial interpretation, citing the principle that "a legislative casus omissus cannot be supplied by a judicial interpretative process."

Q4: What is the significance of Rule 7A (of Income Tax Rules, 1962) mentioned in the case?

A4: Rule 7A (of Income Tax Rules, 1962), introduced in 2002, made 35% of the income from rubber manufacturing, previously treated as agricultural income, assessable under the Income Tax Act.

1. The appellant is engaged in the business of manufacture and sale of centrigued latex and rubber. The appeal is concerned with assessment for the year 2002-2003 when Rule 7A (of Income Tax Rules, 1962) was introduced in the Income Tax Rules, 1962 ('Rules', for short). The appellant's income then assessed under the Kerala Agricultural Income Tax Act, 1991 ('AIT Act', for short) of the State, was assessable under the Income Tax Act, 1961 ('IT Act', for short) to the extent of 35% of such income, which as per Rule 7A (of Income Tax Rules, 1962) is deemed to be income liable to tax. The issue arises as to the depreciation allowable to the assessee.

2. The questions of law arising from the order of the Income Tax Appellate Tribunal (for short, 'Tribunal') as available in the memorandum of appeal are as follows:-

“i) Whether on the facts and in the circumstances of the case, was the Income Tax Appellate Tribunal justified in restricting the depreciation allowed to the amount worked out on the written down value of the assets as against the original cost of the assets claimed by the assessee ?

ii) In the facts and circumstances of the case ought not the Tribunal have held that applying the provisions of Rule 7A (of Income Tax Rules, 1962) and Section 43(6) (of Income Tax Act, 1961), that the claim of depreciation of the appellant on the original cost was in order ?”

3. The assessee claimed depreciation of the entire cost of the plant and machinery to the extent of 35% treating it as the actual cost allowable on which is computed the allowable deduction for depreciation. The Assessing Officer found that the appellant had been providing for depreciation on assets used for the agricultural operations, in the profit and loss accounts prepared as per the Companies Act, 1956. The depreciation on assets used in the plantations, including for manufacturing activity, was found to have been claimed by the assessee-Company for more than two decades. It was found that earlier the assessments have not been taken under the IT Act, since the entire income was assessable under the AIT Act. It was found that as per Section 32(1) (of Income Tax Act, 1961), depreciation on building, machinery, etc. is to be allowed on the written down value of the assets, owned by the assessee and used for the purposes of the business.

4. The written down value of the assets as per Section 43(6) (of Income Tax Act, 1961) is the actual cost when the assets were acquired before the previous year. Otherwise the written down value shall be the actual cost of the assets less all depreciation actually allowed under the IT Act. The Assessing Officer also found that the assessee- appellant had been claiming “depreciation” in computing the income of the assessee from plantations, and if the actual cost of the assets is adopted it would lead to the assessee getting a double benefit on the same component of cost, to the extent of 35%. Hence, the written down value for the previous year was only permissible to be claimed as depreciation, was the specific ground on which such claim was rejected. The Commissioner of Appeals affirmed the view of the Assessing Officer. The appellant was before the Tribunal. The Tribunal, as is seen from Annexure-C order, relied on the decision in CIT v. Parry Agro Industries Ltd., [206 CTR 36 (Ker.)] to hold that there can be no claim for the assessee over and above the written down value as per the books of accounts.

5. The learned Counsel appearing for the appellant would at the outset submit that the decision relied on by the Tribunal is not applicable, insofar as the same having been rendered under Section 80HHC (of Income Tax Act, 1961). Specific reliance is placed on the judgment of the Hon'ble Supreme Court in Commissioner of Income Tax v. Doom Dooma India Ltd. [(2009) 310 ITR 392 (SC)], wherein the actual meaning of the words “actual cost to the assessee” as found in Section 43(6) (of Income Tax Act, 1961), was held to be the actual cost incurred by the assessee in acquiring the plant and machinery de hors the fact whether the acquisition was in the previous year or not. Even if it was acquired in years prior to the previous year and if no depreciation has been claimed, then there could be a claim raised to the extent of the actual cost itself, by virtue of the clear statutory provision, argues learned Counsel.

