Court Can't Play Appellate Role in Black Money Act Cases Under Article 226

Full News

Court Can't Play Appellate Role in Black Money Act Cases Under Article 226

Court Can't Play Appellate Role in Black Money Act Cases Under Article 226

This case involves a petition filed under Article 226 of the Indian Constitution challenging a penalty order issued under the Black Money Act. The High Court dismissed the petition, stating it cannot act as an appellate authority in such matters, and directed the petitioner to seek appropriate remedies under the Black Money Act.

Get the full picture - access the original judgement of the court order here

Case Name:

Thomas Mathew vs Income Tax Officer (High Court of Kerala)

WP(C).No.10200 of 2020

Date: 25th May 2020

Key Takeaways:

1. High Courts cannot act as appellate authorities in Black Money Act cases under Article 226.

2. Proper remedies for challenging penalty orders exist within the Black Money Act itself.

3. Non-disclosure of foreign assets in Schedule FA can lead to penalties, even if acquired from non-taxable income.

4. Circulars issued by tax authorities, while not binding, can provide guidance in interpreting the law.

Issue:

Can the High Court, under Article 226 of the Constitution of India, exercise the role of an appellate authority to deal with controversies arising from orders passed under the Black Money Act?

Facts:

1. The petitioner, Thomas Mathew, was a Non-Resident Indian employed abroad as a Bank Professional.

2. He returned to India after retirement and filed an income tax return for the assessment year 2016-17.

3. The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act 2015 was introduced.

4. The petitioner filed a revised return on 30.8.2018, disclosing details of foreign assets in Schedule FA.

5. The Income Tax Officer imposed a penalty of Rs.10 lakhs for the assessment year 2016-17.

6. The petitioner challenged this order through a writ petition under Article 226 of the Constitution.

Arguments:

Petitioner's Arguments:

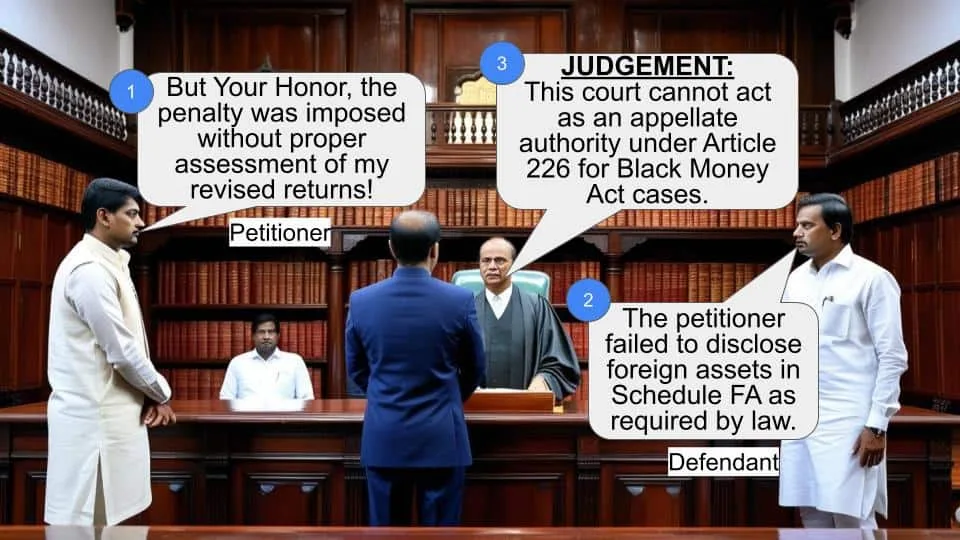

1. The penalty was imposed without an assessment of the revised returns .

2. There was no case of nondisclosure of assets or accumulation of black money.

3. The assets were acquired from non-taxable income earned as a non-resident.

4. The petitioner was under a bonafide belief that Schedule FA disclosure was only necessary from assessment year 2017-18.

Tax Authority's Position:

1. The penalty was imposed under Section 43 of the Black Money Act for failure to furnish information or furnishing inaccurate particulars about foreign assets.

