Court Rejects Deferred R&D Expense Claim, Upholds Tax Assessment

Full News

Court Rejects Deferred R&D Expense Claim, Upholds Tax Assessment

Court Rejects Deferred R&D Expense Claim, Upholds Tax Assessment

The High Court dismissed an appeal by Banyan Networks Pvt. Ltd. against an Income Tax assessment order. The company had claimed deferred research and development expenses, which were disallowed by tax authorities. The court upheld the decision, stating there's no provision in the Income Tax Act for such deferred claims.

Get the full picture - access the original judgement of the court order here.

Case Name:

Banyan Networks Pvt. Ltd. vs Assistant Commissioner of Income Tax (High Court of Madras)

T.C.(A).No.318 of 2008

Key Takeaways:

1. The Income Tax Act doesn't provide for deferred research and development expenditure claims.

2. R&D expenses must be claimed in the year they are incurred, not carried forward.

3. The court emphasized strict adherence to the provisions of Section 35 (of Income Tax Act, 1961).

4. Pre-commencement R&D expenses can only be claimed as per the Explanation to Section 35 (of Income Tax Act, 1961).

Issue:

Whether the Income Tax Appellate Tribunal was correct in holding that the deferred revenue expenditure in aggregate incurred by the assessee towards product development is not allowable?

Facts:

1. Banyan Networks Pvt. Ltd. is engaged in manufacturing telecommunication products, R&D, and software development.

2. The company filed a return admitting a total loss of Rs. 5,26,38,410/- for the assessment year 2002-2003.

3. The company claimed deferred R&D expenses from previous years in the current assessment year.

4. The Assessing Officer disallowed Rs.1,92,98,564/- of the claimed expenses, allowing only Rs.34,44,649/- related to the current year.

Arguments:

Assessee's Arguments:

1. The company was developing new technology for a product known as DIAS.

2. The expenses were incurred for research and development.

3. The company decided to write off the whole expenses as the product technology became obsolete.

Revenue's Arguments:

1. There's no concept of deferred scientific research expenses in the Income Tax Act.

2. Section 35 (of Income Tax Act, 1961) doesn't allow carrying forward of R&D expenses.

3. The expenses should have been claimed in the year they were incurred.

Key Legal Precedents:

1. Section 35(1)(i) (of Income Tax Act, 1961) was cited, which deals with deductions for scientific research expenditure.

2. The court distinguished this case from Madras Industrial Investment Corporation Ltd. v. Commissioner of Income Tax, (1997) 225 ITR 802 (SC), noting that the latter dealt with discount on debentures and wasn't applicable here.

Judgement:

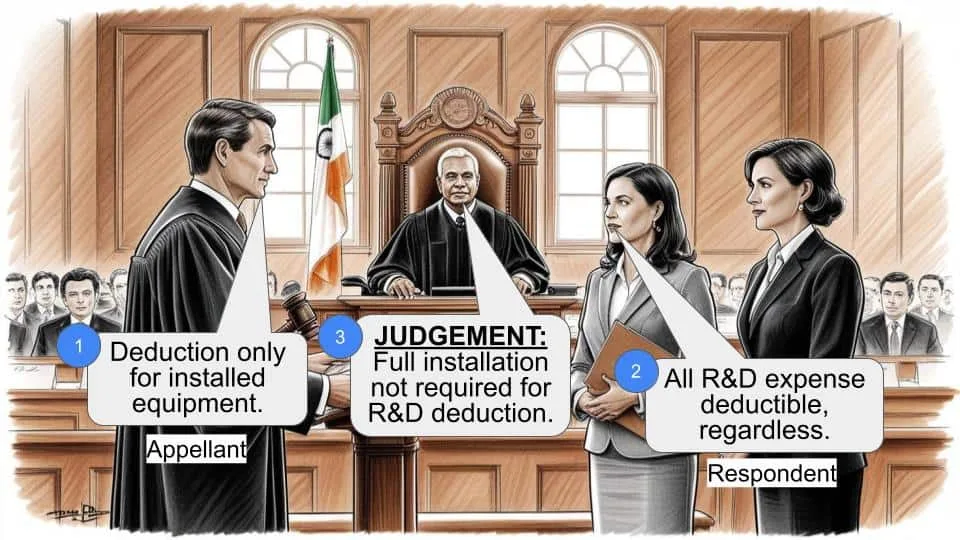

1. The High Court dismissed the appeal, upholding the decisions of the lower authorities.

2. The court found no provision in the Income Tax Act for claiming deferred research and development expenditure.

3. It agreed that the Assessing Officer was justified in allowing only the expenses related to the current assessment year.