6. Doom Dooma India Ltd. (supra) was a case in which under Rule 8 (of Income Tax Rules, 1962), when depreciation was claimed, the same was disallowed to the extent of 100%. The claim of the assessee was that it could have been disallowed only to the extent of 60%. The Honourable Supreme Court in the aforesaid decision followed Madeva Upendra Sinai v. Union of India and Others [1975 (98) ITR 209 (SC)] and quoted the following paragraph with approval.

“From the above conspectus, it is clear that the essence of the scheme of the Indian Income-tax Act is that depreciation is allowed, year after year, on the actual cost of the assets as reduced by the depreciation actually allowed in earlier years. It follows, therefore, that even in the case of assets acquired before the previous year, where in the past no depreciation was computed, actually allowed or carried forward, for no fault of the assessee, the "written-down value" may, under Clause (b) of section 43(6) (of Income Tax Act, 1961), also, be the actual cost of the assets to the assessee.”

The Assessing Officer has also relied on the very same decision, but has looked at the minority dissenting opinion, is the contention raised.

7. The learned Senior Counsel, Government of India (Taxes), contended that the legislature would never have contemplated granting of a double benefit. The assessee till that date was assessable under the AIT Act. There was also a provision in the AIT Act, i.e. Section 7 (of Income Tax Act, 1961), which permitted depreciation. Whatever had been claimed as depreciation from the actual cost of the assets acquired cannot again be granted under the IT Act, is the compelling argument.

8. We had a doubt as to the actual depreciation claimed by the assessee for the previous years. We, hence, directed the Assessing Officers under the AIT Act and under the IT Act to verify the earlier assessments for the previous years and file a report. Both the Assessing Officers were present before this Court and they have submitted separate reports on verification of the respective assessments. We have handed over copies of the same to the learned Counsel appearing for both sides. The report submitted by the Assistant Commissioner of State Tax, State Goods and Service Tax Department, Kottarakkara (who is now designated as the Assessing Officer under the AIT Act) is marked as Court exhibit Annexure-C1. The report of the Assistant Commissioner of Income Tax, Circle-I, Kollam, likewise is marked as Annexure-C2.

9. We see from Annexure-C1 report filed by the Assessing Officer under the AIT Act that the assessee has claimed depreciation in the earlier years when filing returns under the AIT Act. Annexure-C2 report of the Assessing Officer under the IT Act also indicates that the assets pertaining to the agricultural income has not been projected for depreciation under the IT Act for the previous years. The Assessing Officer points out that depreciation was claimed in the years 1998-99 to 2001-02 with respect to the building and plant & machinery of rubber sheeting factory, the income derived from which, being a manufacturing activity, however is not covered under the AIT Act. In such circumstances, one has to look at whether in allowing the depreciation on the basis of the written down value as available in Section 43(6)(b) (of Income Tax Act, 1961), the entire cost of the building and plant & machinery for the purpose of generation of agricultural income has to be allowed or not.

10. In this context, we place reliance on the decision in Madeva Upendra Sinai (supra). Therein the IT Act was extended with certain amendments to the Union Territories of Goa, Daman and Diu with effect from April 1, 1963. The question that arose before the Hon'ble Supreme Court was the constitutional validity of the Taxation Laws (Extension to Union Territories) (Removal of Difficulties) Order 2 of 1970. The Central Government by the aforesaid Regulation was empowered to cause issuance of General or Special Orders published in the official gazette to remove any difficulty arising in giving effect to the provisions of the Act. There was no law in force in the Union Territories of Goa, Daman and Diu for allowance in the nature of depreciation while computing the gross income. The law of income tax applicable earlier, levied tax at certain percentage of the gross receipts of an assessee. The issue was as to when the IT Act was introduced, the written down value could be that deemed as provided in Section 43(6)(b) (of Income Tax Act, 1961). We extract herein below the following paragraph:

