Court Reconsiders Tax Refund Denial Due to Late Filing

Full News

Court Reconsiders Tax Refund Denial Due to Late Filing

Court Reconsiders Tax Refund Denial Due to Late Filing

In this case, the court dealt with a dispute over a tax refund claim that was initially denied because the tax returns were filed late. The court ultimately decided to set aside the previous orders denying the refund and directed the tax authorities to reconsider the application for a refund, taking into account the potential for genuine hardship.

Get the full picture - access the original judgement of the court order here

Case Name:

Deputy Commissioner of Income Tax and Another vs. Vasco Sales and Marketing Corporation (High Court of Kerala)

WA. No. 1152 of 2013 & WP(C).24109/2005

Date: 3rd July 2015

Key Takeaways:

- The case highlights the importance of Section 119(2)(b) (of Income Tax Act, 1961), which allows for the condonation of delays in filing tax returns to avoid genuine hardship.

- The court emphasized that the tax authorities must properly exercise their discretion under this section and consider the merits of the case.

- The decision underscores the court's role in ensuring that procedural technicalities do not unjustly prevent taxpayers from receiving refunds they are entitled to.

Issue

Can a taxpayer claim a refund if the tax return is filed late, and under what circumstances can the delay be condoned?

Facts

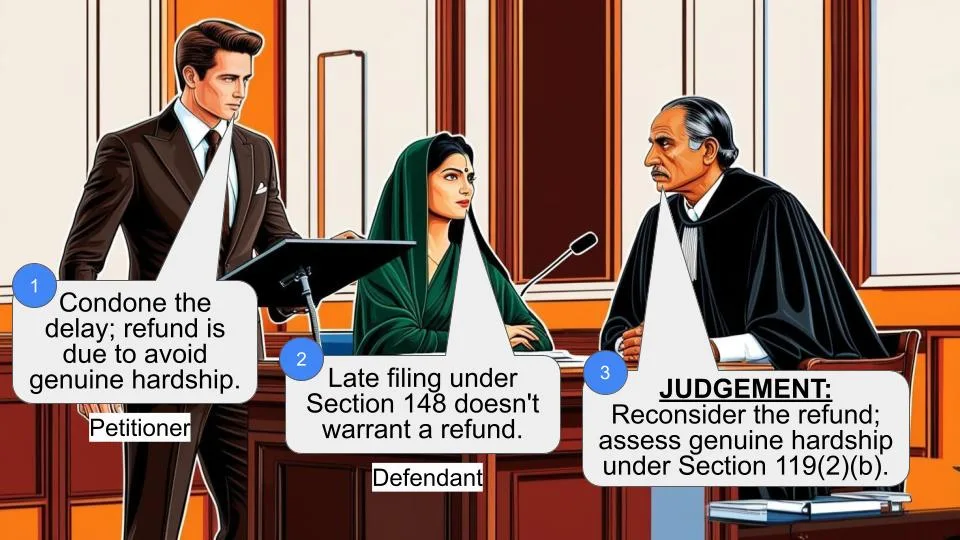

The taxpayer, Vasco Sales and Marketing Corporation, filed tax returns for the assessment years 1996-97 and 1997-98 after the due dates. They claimed a refund for the advance tax paid. The tax authorities rejected the refund claim due to the late filing. The taxpayer then sought to have the delay condoned under Section 119(2)(b) (of Income Tax Act, 1961), which allows for such condonation to avoid genuine hardship.

Arguments

- Taxpayer's Argument: The taxpayer argued that the delay should be condoned under Section 119(2)(b) (of Income Tax Act, 1961) to avoid genuine hardship, and that they were entitled to a refund of the advance tax paid.

- Tax Authorities' Argument: The authorities contended that the returns were filed in response to notices under Section 148 (of Income Tax Act, 1961), and as per the judgment in K. Sudhakar S. Shanbhag v. Income Tax Officer, the taxpayer was not entitled to a refund in such cases.

Key Legal Precedents

- K. Sudhakar S. Shanbhag v. Income Tax Officer: This case was cited to support the argument that a refund is not permissible when returns are filed in response to notices under Section 148 (of Income Tax Act, 1961).

- Section 119(2)(b) (of Income Tax Act, 1961): This section empowers the Central Board of Directors to authorize the condonation of delays in filing returns to avoid genuine hardship.

Judgement

The court set aside the previous orders (Exts. P13 and P16) that denied the refund claim. It directed the tax authorities to reconsider the taxpayer's applications (Exts. P14 and P15) for condonation of delay, emphasizing the need to assess whether genuine hardship would be avoided by allowing the refund.

FAQs

Q1: What does Section 119(2)(b) (of Income Tax Act, 1961) entail?

A1: It allows the Central Board of Directors to authorize the condonation of delays in filing tax returns to avoid genuine hardship, even after the statutory period has expired.

Q2: Why was the initial refund claim denied?

A2: The claim was denied because the tax returns were filed late, and the authorities initially did not find sufficient grounds to condone the delay.

Q3: What was the court's main concern in this case?

A3: The court was concerned that the tax authorities did not properly exercise their discretion under Section 119(2)(b) (of Income Tax Act, 1961) to consider the potential for genuine hardship.

Q4: What does this decision mean for taxpayers?

A4: It reinforces the possibility of obtaining a refund even if returns are filed late, provided that the delay can be justified under Section 119(2)(b) (of Income Tax Act, 1961) to avoid genuine hardship.

