Court Approves Late PF and ESI Payments, Overturns Tax Disallowance

Full News

Court Approves Late PF and ESI Payments, Overturns Tax Disallowance

Court Approves Late PF and ESI Payments, Overturns Tax Disallowance

It's about a company that paid their Provident Fund (PF) and Employees State Insurance (ESI) contributions a few days late, but still before filing their tax return. The tax department wasn't happy about this and tried to disallow these expenses. But guess what? The Income Tax Appellate Tribunal sided with the company, and now the High Court has backed that decision. Let's dive into the details.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Dharmendra Sharma (High Court of Delhi)

ITA 644/2007

Date: 28th November 2007

Key Takeaways:

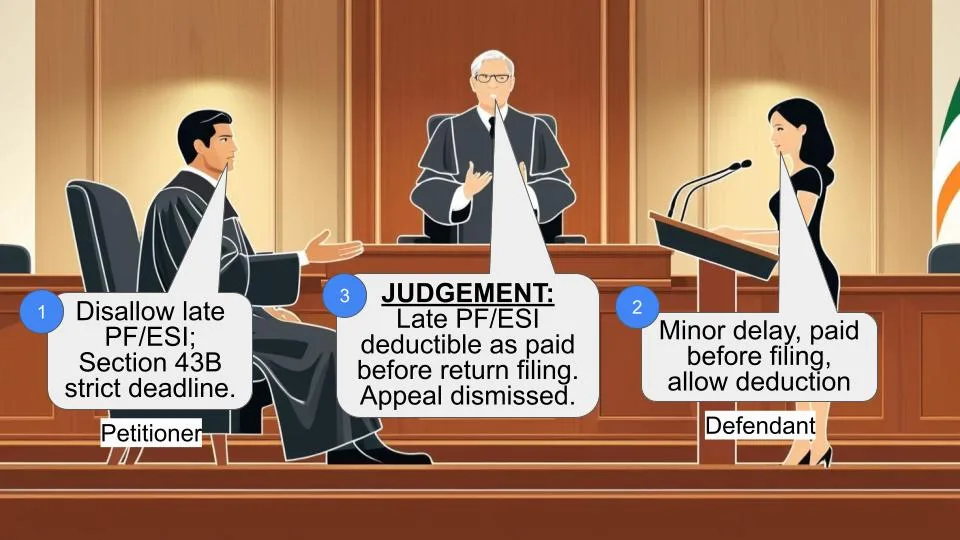

1. Even if PF and ESI payments are made a few days after the grace period, they can still be allowed as deductions if paid before filing the tax return.

2. The court favors a more lenient approach to Section 43B (of Income Tax Act, 1961), especially for minor delays.

3. This judgment could be a relief for businesses struggling with tight payment deadlines.

Issue:

The main question here is: Can a company claim deductions for PF and ESI contributions that were paid just a few days after the grace period but before filing the tax return, or should these be disallowed under Section 43B (of Income Tax Act, 1961)?

Facts:

1. Our company (the assessee) paid their PF and ESI contributions 2 to 4 days after the grace period ended.

2. However, they made these payments before filing their tax return.

3. The Assessing Officer wasn't happy and added back Rs. 10,37,737 for PF and Rs. 1,88,172 for ESI to the company's taxable income.

4. The Commissioner of Income Tax (Appeals) agreed with the Assessing Officer.

5. But then, the Income Tax Appellate Tribunal stepped in and reversed this decision.

6. Now, the tax department is appealing to the High Court, hoping to overturn the Tribunal's decision.

Arguments:

The company's side:

- They say it was just a "technical default" - the payments were only a few days late.

- They made the payments before filing their tax return, which should be the real deadline.

The tax department's side:

- Rules are rules, and the payments were made after the grace period specified in Section 43B (of Income Tax Act, 1961).

- They argue that the law should be strictly interpreted, and late payments shouldn't be allowed as deductions.

Key Legal Precedents:

Here's where it gets interesting! The court looked at two important cases:

1. Commissioner of Income Tax v. George Williamson (Assam) Ltd. (2006) 284 ITR 619 (Gau)

2. CIT vs. Vinay Cement Ltd. (2007) 213 CTR (SC) 268

In the George Williamson case, the Supreme Court said that if the company contributed to the provident fund before filing the return, they should get the benefit under Section 43B (of Income Tax Act, 1961). This was a big deal and really helped our company's case.

Judgement:

Good news for the company! The High Court dismissed the tax department's appeal. They said:

1. The Supreme Court's decision in the George Williamson case applies here.

2. No "substantial question of law" arose from this case.

3. Basically, they're saying that as long as you pay before filing your return, a few days' delay isn't a big deal.

FAQs:

1. Q: Does this mean companies can be relaxed about PF and ESI payment deadlines?

A: Not exactly. It's always best to pay on time, but this judgment provides some leeway for minor delays.

2. Q: What's the significance of "before filing the return"?

A: It seems the courts are more concerned with whether the payment was made before the company claimed the deduction, rather than strict adherence to the original due date.

3. Q: Could this judgment be applied to other types of payments under Section 43B (of Income Tax Act, 1961)?

A: Possibly, but it's best to consult with a tax professional. Each case can have unique circumstances.

4. Q: What does "no substantial question of law" mean?

A: It means the court felt the existing law was clear enough to decide this case without needing to interpret or create new legal principles.

1.The Revenue is aggrieved by an order dated 12th October, 2006 passed by the Income Tax Appellate Tribunal, Delhi Bench ?F?, New Delhi (`the Tribunal?) in ITA No. 2413/Del/2004 relevant for the Assessment Year 2001-2002.The case relates to the addition of an amount of Rs.10,37,737/- and Rs.1,88,172/- made by the Assessing Officer on account of delayed payment of Provident Fund and Employees State Insurance respectively. According to the Assessee, the amount was paid within 2 to 4 days after the grace period provided under Section 43B (of Income Tax Act, 1961) (`the Act?) but before filing the return. According to the Assessee, it was at best a technical default.

2.The Assessing Officer did not accept the view of the Assessee and the Commissioner of Income Tax (Appeals) [CIT (A)] upheld the view of the Assessing Officer. However, the Tribunal has reversed the decision of the CIT(A).

3.Learned counsel for the Assessee has placed before us a decision of the Gauhati High Court in Commissioner of Income Tax v. George Williamson (Assam) Ltd., [2006] 284 ITR 619(Gau). This decision was taken in appeal before the Supreme Court and by an order dated 7th March, 2007, the Supreme Court observed that it was concerned with the law as it stood prior to the amendment of Section 43-B (of Income Tax Act, 1961). The Assessee was entitled to claim the benefit provided under Section 43-B (of Income Tax Act, 1961) for that period particularly in view of the fact that he had contributed to provident fund before filing the return. Accordingly, the SLP filed by the Revenue against the decision of Gauhati High Court was dismissed.

4.The decision of the Supreme Court is fully applicable to the facts of the present case in view of what we have already mentioned above.

5.Under the circumstances, no substantial question of law arises for our consideration.

6.The appeal is dismissed.

7.ITA Nos. 642/2004, 644/2004, 717/2004 and 497/2005 which raise a similar issue be listed for directions on 29th November, 2007, so that they can be disposed of in terms of today?s order. MADAN B. LOKUR, J S.MURALIDHAR, J NOVEMBER 28, 2007

×

Similar Ripples

Questions

Court Approves Late PF and ESI Payments, Overturns Tax Disallowance

Write your CommentSimilar Posts

Generic

- Reportdata/5130_.pdf