Court Rules on Wealth Tax: Rented Houses Not Eligible for Section 7(2) (of Inco…

Full News

Court Rules on Wealth Tax: Rented Houses Not Eligible for Section 7(2) (of Income Tax Act, 1961) Valuation

Court Rules on Wealth Tax: Rented Houses Not Eligible for Section 7(2) (of Income Tax Act, 1961) Valuation

This case involves Bennett Coleman & Co. Ltd. appealing against the Assistant Commissioner of Wealth Tax regarding the interpretation of certain provisions of the Wealth Tax Act, 1957. The main issues revolved around the applicability of specific sections to different types of employees, the classification of a flat in a tenant co-partnership society as an asset, and the valuation method for a rented residential property. The court dismissed the appeal, upholding the decisions of the lower authorities.

Get the full picture - access the original judgement of the court order here

Case Name:

Bennett Coleman & Co. Ltd. vs Assistant Commissioner of Wealth Tax & Anr. (High Court of Bombay)

Income Tax Appeal No.452 of 2001

Date: 8th January 2008

Key Takeaways:

1. The salary cap in Section 2(ea)(i)(1) (of Income Tax Act, 1961) applies to all categories of full-time employees, not just directors.

2. A flat in a tenant co-partnership society is considered an "asset" under

the Wealth Tax Act.

3. Section 7(2) of the Wealth Tax Act is not applicable to houses that are rented out.

Issue:

The main issues were:

1. Does the salary cap in Section 2(ea)(i)(1) (of Income Tax Act, 1961) apply only to directors or to all employees?

2. Is a flat in a tenant co-partnership society considered an "asset" under the Wealth Tax Act?

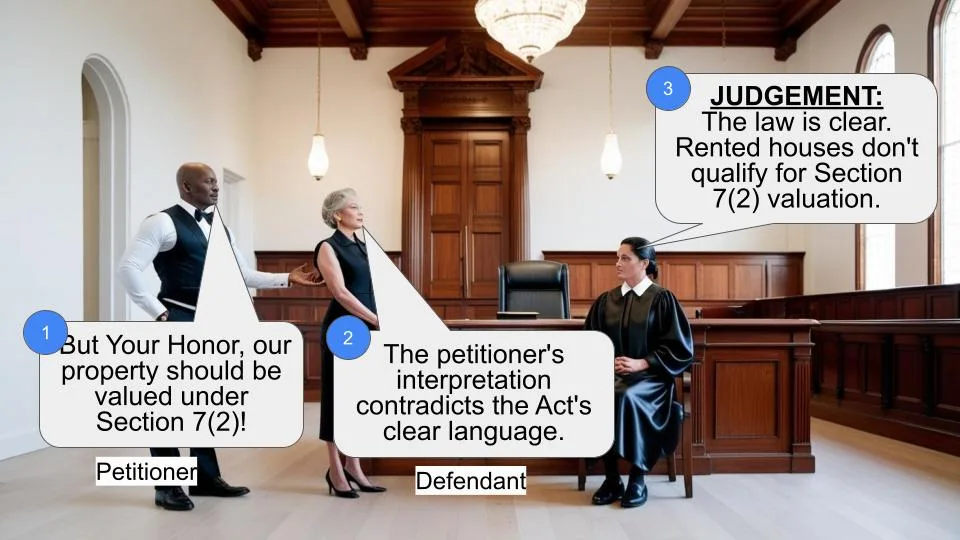

3. Can Section 7(2) of the Wealth Tax Act be applied to a house that is rented out?

Facts:

Bennett Coleman & Co. Ltd. appealed against the order of the Income Tax Appellate Tribunal (ITAT) dated 3.5.2001 for the assessment year 1994-95. The case involved the interpretation of various sections of the Wealth Tax Act, 1957, particularly concerning the valuation of residential properties and the definition of assets.

Arguments:

The appellant argued:

1. The salary cap in Section 2(ea)(i)(1) (of Income Tax Act, 1961) should only apply to directors in full-time employment.