“We are unable to accept the contention that but for the impugned proviso, the provisions of Section 32 (of Income Tax Act, 1961) and Section 43(6)(b) of the Income Tax Act, 1961 on its extension to Goa, Daman and Diu could not be given effect to and applied to the assessees in those territories. There could be no difficulty in computing the 'written down value' of the assets that had been acquired by the petitioners before the previous year, under clause (b) of Section 43(6) (of Income Tax Act, 1961). Since no depreciation was, in fact, allowed to the petitioners in the past under the Portuguese law in the first assessment under the Indian Income-tax Act, the written down value would, under clause (b) work out to be the actual cost of the assets less nil. Thereafter, in each succeeding year the depreciation actually allowed in the preceding year would be deducted causing yearly diminution of the written down value with consequent decrease in the depreciation allowed on that basis. Exactly, this was the manner in which the 'written down value' of the assets of the petitioners has been computed and depreciation allowed for several assessment years from 1964-65, onwards. This itself demonstrates that there was no difficulty in applying the aforesaid provisions to the cases of these assessees.”

11. The contention of the Department seems to be that there is a double taxation benefit granted to the assessee, insofar as the actual cost of the assets having been depreciated considerably in the years after its purchase, though not actually claimed under the IT Act. Admittedly the same was claimed under the AIT Act, and the allowance granted in computing the taxable agricultural income. The books of accounts as maintained by the assessee also discloses only the written down value of the assets, as available at the commencement of the financial year, after the depreciation claimed under the AIT Act for the previous years and that arrived at under the Companies Act. The question would be as to whether the depreciation already claimed for the very same assets under the AIT Act should be reduced to arrive at the written down value.

12. We extract herein below sub-Clauses (a) and (b) of Section 43(6) (of Income Tax Act, 1961):

“43(6) " written down value" means-

(a) in the case of assets acquired in the previous year, the actual cost to the assessee;

(b) in the case of assets acquired before the previous year, the actual cost to the assessee less all depreciation actually allowed to him under this Act, or under the Indian Income- tax Act, 1922 (11 of 1922 ), or any Act repealed by that Act, or under any executive orders issued when the Indian Income-tax Act, 1886 (2 of 1886), was in force:

Provided that in determining the written down value in respect of buildings, machinery or plant for the purposes of clause (ii) of sub-section (1) of section 32 (of Income Tax Act, 1961), "depreciation actually allowed" shall not include depreciation allowed under sub-clauses (a), (b) and (c) of clause (vi) of sub- section (2) of section 10 of the Indian Income- tax Act, 1922 (11 of 1922 ), where such depreciation was not deductible in determining the written down value for the purposes of the said clause (vi)”

13. There need not be any controversy raised on the interpretation of the aforesaid provision at sub-Clause (b). What can be reduced from the actual cost to the assessee is all depreciation actually allowed under the IT Act, 1961 or the IT Act, 1922 or any Act repealed by that Act or any executive orders issued when the Indian Income Tax Act, 1886 was in force. The AIT Act having not been specifically noticed and the depreciation allowed with respect to the income assessed to tax under any other enactments having not been excluded, there is no reason for this Court to come to a different finding as to the written down value which could be claimed as depreciation on the first year in which the assessee is assessed under the IT Act. We perfectly understand that the assessee was earlier assessed under the IT Act, but for its manufacturing activity and not its agricultural operations, the income from which was assessed under the AIT Act. The assets employed for agricultural operations were never accounted for computing the depreciation under the IT Act, since that income, prior to Rule 7A (of Income Tax Rules, 1962), was not exigible to tax under the IT Act.