4. The court emphasized that R&D expenses must be claimed in the year they are incurred, not carried forward.

FAQs:

Q1: Can a company claim R&D expenses from previous years in the current assessment year?

A1: No, the court ruled that R&D expenses must be claimed in the year they are incurred, not carried forward.

Q2: Does the Income Tax Act allow for deferred scientific research expenses?A2: No, the court clarified that there's no concept of deferred scientific research expenses in the Income Tax Act.

Q3: How does Section 35 (of Income Tax Act, 1961) treat R&D expenses?

A3: Section 35 (of Income Tax Act, 1961) allows deductions for scientific research expenditure, but it must be claimed in the year it's incurred, except for specific pre-commencement expenses.

Q4: What happens to R&D expenses incurred before the commencement of business?

A4: The Explanation to Section 35 (of Income Tax Act, 1961) allows certain pre-commencement R&D expenses to be claimed in the year the business starts, subject to specific conditions.

Q5: Can the decision in Madras Industrial Investment Corporation Ltd. v. Commissioner of Income Tax be applied to R&D expense cases?

A5: No, the court clarified that this decision relates to discount on debentures and doesn't apply to R&D expense cases.

1. The assessee has filed this appeal under Section 260A (of Income Tax Act, 1961) challenging the order of the Income Tax Appellate Tribunal, 'A' Bench, Chennai, dated 23.10.2007 made in I.T.A.No.530/Mds/2006 for the assessment year 2002-2003, and the same was admitted on the following questions of law:

(i) Whether the Tribunal was right in holding that the deferred revenue expenditure in the aggregate incurred by the assessee towards the product development is not allowable?

(ii) Whether the Tribunal was right in holding that the deferred revenue expenditure claimed by the assessee is not allowable in terms of explanation to Section 35 (of Income Tax Act, 1961)?

(iii) Whether the Tribunal was right in holding that the assessee is not entitled to the deduction of the prior year's expenditure forming part of the deferred revenue expenditure even though, such a claim is allowable in law as per the decision of the Supreme Court in the case of Madras Industrial Investment Corporation Ltd. v. Commissioner of Income Tax, (1997) 225 ITR 802 (SC)?

2.1. The facts in a nutshell are as under: The appellant is a private limited company engaged in the business of manufacture of telecommunication products, research and development in telecommunication products, software development and support services. The assessee filed return of income admitting total loss of Rs.5,26,38,410/-. The return was processed under Section 143(1) (of Income Tax Act, 1961) and subsequently, the case was selected for scrutiny and notice under Section 143(2) (of Income Tax Act, 1961) was issued. In response to the said notice, the assessee's representative appeared in person and furnished various details as sought for during the course of scrutiny.

2.2. It is not in dispute that the business of the assessee commenced even prior to the financial year 1999-2000. The claim of the assessee under the head deferred research and development expenses is set out in the assessment order as follows:

1999-2000 2000-2001 2001-2002 Balance at the commencement of the year Addition during the year - 7631487 7,631,487 13,556,259 19,298,564 3,444,649 1999-2000 2000-2001 2001-2002 7,631,487 21,187,746 22,743,213 Less: Written off during the year - 1,889,182 22,743,213 Balance at the close of the year 7,631,487 19,298,564 -