2. A flat in a tenant co-partnership society should not be considered an "asset" under the Act.

3. Section 7(2) (of Income Tax Act, 1961) should be applicable even if the house is rented out.

The tax authorities contended that these interpretations were incorrect.

Key Legal Precedents:

The court distinguished this case from "Late Nawab Sir Mir Osman Ali Khan vs. CWT (1986) 57 CTR (SC) 89 : (1986) 162 ITR 888 (SC)".

In that case, there was no completed transfer, so the property was assessed in the hands of the transferor. In the present case, the assessee had been allotted the flat and was a member of the society.

Judgement:

1. The court held that the salary cap applies to all categories of full-time employees, including directors, officers, and other employees.

2. The court ruled that a flat in a tenant co-partnership society is indeed an "asset" under the Wealth Tax Act.

3. The court decided that Section 7(2) of the Wealth Tax Act is not applicable to houses that are rented out, as it requires exclusive use by the assessee for residential purposes throughout the preceding 12 months.

The appeal was dismissed.

FAQs:

Q1: What is Section 7(2) of the Wealth Tax Act?

A1: Section 7(2) (of Income Tax Act, 1961) allows for a specific valuation method for houses exclusively used by the assessee for residential purposes throughout the preceding 12 months.

Q2: Why wasn't Section 7(2) (of Income Tax Act, 1961) applicable in this case?

A2: The property in question was given on rent, so it wasn't exclusively used by the assessee for residential purposes.

Q3: Does the salary cap in Section 2(ea)(i)(1) (of Income Tax Act, 1961) apply to all employees?

A3: Yes, the court ruled that it applies to all categories of full-time employees, including directors, officers, and other employees.

Q4: Is a flat in a tenant co-partnership society considered an asset under the Wealth Tax Act?

A4: Yes, the court ruled that such a flat is considered an asset, as long as the assessee is a member of the society and has been allotted the flat.

Q5: What's the significance of this judgment?

A5: It clarifies important aspects of the Wealth Tax Act, particularly regarding the interpretation of certain sections and the classification of assets.

1.Admit on the questions of law which are reproduced hereinafter. Heard forthwith.

2.The appellant is aggrieved by the order of ITAT dated 3.5.2001 which disposed of two appeals for the Assessment years 1993.94 and 1994.95. This appeal is in respect of the assessment year 1994.95. The Tribunal confirmed the order of the Commissioner of Income Tax (Appeals).

3.The appellant has raised the following three questions.

1. Whether the words "having a gross annual salary of less than Rs.2/- lakhs" in Section-2(ea)(i)(1) (of Income Tax Act, 1961) should be confined to the subject which immediately proceeds it, i.e. to a director who is in whole time employment or would it also apply to the case of an employee or an officer?

2. Whether the fact in a tenant co-partnership society constitutes an "asset" as defined in Section 2(ea)(i)(1) (of Income Tax Act, 1961) given that the right of occupation enjoyed by the appellant by reason of being a member of the tenant co-partnership society cannot be regarded as "building or land appurtenant thereto"?

3. Whether a house belonging to the assessee and let out for residential purposes would attract section 7(2) (of Income Tax Act, 1961)?

4.We may first deal with the first question as framed. The question is purely based on the construction of Clause-1 of Sub Section-1 (of Income Tax Act, 1961) of Section 2(ea) of the Wealth Tax Act, 1957. The relevant portion reads as under:

"A house meant exclusively for residential purposes and which is allotted by a company to an employee or an officer or a director who is in whole time employment, having a gross annual salary of less than two lakhs rupees."

. It is sought to be submitted on behalf of the appellant that expression" having a gross annual salary of less than two lakhs rupees" would apply only be in respect of the director and not to an employee or officer. In our opinion, it will not be possible to so construe the provision both on literal interpretation or by other mode of interpretation. The expression employee, officer, director are used disjunctively.

