Court Affirms Assessee's Right to Choose Depreciation Claims

Full News

Court Affirms Assessee's Right to Choose Depreciation Claims

Court Affirms Assessee's Right to Choose Depreciation Claims

The Gujarat High Court dismissed an appeal by the Revenue challenging the Income Tax Appellate Tribunal's decision. The court upheld the Tribunal's ruling allowing deductions under sections 80HHC (of Income Tax Act, 1961) and 80IA on gross total income, including income from other sources. It also affirmed that depreciation not claimed by the assessee cannot be forcibly allowed as a deduction.

Get the full picture - access the original judgement of the court order here.

Case Name:

Deputy Commissioner of Income Tax Vs Sun Pharmaceuticals India Ltd. (High Court of Gujarat)

Tax Appeal No. 93 of 2000

Date: 17th December 2014

Key Takeaways:

1. Deductions under sections 80HHC (of Income Tax Act, 1961) and 80IA can be claimed on gross total income, including income from other sources.

2. Depreciation is optional for the assessee, and the Assessing Officer cannot allow it if not claimed by the assessee.

3. The concept of block assets doesn't change the optional nature of depreciation claims.

4. The court relied on previous judgments, particularly CIT v. Mahendra Mills, to support its decision.

Issue:

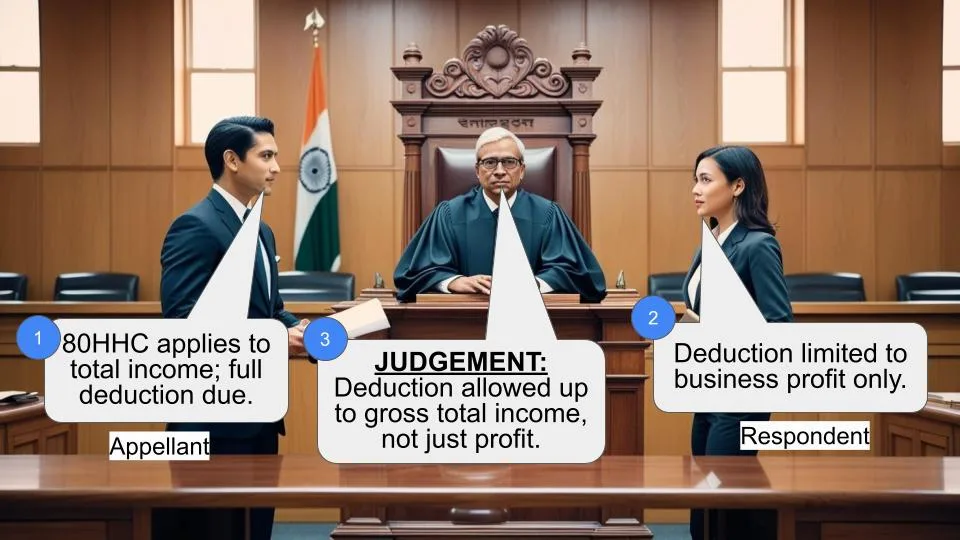

1. Whether the Appellate Tribunal is right in law and on facts in allowing the deduction under sections 80HHC (of Income Tax Act, 1961) and 80IA on gross total income inclusive of income from other sources?

2. Whether the Appellate Tribunal is right in law and on facts in holding that depreciation not claimed by the assessee cannot be allowed as a deduction despite the introduction of the concept of block assets?

Facts:

- The case involves Sun Pharmaceuticals Ind. Ltd. for the Assessment Year 1996-97.

- The assessee received income from lease rent and interest, which was taxed as income from other sources.

- The assessee claimed deductions under sections 80HHC (of Income Tax Act, 1961) and 80IA on their gross total income, including this income from other sources.

- The assessee chose not to claim depreciation on certain assets.

Arguments:

Revenue's Arguments:

1. Income from other sources should not be included in income eligible for deduction under sections 80HHC (of Income Tax Act, 1961) and 80IA.

2. Depreciation should be mandatorily allowed, even if not claimed by the assessee, due to the concept of block assets.

Assessee's Arguments:

1. Deductions under sections 80HHC (of Income Tax Act, 1961) and 80IA should be allowed on gross total income, including income from other sources.

2. Depreciation is optional, and the assessee has the right to choose whether to claim it or not.

Key Legal Precedents:

1. CIT v. Mahendra Mills (2000) 243 ITR 56:

This Supreme Court decision was relied upon to support the Tribunal's view.

2. CIT v. Arun Textiles 192 ITR 700:

The Gujarat High Court held that depreciation is optional for the assessee.

