Court remands case due to incomplete facts, orders reassessment by Assessing Of…

Full News

Court remands case due to incomplete facts, orders reassessment by Assessing Officer

Court remands case due to incomplete facts, orders reassessment by Assessing Officer

An interesting case here. The High Court was asked to review a decision made by the Income Tax Appellate Tribunal regarding an assessee's (that's the taxpayer) claims for the assessment year 1978-79. The main issues were about some work-in-progress and forfeited tippers (those are like dump trucks). The Court decided it couldn't make a final call because there weren't enough facts on record. So, they sent the case back to the Assessing Officer to dig deeper and make a decision after getting all the facts straight.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Nechupadam Construction & Ors. (High Court of Kerala)

ITR. No. 182 of 1996

Date: 14th January 2008

Key Takeaways:

1. The Court emphasized the importance of having complete facts before making a decision in tax cases.

2. Work-in-progress and asset forfeiture can be tricky issues in tax assessments, especially when dealing with cancelled contracts.

3. The treatment of business assets and their impact on tax calculations needs careful consideration.

4. Sometimes, higher courts will send cases back to lower authorities for a more thorough fact-finding process.

Issue:

The main questions the Court had to consider were:

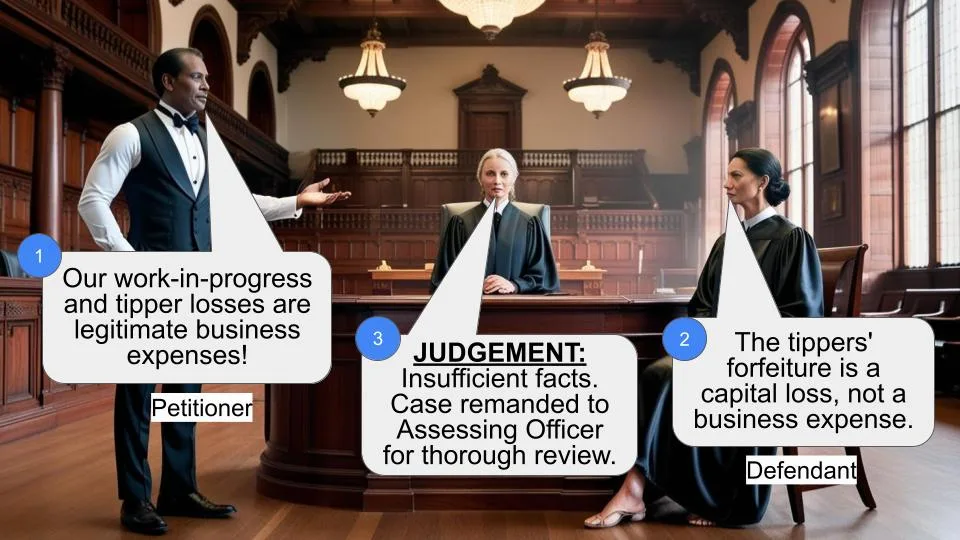

1. Was the Tribunal right in deleting an addition of Rs.68,581?

2. Was the Tribunal correct in saying that the loss related to the tippers wasn't a capital loss?

Facts:

1. On December 22, 1976, the assessee (our taxpayer) got a contract from Mysore Power Corporation to build a tunnel and do some other work.

2. The Corporation sold four tippers (think dump trucks) to the assessee for the construction work.

3. The assessee didn't do much work - only about Rs.68,581 worth.

4. Because they didn't finish the job, the contract was cancelled on December 27, 1977 - just about a year after it started.

5. The Corporation claimed liquidated damages of Rs.11 lakhs and also took back (forfeited) the four tippers.

6. When calculating the loss, the Assessing Officer reduced the work-in-progress amount and didn't allow the loss claimed for the forfeited trucks.

7. The Tribunal, however, allowed both claims.

Arguments:

The main points of contention were:

1. Whether the work-in-progress should be set off against the net loss claimed.

2. Whether the loss from the forfeited tippers should be treated as a business loss or a capital loss.

The assessee argued that both should be allowed as business losses, while the tax department contended that the tippers' forfeiture was a capital loss.

Key Legal Precedents:

Interestingly, this judgment doesn't mention any specific legal precedents. Instead, it focuses on the need for a thorough examination of facts to apply the correct tax principles.

Judgement:

The Court decided that:

1. They couldn't answer the questions definitively because there weren't enough facts on record.

2. They set aside the orders of both the Tribunal and the Commissioner of Income Tax (Appeals).

3. They sent the case back to the Assessing Officer to reconsider after verifying all the facts.

4. The Assessing Officer should also look at the assessments for subsequent years when making the decision.

FAQs:

Q1: Why didn't the Court make a final decision?