Key Legal Precedents:

While no specific case laws were cited, the judgment refers to:

1. Section 3 of the Black Money Act, which came into force after April 2016.

2. Sections 10, 11, 12, 15, 16, 17, and 18 of the Black Money Act, outlining assessment procedures and appeal mechanisms.

3. Section 43 of the Black Money Act, empowering tax officers to impose penalties.

Judgement:

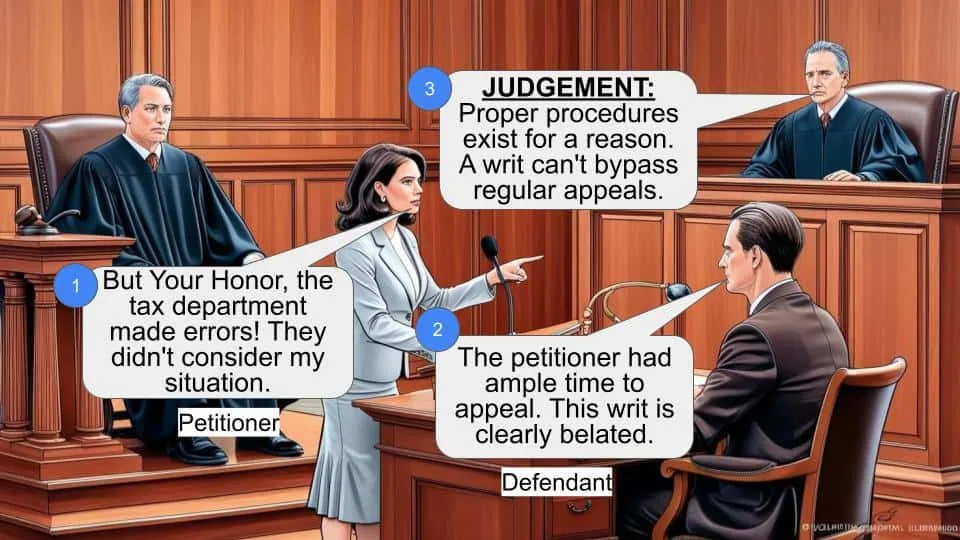

1. The High Court dismissed the writ petition.

2. It held that under Article 226, it cannot exercise the role of an appellate authority defined under the Black Money Act.

3. The court noted that the petitioner has the right to appeal the order through proper channels as defined in the Black Money Act.

4. The limitation period for appeal was extended due to the COVID-19 lockdown.

FAQs:

Q1: Can I directly approach the High Court to challenge a penalty under the Black Money Act?

A1: No, the High Court has clarified that it cannot act as an appellate authority in such cases under Article 226.

Q2: What should I do if I disagree with a penalty imposed under the Black Money Act?

A2: You should follow the appeal procedures outlined in the Black Money Act, such as appealing to the Commissioner of Appeals under Section 15 (of Income Tax Act, 1961).

Q3: Does non-disclosure of foreign assets always lead to penalties, even if the income was non-taxable?

A3: Yes, the judgment suggests that non-disclosure in Schedule FA can lead to penalties, regardless of the source of income.

Q4: Are CBDT circulars legally binding?

A4: No, the court clarified that circulars are not binding but can provide guidance in interpreting the law.

Q5: What is the penalty for non-disclosure of foreign assets under the Black Money Act?

A5: As per Section 43 (of Income Tax Act, 1961), the penalty can be up to ten lakh rupees (Rs.10 lakhs).

1. Petitioner in the instant case sought the indulgence of this Court under Article 226 of the Constitution of India challenging the order Ext.P8 dated 17.3.2020 of Income Tax Officer, Non-Co-operative Ward -1(5) Cochin whereby the penalty of Rs.10 lakhs for the assessment year 2016-17 has been imposed and further called upon to deposit the same within a period of 30 days.

2. According to the petitioner, he was a Non Resident Indian employed abroad as a Bank Professional and investments made by the petitioner from such income, was not liable to any tax in India. After having attained retirement, he returned to India and filed his income tax return for the assessment year 2016-17 declaring the total income of Rs.46,81,590/-. In the meanwhile, the Government of India introduced the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act 2015 (hereinafter referred to as 'Black Money Act').