3. JOINT COMMISSIONER OF INCOME TAX v. MANDIDEEP ENG. AND PKG.IND. P. LTD. (2007) 292 ITR 1 (SC):

This case was cited regarding the independence of deductions under different sections.

Judgement:

The High Court dismissed the appeal and ruled in favor of the assessee, holding that:

1. The Appellate Tribunal was correct in allowing deductions under sections 80HHC (of Income Tax Act, 1961) and 80IA on gross total income, including income from other sources.

2. The Appellate Tribunal was right in holding that depreciation not claimed by the assessee cannot be forcibly allowed as a deduction, even with the introduction of the concept of block assets.

FAQs:

Q1: Can an assessee choose not to claim depreciation on certain assets?

A1: Yes, the court affirmed that depreciation is optional for the assessee, and they can choose not to claim it on certain assets.

Q2: Does the concept of block assets make depreciation mandatory?

A2: No, the court ruled that the concept of block assets doesn't change the optional nature of depreciation claims.

Q3: Can deductions under sections 80HHC (of Income Tax Act, 1961) and 80IA be claimed on income from other sources?

A3: Yes, the court upheld that these deductions can be claimed on gross total income, including income from other sources.

Q4: What was the significance of the CIT v. Mahendra Mills case in this judgment?

A4: The CIT v. Mahendra Mills case was a key precedent that supported the Tribunal's view and influenced the High Court's decision.

Q5: Can the Assessing Officer allow depreciation if it's not claimed by the assessee?

A5: No, the court ruled that if the assessee chooses not to claim depreciation, the Assessing Officer cannot allow it while computing the income.

1. By way of this appeal, the Revenue has challenged the judgment and order dated 6.3.2000 passed by the Income Tax Appellate Tribunal, Ahmedabad Bench “C” in ITA No. 1261/Ahd/1999 for AY 1996-97.

2. At the out-set, it is to be noted that when

the present appeal was preferred by the Revenue,

the Revenue felt that the challenge should be

only to the effect as to whether the Tribunal is

right in law and on facts in allowing the

deduction u/s. 80HHC (of Income Tax Act, 1961) and 80IA on gross total

income inclusive of income from other sources as

per the provisions of sec. 80AB (of Income Tax Act, 1961). According to the

Revenue, other sources could not be included in

the income eligible for deduction under sec.

80HHC and 80IA. It is an admitted position by and

between the parties that the assessee received

income from lease rent and interest which has

been taxed, according to the AO as income from

other sources.

3. The CIT(Appeals), on appeal preferred by the

assessee, the present respondent herein, held

that the claim for deduction under sec. 80HHC (of Income Tax Act, 1961) and

80IA was allowable. This aspect has aggrieved the

Revenue and following question was posed for

consideration of this Court:

“Whether the Appellate Tribunal is right

in law and on facts in allowing the

deduction u/s. 80HHC (of Income Tax Act, 1961) and 80IA on gross

total income inclusive of income from

other sources ?”

4. This Court in the case of Jt. Commissioner of

Income Tax v. United Phosphorous Ltd. in Tax

Appeal No. 2 of 2002, has held as follows:

“7. Similarly, in Tax Appeal No.175/2001

disposed of by the coordinate Bench, the

following observations are relevant for

our purpose;

“We have heard the learned advocates

at length and have also perused the

order of the Tribunal and judgment

delivered in the case of CIT v.

Mahendra Mills, 243 ITR 56. In our

opinion, no substantial question of

law arises in this appeal as the

Tribunal has rightly decided the

appeal in view of the ratio laid

down by the Hon'ble Supreme Court in

the case of Mahendra Mills (supra).

It is also pertinent to note that

the Tribunal had taken similar view

in the case of Sun Pharmaceutical

Industries v. Deputy Commissioner of

Income tax (Assessment) in I.T.A.

Nos. 2355/A/98, 1261 and 1190/A/89

for the Assessment Years 199596 and

199697 and against the said view

taken by the Tribunal in the case of

Sun Pharmaceutical Industries

(supra), the revenue had not filed

an appeal though an appeal has been

filed by the revenue in the said

case on other points. It has been

submitted by learned advocate Shri

Qureshi that the revenue proposes to

amend the appeal memo filed in the

case of Sun Pharmaceutical

Industries, but as on today, the

fact remains that the issue

regarding claim of depreciation in

the case of Sun Pharmaceutical

Industries decided by the Tribunal

has not been challenged by the

revenue.

Looking to the view expressed by

the Supreme Court in the case of

Mahendra Mills (supra), in our

opinion, the Tribunal was justified

in taking the view with regard to

the depreciation in the instant case

and, therefore, we do not find any

substantial question of law involved

in this appeal and, therefore, the

appeal is dismissed.