There is a comma before the words having a gross annual salary of less than five lakhs. The entire object appears to be to include all persons in full time employment whether they being an employee, officer or director, who are allotted a house for residential purpose. In our opinion, the construction arrived at by the Tribunal to include all categories in service including a director who is in full time employment would be the correct interpretation, considering the provisions and the scheme of the relevant portion of the section which we have reproduced above. The first question therefore, would not arise.

5.Dealing with the second question, there is no dispute that what we are concerned with is a flat given for residence. It would make no difference that the flats are in a tenant co-partnership society as long as the asset falls within the ambit of Section 4(7) of the Wealth Tax Act. The test would be, is the assessee a member of a co-operative society and has been allotted a building or part of the building. An asset has been defined under Section-2(ea)(i) (of Income Tax Act, 1961) to include any building or land appurtenant thereto. Such building or land is also referred to as a house. The expression building has not been defined under the Act. As such, it will have to be understood in the ordinary sense in which the word is understood. A flat in the building would be "building". Mere fact that the flat in the building is in a co-partnership society would be of no consequence as long as the flat was obtained for a consideration and the person allotted the flat is a member of the society.

It is not disputed that the appellants have been allotted a flat in the building which is tenant co-partnership society. In our opinion, therefore, the flat would be building and consequently an asset. Both the Commissioner (Appeal) as well as ITAT have held accordingly. We have no reason to take a view different from the view taken by the Tribunal which has recorded that the agreement of purchase of the flat was entered into on 20.12.1981 and the permission has been granted to transfer the shares of the said premises directly in the name of the assessee. Apart from that the property was included in the balance sheet of the assessee. Reliance was sought to be placed on the judgment in the case of Nawab Sir Mir Osman Ali Khan Vs. CWT 162 ITR 888 (S.C.). In that case as there was no completed transfer, it was assessed in the hands of the transferor and not the transferee. In ordinary law mere agreement to sell would not transfer the title of the property until it is effected by registering the sale deed. Once therefore an assessee is admitted to membership and allotted a building or part of the building it is an ’asset’. The second question therefore also would not arise.

6.We may now deal with the last contention as to Whether Section 7(2) of the Wealth Tax Act,1957 is attracted. Section 7(1) (of Income Tax Act, 1961) provides for the manner of valuation of the asset. The language used in section 7(2) (of Income Tax Act, 1961) deals with the value of the house belonging to the assessee and exclusively used by him for residential purpose through out the period for 12 months immediately preceding the valuation date. It was sought to be contended by the appellant-assessee that the valuation ought to be as of 31.3.1971.

7.The learned Tribunal found that the main ingredient of Section 7(2) (of Income Tax Act, 1961) is that the house must belong to the assessee and much have been exclusively used by him for residential purposes through out the period of twelve months immediately preceding the valuation date. A finding is recorded that the assessee has given the property on rent and therefore, the provisions of Section 7(2) (of Income Tax Act, 1961) are not applicable. Section 7(2) (of Income Tax Act, 1961) reads as under:

"The value of a house belonging to the assessee and exclusively used by him for residential purposes throughout the period of twelve months immediately preceding the valuation date, may, at the option of the assessee, be taken to be the value determined in the manner laid down in Schedule III as on the valuation date next following the date on which he became the owner of the house or the valuation date relevant to the assessment year commencing on the 1st day of April, 1971, whichever valuation date is later".

A reading thereof would make it clear, that the house must be exclusively used by the assessee for residential purposes through out the period of twelve months.

. Admittedly as per the finding recorded, it was given on rent and consequently Section 7(2) of the Wealth Tax Act, 1957 would not be attracted. This question therefore, would not arise from the order.

8.There is therefore, no merit in this appeal which is accordingly dismissed.

(R.S. MOHITE, J.) (F.I. REBELLO, J.)

×

Similar Ripples

Questions

Court Rules on Wealth Tax: Rented Houses Not Eligible for Section 7(2) (of Income Tax Act, 1961) Valuation

Write your CommentSimilar Posts

Generic

- Reportdata/5039.pdf