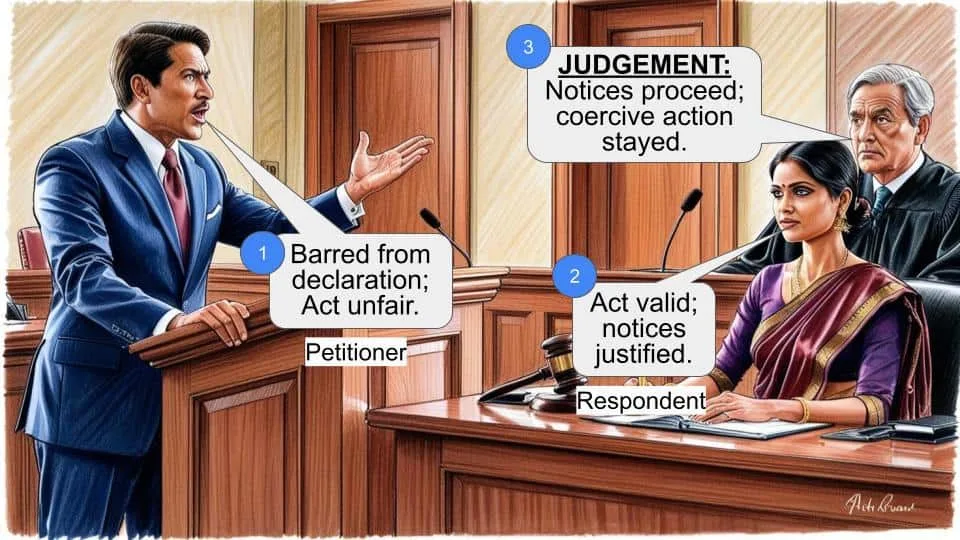

Petitioner was under the bonafide belief that disclosure under Schedule FA was to be made only from the assessment year 2017-18, subsequently was advised even for the assessment year 2016-17 to disclose details of foreign assets owned to be included in the Schedule FA. Accordingly, petitioner filed a revised return on 30-8.2018, but since the period prescribed for filing revised return under Section 139(5) (of Income Tax Act, 1961) expired, the aforementioned return was filed physically, evident from acknowledgment Ext.P3.

3. Sri.Abraham Markose, Learned Senior Counsel submits that the petitioner was surprised to receive a notice dated 17.9.2018 under Section 43 of the Black Money Act, whereby the Officer concerned contemplated to impose a penalty for failure to furnish the return of income and information. The aforementioned notice was duly replied giving extensive details with a further request to drop the aforementioned penalty proceedings. Petitioner appeared and filed a detailed objection on 11.3.2016 as per Ext.P6. During the aforementioned hearing reliance was also laid to the Central Board of Direct Tax circular No.13 dated 6.7.2016, particularly the Question and Answer No.17 evident from Ext.P7. He further submitted that the petitioner was astounded to receive the impugned order Ext.P8 reflecting the imposition of penalty of Rs.10 lakhs but urged though appeal under Section 15 of the Black Money Act lies before the Appellate authority, being a creature under statute but filing of same would be a futile exercise, for, as per the question No.18 the penalty can be only imposed only if Schedule FA is not filed. It is a settled law that the High Court is not bound by the Circular, being only directive in nature.

4. The Rule making authority cannot override or go beyond the provisions of the Act or the spirit of the law. The preamble of the Black Money Act aims at only to curb the menace of black money. It was next contended that the exclusive order under Section 43 (of Income Tax Act, 1961) ibid cannot be imposed without there being an assessment on the revised returns. It is no case of any nondisclosure of assets or accumulation of any black money, therefore, the alleged reasoning regarding nondisclosure is without any foundation or basis. Section 43 of the Black Money Act can only apply to the assets which are in the nature of black money or assets for which there is no explanation as to the source. Mere nondisclosure of the same in Schedule FA would not make any asset or income illegally acquired as black money.