8. In view of the above, the question

of law raised in this appeal is answered

in favour of the assessee and against

the Revenue.”

5. Even Tax Appeal No. 175/2001 has been

disposed off by the co-ordinate Bench of this

Court relying on the decision of the Apex Court

in the case of CIT V. Mahendra Mills, reported in

243 ITR 56.

6. The learned counsel for the appellant felt

that as the aforesaid question was not raised in

this appeal should be raised in this appeal

afresh after many years that the issue involved

in the present case, requires re-consideration,

and therefore, Civil Application being OJ CA No.

546 of 2010 was filed after Tax Appeal No. 2/2002

was decided, and pursuant to the order passed in

OJCA No. 546 of 2010, vide order dated

26.11.2014, the following substantial question of

law has been framed by this Court, which reads

as under:

“Whether, the Appellate Tribunal is

right in law and on facts in holding

that depreciation not claimed for by the

assessee, cannot be allowed as a

deduction despite the introduction of

the concept of block assets ?”

6. We have heard the learned counsels appearing

for the parties and considered the submissions.

Mr. Soparkar learned counsel at the out set

submitted that the question no. 2 cannot be re-

agitated as it is covered by the decision of this

Court in Tax Appeal No. 175 of 2001 as well as

Tax Appeal No. 2/2002 decided on 17.11.2014.

However, Mr. Parikh learned counsel for Revenue

submitted that the question of law as raised in

this case was never decided in those matters,

and therefore, he requested that the question of

law be decided afresh. As both the questions of

law are inter connected are decided together.

7. We have heard the learned counsel appearing

for the parties at length. According to the

learned counsel Mr. Parikh, the decision of the

Full Bench of the Bombay High Court in the case

of Plastiblends India Limited v. Additional

Commissioner of Income-tax & Ors., reported in

[2009] 318 ITR (Bom)[FB] will have to be applied

to the facts of this case. Ld. Counsel has relied

on the grounds of challenge raised in this appeal

as it original was and amended.

8. In contra, learned counsel Mr. Soparkar for

revenue has drawn our attention to the decision

of the Hon’ble Supreme Court in the case of

Commissioner of Income Tax v. Mahendra Mills,

reported in [2000] 243 ITR 56 and the decision of

this Court in Tax Appeal 2/2002 and Tax Appeal

No. 175/2001. It is submitted that the questions

of law are concluded, but no elaborate reasons

are to be given in view of the finding of fact

and the question also having been answered in the

case of Manehdra Mills (supra), and therefore,

the decision of the Hon’ble Supreme Court will

enure for the benefit of the present assessee as

the amendment is after 2000 and not prior

thereto.

9. The decision cited by the learned counsel for

the Revenue of the Bombay High Court (supra)

cannot be applied in the facts of this case and

as far as this question of law is concerned.

10. This takes us to the original first question

wherein also the learned counsel for the

appellant has placed reliance on the decision of

the Full Bench of Bombay High Court Plastiblends

India Limited v. Additional Commissioner of

Income-tax & Ors., reported in [2009] 318 ITR

(Bom)[FB] and submitted that this appeal should

be allowed.

11. As far as this aspect is concerned, the

finding of fact recorded by the CIT(Appeals)

which reads as under:

“3. The contentions of the appellant and

the reasons given by the Assessing

Officer in allowing full depreciation

are considered. The decision of CIT v.

Mother India Refrigeration (P) Ltd.

(supra) relied on by the assessing

Officer is not applicable in the instant

case as the issue as to whether

depreciation is optional or not was

never before the Supreme Court. The

second decision of Madras High Court in

the case of Dasa Prakash Bottling Co. v.

CIT (supra) will also not be applicable

as the Gujarat High Court,which is

jurisdictional High Court in the case of

CIT v. Arun Textiles 192 ITR 700 did not

agree with this decision. In the case of

Arun Textiles (supra), the Gujarat High

Court held that there is nothing in the

provisions of section 32(1) (of Income Tax Act, 1961) read with

section 29 (of Income Tax Act, 1961),

to indicate that even when no claim is

made for allowing deduction in respect

of the depreciation under section 32(1) (of Income Tax Act, 1961),

the Income-tax Officer is bound to allow

a deduction. Under the scheme of the

Act, income is to be charged regardless

of depreciation on the value of the

assets and it is only by way on an

exception that section 32(1) (of Income Tax Act, 1961) grants an

allowance in respect of depreciation on

the value of the capital assets

enumerated therein. There is intrinsic

evidence under section 43(6)(b) (of Income Tax Act, 1961) of the

Act in the expression “less all

depreciation actually allowed” to show

that it is not as if all allowable

deductions are to be granted by the

Income-tax Officer even when the

assessee does not want the same. Sub-

section (2)(a) of Section 143(3) (of Income Tax Act, 1961) of the

Act provides that an assessee can object

to such deduction made under section

143(1). Therefore, the assessee can

come forward in such a case and make

clear its intention that it does not

want to compute depreciation on the

assets and wants no benefit of claiming

any depreciation in respect thereof. The

Circular of CBDT 29 D (XIX-4) of 1965

(F. No. 45/239/65-ITJ), dated 31.8.1996)