14. The question arise since the entire income generated from the agricultural income was assessable to tax under the AIT Act, a State enactment. Only in the relevant assessment year i.e. 2002-03, the provision for a separate assessment under the AIT Act and IT Act came into force by virtue of the Income Tax Rules. Income from the manufacture of rubber which was earlier treated as agricultural income was made assessable under the IT Act to the extent of 35% of the income derived from the business. Hence, the assessee would be entitled to claim only 35% of the depreciation for the relevant assessment year. However, in computing such depreciation, should one adopt the entire cost of the plant and machinery or that shown as the written down value after reducing the depreciation allowed under the AIT Act, is the vexing question.

15. As we noticed, the deeming provision is very clear and there is nothing to exclude from the computation of the cost of the assets; the depreciation allowed under the AIT Act. The learned Senior Counsel appearing on behalf of the Revenue would contend that this Court has ample powers to iron out the creases and avoid a double benefit being conferred on the assessee. We have no doubt of such powers, but, whether it could be exercised in the present case is the question which troubles us. In ironing out creases we should not be accused of burning the cloth, by adding words into the statute to digress from the essential unambiguous intention.

16. The Rule providing division of income to be assessed respectively under the AIT Act and the IT Act was brought in, in the year 2002. The Government was quite aware of the provision available in the IT Act, 1961 by which the depreciation in cases, where it was not being claimed under the enactments as specified in Section 43(6)(b) (of Income Tax Act, 1961), can only be excluded and otherwise the written down value has to be deemed to be the cost of the assets. On apportioning the income from agriculture to be assessed under the respective enactments of the State and the Union; amendments ought to have been brought in accordingly to ensure that no double benefit accrues on an assessee.

17. We find that such amendments were brought in with retrospective effect as is seen from Explanation 7 to Section 43(6) (of Income Tax Act, 1961) which got inserted by the Finance Act, 2009 with effect from 1.4.2010. We extract below Explanation 7, for easy reference:-

“Explanation 7 to Section 43(6) (of Income Tax Act, 1961): For the purposes of this clause, where the income of an assessee is derived, in part from agriculture and in part from business chargeable to income-tax under the head “Profits and gains of business or profession”, for computing the written down value of assets acquired before the previous year, the total amount of depreciation shall be computed as if the entire income is derived from the business of the assessee under the head “Profits and gains of business or profession” and the depreciation so computed shall be deemed to be the depreciation actually allowed under this Act.”

The Explanation takes in the specific defect of double benefit being conferred on the assessee as argued by the learned Senior Counsel. The legislature thought it fit to give it effect from 1.4.2010. The assessment year herein is 2002-03 relating to the income of the previous year being 2001-02. The amendment does not apply to that year. The amendment brought in without any retrospective effect, further makes it clear that the legislature cured the defect, but however, did not do so for the years previous to the amendment and not for the relevant assessment year. Our hands are tied and this is not a situation in which casus omissus could be supplied. As has been held in J.K.Synthetics Ltd. Vs. C.T.O [(1994) 4 SCC 276] and Maruti Wire Industries Ltd. Vs. S.T.O Mattancherry [(2001) 3 SCC 735] “a legislative casus omissus cannot be supplied by a judicial interpretative process” (sic). On the above reasoning, we are unable to accept the dis-allowance of the depreciation and the computation made of the written down value. We answer the questions raised by the assessee in favour of the assessee and against the Revenue. The Assessing Officer is directed to employ the deeming provision for computing the written down value de hors the depreciation granted under the AIT Act and take 35% of the cost of the total assets as written down value, allowing the depreciation for the relevant assessment year to that extent. The Assessing Officer shall deem the written down value to be the cost of the assets and compute the depreciation allowable at 35% of such deemed written down value and apply it to the portion of the income derived from the agricultural business, that is assessable under the IT Act.

The Income Tax Appeal is allowed with the above observations. No costs.

K.VINOD CHANDRAN

JUDGE

ASHOK MENON

JUDGE

×

Similar Ripples

Questions

Court allows full depreciation claim on agricultural assets under IT Act

Write your CommentSimilar Posts

Generic

- Reportdata/730.pdf