2.3. In the financial year 2000-2001 (assessment year 2001-2002), only a sum of Rs.18,89,182/- was claimed as expenditure to be written off during the year, even though the total expenditure during the year was to the tune of Rs.1,35,56,259/-. The assessee carried forward the expenditure to the next financial year 2001-2002 (assessment year 2002- 2003) and claimed expenditure to the tune of Rs.2,27,43,213/-, of which only a sum of Rs.34,44,649/- was allowed by the Assessing Officer, while completing the assessment under Section 143(3) (of Income Tax Act, 1961) by an order dated 25.2.2005. The Assessing Officer disallowed the claim of expenditure relating to Rs.1,92,98,564/- stating that there is no provision for carrying forward such expenditure. In brief, the finding of the Assessing Officer is as follows:

“It will be seen from the above details that the assessee has incurred expenses of Rs.76,31,487/- in the financial year 1999-2000. Rs.1,35,56,259/- in the financial year 2000-01 and Rs.34,44,649/- in the financial year 2001-02. In the lengthy submissions made by the assessee the assessee has only stated as to how the product was developed and what is its utility and the market potentiality. However there is no explanation as to why the expenses were written off in one year and as to why the research and development expenses which fall under the purview of Section 35 (of Income Tax Act, 1961) have been deferred. In the formal discussion it was however stated that since new technologies are being developed in their field the product technology has become obsolete and therefore it was decided to write off the whole expenses.

A careful study of the assessee's submissions and the close look at the details of expenses would reveal that none of the expenses mentioned in the list are of capital nature. The same were also stated to have been incurred on Research and development. It is also stated that company was developing a technology for its new product known as DIAS. The assessee in the background of submissions has admitted the fact that during the year the company was close on the completion of the development of their product and the necessary field trials of the product were completed. This very revelation indicate that the expenses made by the assessee were made for research and developments. They therefore very much fall under the purview of section 35 (of Income Tax Act, 1961). As per the submissions made by the assessee, the assessee has written off Rs.18,89,182/- for the financial year 2000- 01 relevant to the assessment year 2001-02. The balance is treated as deferred scientific expenditure. There is no concept like deferred scientific research expenses the Income-tax Act. The Research & Development expenses as envisaged u/s.35 (of Income Tax Act, 1961) and as relevant to the assessee's case states as under:-

(1) In respect of expenditure on scientific research, the following deductions shall be allowed—

(i) any expenditure (not being in the nature of capital expenditure) laid out or expended on scientific research related to the business. Explanation.—Where any such expenditure has been laid out or expended before the commencement of the business (not being expenditure laid out or expended before the 1st day of April, 1973) on payment of any salary [as defined in Explanation 2 below sub-section (5) of section 40A (of Income Tax Act, 1961)] to an employee engaged in such scientific research or on the purchase of materials used in such scientific research, the aggregate of the expenditure so laid out or expended within the three years immediately preceding the commencement of the business shall, to the extent it is certified by the prescribed authority to have been laid out or expended on such scientific research, be deemed to have been laid out or expended in the previous year in which the business is commenced;

Here in this, the assessee's business has already commenced and therefore the explanation to section 35 (of Income Tax Act, 1961) is not applicable to the assessee. Looking to the nature of expenses the same does not include any expenditure towards acquisition of any capital asset and therefore as per the provisions of the Act if at all it was an expenditure on research and development, the same ought to have been claimed in the year in which it was actually incurred. The assessee has not done so. As the assessee company itself has admitted these expenses as expenses on research and development and there is no concept of deferred expenses u/s.35 (of Income Tax Act, 1961) only those expenses which relate to the year under consideration can be allowed to the assessee. I Accordingly restrict the assessee's only to the extent of Rs.34,44,649/-. The balance expenses of Rs.1,92,98,564/- are disallowed as not pertaining to this year and added to the assessee's total income.”

(emphasis supplied)

2.4. Calling into question the assessment order, the assessee preferred an appeal before the Commissioner of Income Tax (Appeals). The Commissioner of Income Tax (Appeals), while concurring with the finding of the Assessing Officer, dismissed the appeal holding that the expenditure incurred by the assessee on research and development falls within the purview of Section 35 (of Income Tax Act, 1961) and since the business of the assessee has already commenced, the expenditure shall be allowed only in the year in which it was incurred.

