Full News

Annual rent for wealth tax based on owner's receipts, not sublessee's payments

Annual rent for wealth tax based on owner's receipts, not sublessee's payments

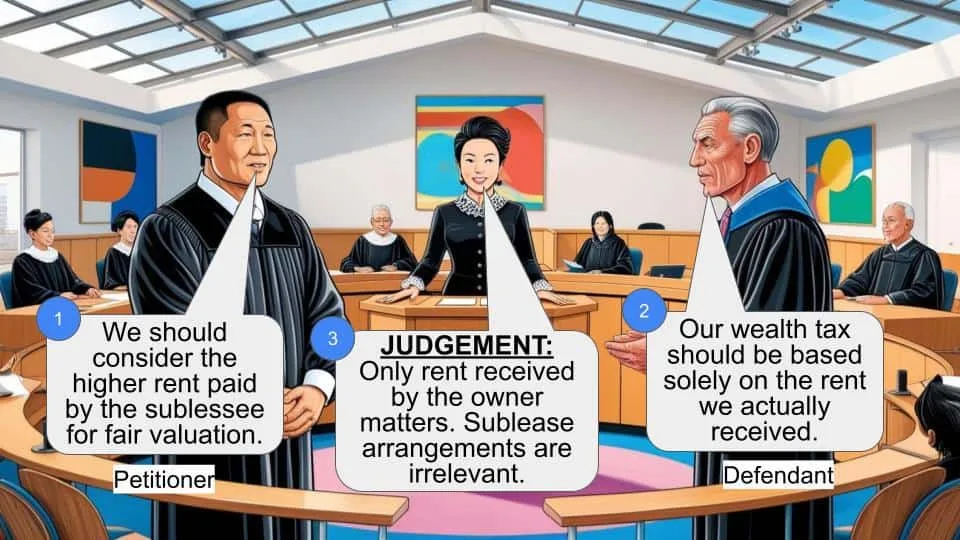

This case involves a dispute between the Commissioner of Wealth Tax and Akshya Textiles Trading & Agencies (P) Ltd. The main issue was how to determine the annual rent for wealth tax purposes when a property is subleased. The court ruled in favor of the assessee (Akshya Textiles), stating that only the rent received by the property owner should be considered, not the higher rent paid by a sublessee.

Get the full picture - access the original judgement of the court order here

Case Name:

COMMISSIONER OF WEALTH TAX VS AKSHYA TEXTILES TRADING & AGENCIES (P) LTD (High Court of Bombay)

WEALTH TAX APPEAL NO. 313 OF 2003

Date: 24th October 2007

Key Takeaways:

1. For wealth tax purposes, only the rent received or receivable by the property owner is relevant.

2. Subleasing arrangements and higher rents paid by sublessees are immaterial for wealth tax calculations.

3. The court's decision aligns the interpretation of annual rent under the Wealth Tax Act with similar provisions in the Income Tax Act.

Issue:

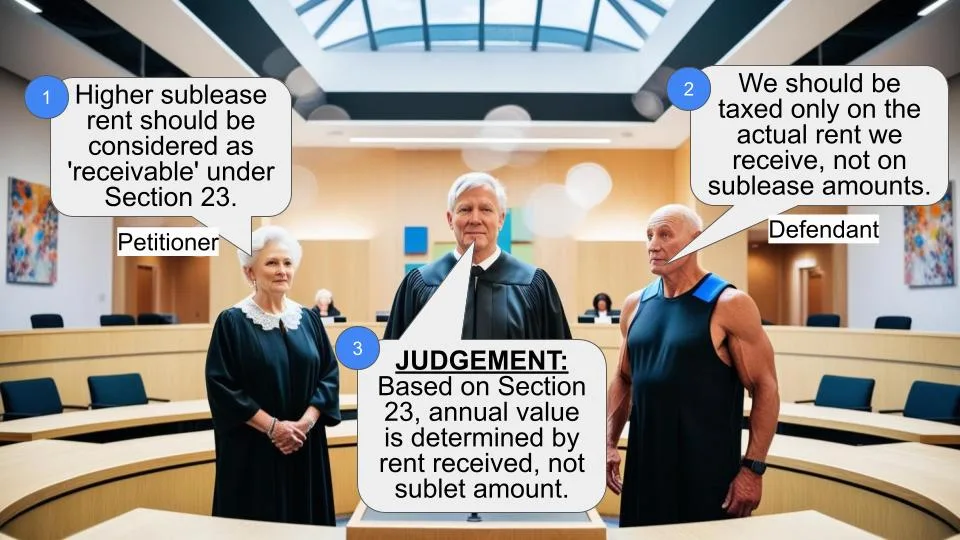

Should the rent and deposits received by an intermediary tenant from the ultimate user of the premises, rather than the rent and deposit received by the assessee from the intermediary tenant, be used for computing the net wealth of the assessee under Rule 3 (of Income Tax Rules, 1962) of Part B of Schedule III of the Wealth Tax Act, 1957?