A1: The Court felt there weren't enough facts to make an informed decision. They needed more information about how the work-in-progress and tippers were treated in the assessee's accounts.

Q2: What should the Assessing Officer do now?

A2: They need to gather all the relevant facts, including details about billing, asset treatment, and how the liquidated damages were calculated.

Q3: Why is the treatment of the tippers important?

A3: How the tippers are classified (as business assets or not) affects whether their loss is considered a business loss or a capital loss, which has tax implications.

Q4: What's the significance of this judgment?

A4: It highlights the importance of thorough fact-finding in tax cases and shows that higher courts will remand cases when they feel there's insufficient information to make a proper judgment.

Q5: Does this mean the assessee won or lost?

A5: Neither, really. The case is essentially starting over, with the Assessing Officer needing to re-examine everything with more detailed information.

Heard learned counsel for the applicant and learned Standing Counsel appearing for the respondents as well. The questions which arise from the order of the Tribunal for the assessment year 1978-79 are the following:

“1. Whether on the facts and in the circumstances of the case the Tribunal is right in law and fact in deleting the addition of Rs.68,581?

2. Whether, on the facts and in the circumstances of the case the Tribunal is right in law in holding that the loss in relation to the tippers cannot be viewed as capital loss?”

The assessee was awarded a contract on 22.12.1976 by the Mysore Power Corporation for the construction of a tunnel and allied works. The awarder had sold four tippers to the assessee for use in the construction work. Admittedly, the trucks were charged. It is not known whether the assessee made payment for the trucks or whether the value remained as amount payable to the awarder to be set off against the bills raised by the assessee.

The accepted position is that the assessee carried out only very little work, valued at Rs.68,581/- and on account of the failure of the assessee to complete the work, the contract was cancelled on 27.12.1977. In fact, it is seen that the contract awarded on 22.12.1976 was cancelled within a year on account of the assessee's failure to carry out the work. It is seen from the Tribunal's order that the total liquidated damages claimed by the awarder is Rs.11 lakhs. Besides the liquidated damages claimed, the awarder forfeited the four tippers sold to the assessee for use in the construction work. The assessing officer, while granting the loss claimed, reduced the amount of work in progress and allowed the net loss which was objected by the assessee. Similarly, the loss claimed for forfeiture of the trucks was disallowed by the assessing officer, treating it as capital loss. Even though the Commissioner of Income Tax affirmed the assessment, the Tribunal allowed both the claims.

2. On going through the Tribunal's order and after hearing learned counsel appearing on both sides, we are unable to answer the questions, for the reason that full facts are not on record. In the first place, it is not known whether the assessee had billed for the work in progress and if so,following the mercantile system, it was to be set off against the net loss claimed. Moreover, if the work bill was not approved by the awarder for payment, then there is no question of reducing the value of work in progress from the loss claimed by the assessee. On the other hand, if the bill was entertained for consideration, then it was rightly reduced from the loss claimed by the assessee. So far as the value of the forfeited tippers are concerned, we do not know whether it was treated as a business asset and depreciation granted for the preceding assessment year, i.e. 1977-78. If the vehicles are treated as business assets and depreciation granted, then the department's claim that it is a business asset and hence forfeiture leads to capital loss only, is to be upheld. If it was a case of procurement of trucks for purpose of business and business never took off, then it could not be claimed as a business loss and there was no occasion to use the trucks for any business purpose. If the tippers were seized before commencement of the work and the awarder has reckoned the cost of the seized tippers while computing liquidated damages, then the question of allowing its cost as loss over and above the liquidated damages, does not arise. The Tribunal had allowed the claim on the ground that apart from claiming liquidated damages, the awarder has forfeited the tippers.

3. Since factual position is not clear from the Tribunal's order and the same will be evident only from the final claim of liquidated damages by the awarder, we set aside the order of the Tribunal and the Commissioner of Income Tax (Appeals) and remand the matter to the assessing officer for reconsidering the issue after verifying facts and with reference to the subsequent years' assessment also.

The Income Tax Reference is disposed of as above.

(C.N. Ramachandran Nair, Judge.)

(T.R. Ramachandran Nair, Judge.)

C.N. Ramachandran Nair & &

T.R. Ramachandran Nair, JJ.

×

Questions

Court remands case due to incomplete facts, orders reassessment by Assessing Officer

Write your CommentSimilar Posts

Generic

- Reportdata/5021.pdf