5. The charging Section 3 (of Income Tax Act, 1961) deals with any income from any source outside India, which is undisclosed in the return of income or value of any undisclosed assets located outside India. The IT returns and Schedule FA only requires the disclosure. Clause 13 and Question No.17 of the Circular 15 reported on 6.7.2016 ibid conforms that the report in Schedule FA would not bring to tax to such undeclared assets, whereas in the instant case, assets have acquired out of non-taxable income earned by the assessee, while he was a non-Resident and thus the non- reporting of such non-taxable assets cannot attract the penalty as contemplated under section 43 (of Income Tax Act, 1961). The Clarification given in Paragraph 18 of the circular ibid is vague and not in accordance with the provisions of the Act or Income tax Act. The Rule making authority cannot for the sake of repetition override or go beyond the provisions of the Act or spirit of law.

6. Petitioner was under a bonafide belief that the disclosure of Schedule FA was only necessary for assessment year 2017-2018, whereas the Act was only introduced in the assessment year 2016-17. Petitioner filed a revised return rectifying the defects during the assessment year 2016-17, but almost 1 and 1⁄2 months after filing of the revised returns.

Thereafter, petitioner was served with a notice dated 17.9.2018. It is a settled law that where an assessee had not committed an intentional error by bonafide or inadvertent, in other words, there was no willful intention, thus, penalty cannot be imposed.

7. I have heard learned Counsel for the parties and appraised the paper book and as well the provisions of law, referred to above. I am of the view there is no force or merit in the submission.

8. The aforementioned Black Money Act came into force in the year 2016, whereas the charging Section 3 (of Income Tax Act, 1961), which is extracted herein below came into force after April, 2016 specifying the charging of the tax on every assessee for every assessment year, post 1st April 2016.

“Section 3 (of Income Tax Act, 1961) Charge of tax (1) There shall be charged on every assessee for every assessment year commencing on or after the 1st day of April, 2016 subject to the provisions of this Act, a tax in respect of his total undisclosed foreign income and asset of the previous year at the rate of thirty per cent of such undisclosed income and asset.

Provided that an undisclosed asset located outside India shall be charged to tax on its value in the previous year in which such asset comes to the notice of the Assessing Officer.

(2) For the purpose of this section “value of an undisclosed asset” means the fair market value of an asset (including financial interest in any entity) determined in such manner as may be prescribed.

9. As per Section 11(2) (of Income Tax Act, 1961) undisclosed asset located outside India means an asset (including financial interest in any entity) located outside India, held by the assessee in his name or in respect of which is a beneficial owner, and has no explanation about the source of investment in such asset or explanation given to him is in the opinion of the Assessing Officer unsatisfactorily.

10. The assessment proceedings are provided under Section 10 (of Income Tax Act, 1961). The procedure for assessment has been prescribed under Sections 10 (of Income Tax Act, 1961), 11 and 12 of the Act and the remedy of appeal before the Commissioner of Appeal is under Section 15 (of Income Tax Act, 1961) and the procedure to be followed in appeal is under Section 16 (of Income Tax Act, 1961) and powers of Commissioner is under section 17 (of Income Tax Act, 1961).

11. As per Section 18 (of Income Tax Act, 1961), appeal to the appellate Tribunal would lie against an order passed under Section 15 (of Income Tax Act, 1961). The provisions of appeal would also applicable in any proceedings initiated under Section 43 (of Income Tax Act, 1961), which is reproduced below, which empowers the tax officer to initiate proceedings of imposition of penalty on account of failure to furnish any incorrect particulars about the asset including financial interest in any entity located outside India.

“Section 43 (of Income Tax Act, 1961) Penalty for failure to furnish in return of income, an information or furnish inaccurate particulars about an asset (including financial interest I any entity) located outside India.