Facts:

1. Akshya Textiles Trading & Agencies (P) Ltd. (the assessee) gave premises on license to a licensee for a certain consideration.

2. The licensee then sub-licensed the premises to Reliance Industries Ltd. for a higher consideration.

3. The Assessing Officer initially held that the transaction between the licensee and licensor was a colourable device and considered the amount paid by Reliance as the assessable value.

4. The case went through appeals, reaching the High Court for final judgment.

Arguments:

Revenue's Argument:

- The rent received from Reliance Industries Ltd. by the sub-licensee should be considered for determining the annual letting value.

Assessee's Argument:

- Only the rent actually received by the owner (Akshya Textiles) should be considered for wealth tax purposes.

Key Legal Precedents:

1. CIT vs. Akshay Textiles Trading & Agencies (P) Ltd. (2008) 214 CTR (Bom) 316: This case, dealing with similar facts under the Income Tax Act, was applied to support the current decision.

Judgement:

The court ruled in favor of the assessee, Akshya Textiles Trading & Agencies (P) Ltd. Key points of the judgment include:

1. Only the rent received or receivable by the owner is material for wealth tax purposes.

2. It's immaterial if the licensee or lessee sublets the premises for a higher consideration.

3. The colourable device between the licensee and sub-licensee, if any, is inconsequential for determining the assessee's wealth tax.

4. The court found no infirmity or error in the findings recorded by the Tribunal.

The court based its decision on the interpretation of various sections of the Wealth Tax Act, including Section 3(2) (of Income Tax Act, 1961), Section 2(m) (of Income Tax Act, 1961), Section 2(ea) (of Income Tax Act, 1961), Section 7(1) (of Income Tax Act, 1961), and Rules 3, 4, and 5 of Schedule III.

FAQs:

Q1: What does "annual rent" mean in the context of this case?

A1: According to the Explanation to Rule 5 (of Income Tax Rules, 1962), "annual rent" means the actual rent received or receivable by the owner for the year ending on the valuation date, when the property is let throughout that year.

Q2: Does this ruling apply to both rent and deposits?

A2: Yes, the court clarified that for both annual value and deposits, only the amount received by the owner should be considered.

Q3: How does this ruling affect cases where the sublessee pays a much higher rent?

A3: The higher rent paid by the sublessee is immaterial for wealth tax purposes. Only the rent received by the actual owner is considered, regardless of subleasing arrangements.

Q4: Are there any exceptions to this rule?

A4: Yes, if the rent received is less than the municipal rate of assessment or, where rent laws apply, less than the standard rent, the Revenue could potentially determine a different value for annual letting.

Q5: How does this ruling relate to Income Tax cases?

A5: The court noted that this ruling aligns with similar judgments under the Income Tax Act, as the schemes of both Acts are similar in this regard.

The Revenue has preferred this appeal on the following question :

"In the facts and circumstances of the case and in law, whether the rent and deposits received by the intermediary tenant from the ultimate user of the premises of the rent and deposit received by the assessee from the intermediary tenant, who never occupied the premises is to be taken for the computation of net wealth of the assessee for valuation under Rule 3 (of Income Tax Rules, 1962) of Part B of Schedule III of the Wealth Tax Act, 1957?"

2. For the assessment year 1998-99 the Assessing Officer noted that the Assessee had given premises on licence to the Licensee for a consideration. The licencee thereafter had sub licensed the premises to Reliance for higher consideration. The learned Assessing Officer held that the transaction between the licensee and licensor was a colourable device and therefore the amount receivable by the Assessee Company was the amount which M/s. Reliance Industries Ltd. sub licensee has paid to the Licensee. The assessee being aggrieved preferred an appeal before the Commissioner of Wealth Tax (Appeals). The Commissioner noted that in another case dated 8.9.2000, it was held that the Assessing Officer was not justified in adopting the rent paid by the ultimate user as ALV and also 15% deposit paid by the ultimate user cannot be taken into account for the purpose of working out the annual rent and gross maintainable rent and accordingly allowed the appeal. The Revenue being aggrieved preferred an appeal before the ITAT. The appeal preferred by the Respondent and Assessee along with other appeals were disposed of by a common order dated 25.09.2002. The tribunal noted the contention as urged by the Revenue that what is to be considered for the purpose of annual letting value, is the rent received from Reliance Industries Ltd. by the sub-licencee. ITAT noted that the tribunal vide its order dated 27th August, 2002 in the case of M/s. Innova Tradecom Pvt. Ltd. Vs. M/s. Chikki Fertilizers Trading & Agencies Pvt. Ltd. has decided the issue in favour of the assesses and dismissed the appeal of the revenue. Therefore, following the aforesaid decision of the tribunal the ITAT also decided all the appeals in favour of the assessee and against the revenue.