directed that, “where the required

particulars have not been furnished by

the assessee and no claim for

depreciation has been made in the

return, the Income-Tax Officer should

estimate the income without allowing

depreciation allowance.” Respectfully

following the decision of the Gujarat

High Court, I hold that the depreciation

is optional to the assessee and once he

chooses not to claim it, the Assessing

Officer cannot allow it while computing

the income. Further, once the

depreciation is option, applying the

same ratio of Gujarat High Court and

other Courts, it will be optional for

block of assets also. It is not

necessary that the depreciation is

allowable not allowable as a whole. The

assessee can claim it partly also in

respect of certain block of assets and

not claim in respect of other block of

assets. I, therefore, direct the

Assessing Officer to withdraw

depreciation allowance of Rs.

85,24,227/- not claimed by the

appellant.”

12. The Tribunal has upheld the well reasoned

finding of CIT(Appeals) in computing and

analyzing the gross business profit. The

provisions of section. 80IA read with section

80HHC reads as follows:

[Deductions in respect of profits and

gains from industrial undertakings or

enterprises engaged in infrastructure

development, etc.

Sec: 80IA:[(1) Where the gross total

income of an assessee includes any

profits and gains derived by an

undertaking or an enterprise from any

business referred to in sub-section (4)

(such business being hereinafter

referred to as the eligible business),

there shall, in accordance with and

subject to the provisions of this

section, be allowed, in computing the

total income of the assessee, a

deduction of an amount equal to hundred

per cent of the profits and gains

derived from such business for ten

consecutive assessment years.]

(2) The deduction specified in sub-

section (1) may, at the option of the

assessee, be claimed by him for any ten

consecutive assessment years out of

fifteen years beginning from the year in

which the undertaking or the enterprise

develops and begins to operate any

infrastructure facility or starts

providing telecommunication service or

develops an industrial park [ or

develops a special economic zone

referred to in clause (iii) of sub-

section (4)] or generates power or

commences transmission or distribution

of power [or undertakes substantial

renovation and modernisation of the

existing transmission or distribution

lines.

Sec: 80HHC:[(1) Where an assessee, being

an Indian company or a person (other

than a company) resident in India, is

engaged in the business of export out of

India of any goods or merchandise to

which this section applies, allowed, in

computing the total income of the

assessee, [ a deduction to the extent of

profits, referred to in sub-

section(1B),] derived by the assessee

from the export of such goods or

merchandise.”

13. The submission of learned counsel for

respondent as is based on the decision of the

Hon’ble Supreme Court in the case of JOINT

COMMISSIONER OF INCOME TAX v. MANDIDEEP ENG. AND

PKG.IND. P. LTD. reported in [2007] 292 ITR 1

(SC), wherein, the Hon’ble Supreme Court has held

as follows:

“The point involved in the present case

is whether sections 80HH and 80-I of the

Income-Tax Act, 1961, are independent of

each other and therefore a new

industrial unit can claim deductions

under both the sections on the gross

total income independently or that

deduction under section 80-I (of Income Tax Act, 1961) can be

taken on the reduced balance after

taking into account the benefit taken

under section 80HH (of Income Tax Act, 1961).”

12. The fact that the Tribunal and the CIT(A)

have concurred, we are not persuaded to take a

different view then that taken by both the

authorities below as the orders are neither

perverse nor against settled legal proposition of

law on the contrary they are based on correct

interpretation of law and decisions of Apex Court

and this Court.

13. We hold that (1) that the Appellate Tribunal

is right in law and on facts in allowing the

deduction u/s. 80HHC (of Income Tax Act, 1961) and 80IA on gross total

income inclusive of income from other sources. As

far as newly added question is concerned, there

also we hold that the the Appellate Tribunal is

right in law and on facts in holding that

depreciation not claimed for by the assessee,

cannot be allowed as a deduction despite the

introduction of the concept of block assets. The

questions are answered in favour of assessee and

against the Revenue. The Tax Appeal stands

dismissed.

(K.S.JHAVERI, J.) (K.J.THAKER, J)

×

Similar Ripples

Questions

Court Affirms Assessee's Right to Choose Depreciation Claims

Write your CommentSimilar Posts

Generic

- Reportdata/4224.pdf