- If any person, being a resident other than not ordinarily resident in India within the meaning of clause (6) of section 6 (of Income Tax Act, 1961), who has furnished the return of income for any previous year under sub-section (1) or sub-section (4) or sub-section (5) of section 139 (of Income Tax Act, 1961), fails to furnish any information or furnishes inaccurate particulars in such return relating to any asset (including financial interest in any entity) located outside India, held by him as a beneficial owner or otherwise, or in respect of which he was a beneficiary, or relating to any income from a source located outside India, at any time during such previous year, the Assessing Officer may direct that such person shall pay, by way of penalty, a sum of ten lakh rupees:

Provided that this section shall not apply in respect of an asset, being one or more bank accounts having an aggregate balance which does not exceed a value equivalent to five hundred thousand rupees at any time during the previous year Explanation – The value equivalent in rupees shall be determined in the manner provided in the Explanation to section 42 (of Income Tax Act, 1961).

This clause relates to penalty for failure to furnish in return of income, an information or furnish inaccurate particulars about an asset (including financial interest in any entity) located outside India. This Clause seeks to provide that if any person being a resident other than not ordinarily resident in India within the meaning of clause (6) of section 6 (of Income Tax Act, 1961), who has furnished the return of income for any previous year under sub-section (1) or sub section (4) or sub-section (5) of section 139 (of Income Tax Act, 1961), fails to furnish any information or furnishes inaccurate particulars in such return relating to any asset (including financial interest in any entity) located outside India, held by him as a beneficial owner or otherwise, or in respect of which he was a beneficiary, or relating to any income from a source located outside India, at any time during such previous year, the Assessing Officer may direct that such person shall pay a penalty of ten lakh rupees.

The said clause further provides that no penalty shall be levied in respect of an asset, being one or more bank accounts having an aggregate balance which does not exceed a value equivalent to five hundred thousand rupees at any time during the previous year.”

12. No doubt the Circular has no binding force and therefore, the challenge to the circular cannot be a ground to negate the plea of the petitioner. But the fact remains that whether the impugned order reflects the adherence to the provisions of the circular of 2015 ibid or in terms of the provisions of the Black Money Act, this Court under Article 226 of the Constitution of India cannot exercise the role of an appellate authority defined under the Black Money Act to deal with the controversy if brought into motion. Petitioner is well within the right to assail the aforementioned order, as the impugned order is dated 17.3.2020 and the limitation in the instant case expired during the lock down but as per the Government directive and judgment of the Full Bench of this Court limitation prescribed already stood extended. Petitioner if so advised shall be at liberty to assail the aforementioned order. Any observation hereinabove would not prejudice the right of the petitioner in case the remedy is availed. In view of what has been noticed, this writ petition sans merit and accordingly, dismissed.

Sd/-

AMIT RAWAL JUDGE

WP(C).No.10200 OF 2020(Y)

APPENDIX PETITIONER'S/S EXHIBITS:

EXHIBIT P1 TRUE COPY OF THE ACKNOWLEDGMENT FOR INCOME TAX RETURN FILED FOR AY 2016-17.

EXHIBIT P2 TRUE COPY OF THE BLACK MONEY (UNDISCLOSED FOREIGN INCOME AND ASSETS) AND IMPOSITION OF TAX ACT, 2015.

EXHIBIT P3 TRUE COPY OF THE RETURN AND ACKNOWLEDGEMENT OF POSTAL RECEIPT.

EXHIBIT P4 TRUE COPY OF THE NOTICE DATED 17.9.2018 ISSUED UNDER SECTION 43 OF THE BLACK MONEY ACT.

EXHIBIT P5 TRUE COPY OF THE REPLY DATED 17.9.2019 FILED BY THE PETITIONER.

EXHIBIT P6 TRUE COPY OF THE REPRESENTATION DATED 11.3.2020.

EXHIBIT P7 TRUE COPY OF THE CBDT CIRCULAR NO.13 OF 2015 DATED 6.7.2015.

EXHIBIT P8 TRUE COPY OF THE ORDER DATED 17.3.2020.

×

Similar Ripples

Questions

Court Can't Play Appellate Role in Black Money Act Cases Under Article 226

Write your CommentSimilar Posts

Generic

- Reportdata/5961.pdf