3. The issue of annual letting value in so far as proceeding under the Income Tax Act, on similar facts, where the assessee had given premises on licence by accepting consideration and the license giving the premises on sub licence to Reliance for higher consideration, has been considered by us in the case of the Commissioner of Income Tax Versus M/s. Akshay Textiles Trading & Agencies Pvt. Ltd. in Income Tax Appeal No. 607 of 2005 decided on 17th October, 2007. in that case, we had proceeded on the footing that the order of the Commissioner (Appeals) setting aside the order of the Assessing Officer as being colourable device had not been challenged before the ITAT and as such could not have been raised before the tribunal and consequently before this court. Apart from that on merits we had also considered the provisions of Section 23(1) (of Income Tax Act, 1961) and had arrived at the conclusion that what has to be considered is the annual value received by the owner, irrespective whether the licensee or lessee on subleting the premises had received higher consideration or rent. In our opinion, considering that judgment under the I.T. Act, the question as raised here though this is a case under the Wealth Tax Act, really would not arise, considering that the scheme of the two Acts are similar.

4. Apart from that we may independently consider the contention based on the provisions of the Wealth Tax Act. Section 3(2) (of Income Tax Act, 1961) reads as under :

"Subject to the other provisions contained in this Act, there shall be charged for every assessment year commencing, on and from the 1st day of April 1993, wealth-tax, in respect of the net wealth on the corresponding valuation date of every individual, Hindu undivided family and company, at the rate of one per cent. of the amount by which the net wealth exceeds fifteen lakh rupees."

"Net wealth" as defined under Section 2(m) (of Income Tax Act, 1961) reads as under:

"net wealth" means the amount by which the aggregate value computed in accordance with the provisions of this Act of all he assets, wherever located, belonging to the assessee on the valuation date, including assets required to be included in his net wealth as on that date under this Act, is in excess of the aggregate value of all the debts owned by the assessee on the valuation date which have been incurred in relation to the said assets."

. "assets" has been defined under Section 2(ea) (of Income Tax Act, 1961) and reads as under :

"assets" in relation to the assessment year commencing on the 1st day of April, 1993, or any subsequent assessment year, means - (i) any building or land appurtenant thereto (hereinafter referred to as "house"), whether used for residential or commercial purposes, or for the purpose of maintaining a guest house or otherwise including a farm house situated within twenty five kilometres from local limits of any municipality (whether known as Municipality, Municipal Corporation or by any other name) or a Cantonment Board......"

The next relevant provision is Section 7(i) (of Income Tax Act, 1961) which reads as under :

"Subject to the provisions of sub section 2 (of Income Tax Act, 1961)), the value of any asset, other than cash, for the purposes of this Act shall be its value as on the valuation date determined in the manner laid down in Schedule III."

. Schedule III contains rules for determining the value of assets. Rule (3) provides for method of valuation of immovable properties. Rule 4 (of Income Tax Rules, 1962) then sets out how the net maintainable rent for the purpose of Rule 3 (of Income Tax Rules, 1962) has to be computed. In the Explanation to Rule 5 (of Income Tax Rules, 1962), "annual rent" means where the property is let through out the year ending on the valuation date (hereinafter referred to as a"previous year"), the actual rent received or receivable by the owner in respect of such year. It would therefore, be immaterial whether the licensee or lessee to whom the owner has let out the premises, lets it out for a higher consideration. For the purpose of Wealth Tax, what is material is only the rent received or receivable by the owner, unless the rent reserved is less than the municipal rate of assessment or where the rent laws applies is less than the standard rent in which case depending on facts, revenue could determine the value of annual letting. The expression "receivable" used in the context of the rent reserved or agreed and which though agreed has not been paid but is yet receivable. Rule 5(iii) (of Income Tax Rules, 1962) sets out that where the owner has accepted any amount as deposit (not being advance payment towards rent for a period of three months or less), then how that is to be taken into consideration.

5. On a consideration of the provisions of the Act and the Rules, it would be clear that the rent/licence fee paid by M/s. Reliance Industries Ltd. or by the ultimate sub lessee to the lessee or Licensor is immaterial. What is to be considered is the amount received or receivable by the owner. Therefore, both, for the purpose of annual value as well as deposit, the relevant test is the amount received by the owner. The colourable device between the licence and the sub licensee, if any is of no consequence in so far as the assessee for determination of his wealth tax.

In so far as assessee is concerned, what only has tobe taken into account is the annual value and the deposit received by the owner in terms of the rules. We find no infirmity or error in the findings recorded by the Tribunal. We are therefore, of the opinion, that the question of law as raised is devoid of any merits and consequently the appeal is dismissed.

(J.P. DEVADHAR, J.) (F.I.REBELLO, J.)

×

Similar Ripples

Questions

Annual rent for wealth tax based on owner's receipts, not sublessee's payments

Write your CommentSimilar Posts

Generic

- Reportdata/5242.pdf