1. This writ appeal is filed by the respondents in W.P.(C)No.24109 of 2005. The writ petition was filed by the respondents herein challenging Ext.P13 order by which their claim for refund was rejected on the ground that return for the assessment years 1996-97 and 1997-98 were filed belatedly and Ext.P16 order, declining to condone delay in filing the returns. By the judgment under appeal, relying on the judgment of this Court in Pala Marketing Co-op. Society Ltd. v. Union of India and Others [2008 (1) KLJ 561], the learned Single Judge condoned the delay in applying for refund and remitted the case to the 3rd appellant to reconsider the application for refund afresh and pass orders thereon. It is this judgment which is impugned before us.

2.We heard the learned counsel for the appellants and the learned counsel appearing for the respondent.

3.Admittedly, returns for the assessment years 1996-97 and 1997-98 were filed belatedly on 30.06.1998 and 29.02.2000 respectively. In these returns, the assessee claimed refund of the advance tax paid. Ext.P13 order was passed rejecting their claim for refund on the ground that returns were filed after the due dates for both the assessment years and the claim for refund cannot be entertained. It was thereupon that the assessee filed Exts.P14 and P15 applications before the 2nd appellant to condone the delay in terms of Section 119(2)(b) (of Income Tax Act, 1961). On that application, Ext.P16 order was passed. In that order, the 3rd appellant held that the returns were filed in response to notices issued under Section 148 (of Income Tax Act, 1961) and that in such a case, the assessee will not be entitled to claim refund of

advance tax paid and relied on the judgment of the Bombay High Court in K. Sudhakar S. Shanbhag v. Income Tax Officer [(2000) 241 ITR 865]. The 3rd

appellant also held that the assessee has not properly explained the delay. It is these orders which are set aside by the learned Single Judge.

4.It is true that returns are to be filed before the

due date under Section 139(1) (of Income Tax Act, 1961) or (4) of the Income

Tax Act and in cases where returns are belatedly

filed or refund claims are made beyond the time

provided in Section 239 (of Income Tax Act, 1961), refund cannot be

claimed. However, Section 119(2)(b) (of Income Tax Act, 1961)

empowers the Central Board of Directors to authorize

any income tax authority, not being a Commissioner

(Appeals), to admit an application or claim for any

refund after the expiry of the period specified by or

under this Act for making such application or claim

and deal with the same on merits in accordance with

law. As is evident from this Section, the purpose of

conferring such authority is for “avoiding genuine

hardship”.

5.Section 119(2)(b) (of Income Tax Act, 1961) reads thus:

“119(2)(b): the Board may, if it considers it

desirable or expedient so to do for avoiding

genuine hardship in any case or class of cases, by

general or special order, authorize any income tax

authority, not being a Commissioner (Appeals) to

admit an application or claim for any exemption,

deduction, refund or any other relief under this

Act after the expiry of the period specified by

or under this Act for making such application or

claim and deal with the same on merits in

accordance with law.”

6.In the light of the above provision, when Exts.P14

and P15 applications were filed by the assessee, what

was required to be examined was whether, to avoid

genuine hardship to the assessee, it was necessary to

condone the delay in making the application for

refund. Ext.P16 order does not show that the

Commissioner has examined Exts.P14 and P15

applications in the manner as required under Section

119(2)(b). On the other hand, Commissioner has

discussed on the merits of the application and held

that the delay has not been properly explained and

that when returns are filed in response to notices

issued under Section 148 (of Income Tax Act, 1961), assessee will not be

entitled to claim refund of advance tax paid. In our

view, such an order does not reflect a proper

exercise of power under Section 119(2)(b) (of Income Tax Act, 1961) and for

that reason, Ext.P16 is unsustainable.

7.It is true that the Bombay High Court in the judgment

in K.Sudhakar S.Shanbhag (supra) has held that when

return is filed in response to a notice under Section

148, assessee is not entitled to claim refund.

However, if the Commissioner condones the delay in

exercise of his power under Section 119(2)(b) (of Income Tax Act, 1961), the

fact that return was filed in response to a notice

under Section 148 (of Income Tax Act, 1961) would pale into insignificance.

8.In this case, according to us, when Ext.P16 order was

passed in an improper manner, the learned Single

Judge ought to have directed reconsideration of

Exts.P14 and P15 instead of condoning the delay by

himself. Therefore, while we are inclined to agree

with the learned Single Judge on the unsustainability

of Exts.P13 and P16 orders, according to us, the

proper consequential order to be passed is to direct

reconsideration of Exts.P14 and P15 with a direction

to pass fresh orders in the matter.

9.Therefore, we set aside the judgment of the learned

Single Judge to the extent the delay is condoned and

dispose of the writ appeal quashing Exts.P13 and P16

orders and directing the competent authority among

the appellants to reconsider Exts.P14 and P15 and

pass orders thereon in the light of Section 119(2)(b) (of Income Tax Act, 1961)

of the Income Tax Act. This shall be done at any

rate within 2 months from the date of receipt of a

copy of this judgment.

Writ appeal is disposed of as above.

Sd/-

ANTONY DOMINIC, Judge.

Sd/-

SHAJI P. CHALY, Judge.

×

Questions

Court Reconsiders Tax Refund Denial Due to Late Filing

Write your CommentSimilar Posts

Generic

- Reportdata/3660.pdf