2.5. Aggrieved by the said order, the assessee appealed to the Tribunal. The Tribunal observed that since the business of the assessee had already commenced, the assessee cannot come within the purview of Explanation to Section 35 (of Income Tax Act, 1961). It was also observed that the expenses relatable to the year under consideration were duly allowed by the Assessing Officer and only the expenditure not relatable to the relevant year of assessment was disallowed. The Tribunal held that the assessee failed to produce any evidence to demonstrate that the expenditure claimed is relatable to the year under consideration. Thus, the Tribunal upheld the orders passed by the authorities below.

2.6. Assailing the said order, the assessee has preferred this appeal on the questions of law referred supra.

3. We have heard Mr.K.Magesh, learned counsel for the appellant and Mr.T.Ravi Kumar, learned Senior Standing Counsel appearing for the revenue and perused the orders passed by the Tribunal and the authorities below.

4. Before adverting to the merits of the case, it would be apposite to refer to Section 35(1)(i) (of Income Tax Act, 1961) and the Explanation thereto, which are as under:

“Section 35 (of Income Tax Act, 1961). Expenditure on Scientific Research:

(1) In respect of expenditure on scientific research, the following deductions shall be allowed--

(i) any expenditure (not being in the nature of capital expenditure) laid out or expended on scientific research related to the business; Where any such expenditure has been laid out or expended before the commencement of the business (not being expenditure laid out or expended before the 1st day of April, 1973) on payment of any salary as defined in Explanation 2 below sub-section (5) of section 40A (of Income Tax Act, 1961) to an employee engaged in such scientific research or on the purchase of materials used in such scientific research, the aggregate of the expenditure so laid out or expended within the three years immediately preceding the commencement of the business shall, to the extent it is certified by the prescribed authority to have been laid out or expended on such scientific research, be deemed to have been laid out or expended in the previous year in which the business is commenced”

(emphasis supplied)

5. With regard to the second question of law, namely, whether the Tribunal was right in holding that the deferred revenue expenditure claimed by the assessee is not allowable in terms of explanation to Section 35 (of Income Tax Act, 1961), the learned counsel for the assessee fairly states that the business of the assessee has commenced long prior to the relevant assessment year and, therefore, he is not canvassing the said question of law. In view of the fair submission made by the learned counsel for the assessee, we do not propose to answer the same in this appeal.

6. Apropos the first question of law, on a plain reading of Section 35 (of Income Tax Act, 1961), we are unable to accept the plea of the learned counsel for the assessee that deferred revenue expenditure could be allowed by way of carry forward. There is no provision under the Income Tax Act which provides for such a method of claiming deferred research and development expenditure. Moreover, the Assessing Officer has allowed the expenses relatable to the year under consideration and disallowed only the expenditure not relatable to the relevant assessment year. It is also not the case of the assessee that the expenditure is relatable to the year under consideration. Therefore, in our firm view, the authorities below were justified in disallowing such a claim made by the assessee. Accordingly, the first question of law is answered against the assessee and in favour of the Revenue.

7. As regards the third question of law, the main plank of the argument of the learned counsel for the assessee is based on the decision of the Supreme Court in Madras Industrial Investment Corporation Ltd. v. Commissioner of Income Tax, (1997) 225 ITR 802 (SC). However, we find that the said decision relates to the issue of discount on debentures and the said decision does not apply to the facts of the present case. Therefore, in our considered opinion, the third question of law does not merit consideration.

For the foregoing reasons, this appeal is dismissed. No costs.

(R.S.J.) (K.B.K.V.J.)

6.4.2015

Index : Yes

Internet : Yes

To:

1. The Assistant Registrar,

Income Tax Appellate Tribunal

Chennai Bench "A", Chennai.

2. The Commissioner of Income Tax (Appeals) - III

Chennai.

3. The Assistant Commissioner of Income Tax

Company Circle I(2), Chennai.

R.SUDHAKAR,J.

and

K.B.K.VASUKI,J.

T.C.(A).No.318 of 2008

6.4.2015

×

Similar Ripples

Questions

Court Rejects Deferred R&D Expense Claim, Upholds Tax Assessment

Write your CommentSimilar Posts

Generic

- Reportdata/3898.pdf