Court Upholds Depreciation on Standby Machinery, Affirms Revenue Nature of Debe…

Full News

Court Upholds Depreciation on Standby Machinery, Affirms Revenue Nature of Debenture Expenses

Court Upholds Depreciation on Standby Machinery, Affirms Revenue Nature of Debenture Expenses

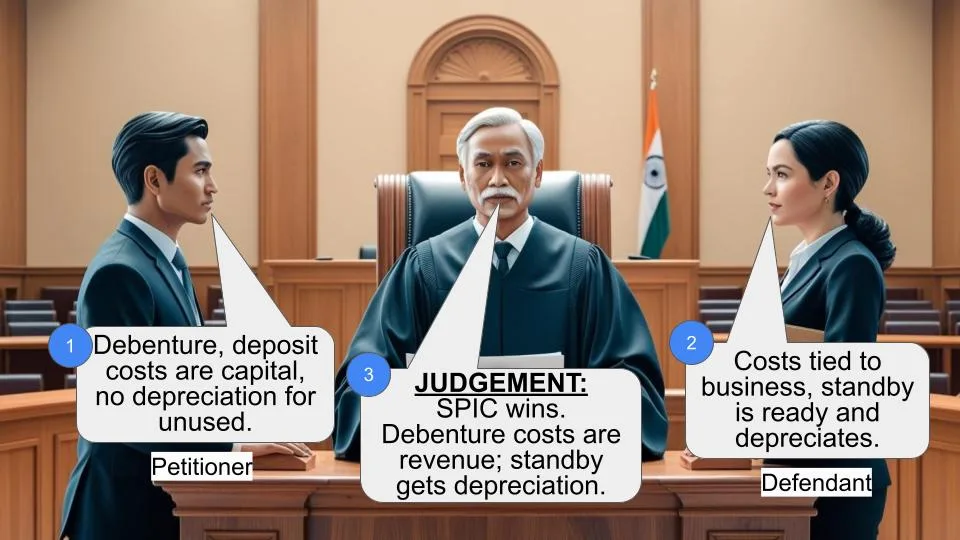

The Income Tax Department (the Revenue) appealed against Southern Petrochemical Industries Corporation Ltd. (SPIC) regarding two main issues: the classification of expenses related to debentures and fixed deposits, and the eligibility of standby machinery for depreciation. The High Court dismissed the appeal, siding with SPIC on both counts. It's a win for the company.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Southern Petrochemical Industries Corpn. Ltd. (High Court of Madras)

Tax Case (Appeal) No.42 of 2008

Date: 13th October 2008

Key Takeaways:

1. Expenses related to issuing debentures and collecting fixed deposits are considered revenue expenditure.

2. Standby machinery, even if not used during the year, is eligible for depreciation.

3. The court relied heavily on previous Supreme Court and High Court decisions to reach its conclusion.

Issue:

The main questions were:

1. Should expenses for issuing debentures and fixed deposits be treated as revenue or capital expenditure?

2. Are standby assets that weren't used during the year entitled to depreciation?

Facts:

SPIC filed their income tax return for the 2000-2001 assessment year, claiming certain deductions. The Assessing Officer wasn't having it and disallowed deductions for expenses on debenture issues, fixed deposit collection, and depreciation on standby machinery. SPIC appealed, won at the Commissioner level, and then again at the Income Tax Appellate Tribunal. Now, the Revenue has brought it to the High Court.

Arguments:

The Revenue argued that these expenses should be treated as capital expenditure and that standby machinery shouldn't get depreciation. SPIC, on the other hand, said, "Nope, these are revenue expenses, and our standby machinery deserves depreciation too!"

Key Legal Precedents:

The court relied on some heavy hitters here:

1. INDIA CEMENTS LIMITED VS. COMMISSIONER OF INCOME-TAX (1966) 60 ITR 52

2. ADDITIONAL COMMISSIONER OF INCOME-TAX VS. AKKAMAMBA TEXTILES LIMITED (1997) 227 ITR 464

3. COMMISSIONER OF INCOME TAX VS. SOUTHERN PETROCHEMICAL INDUSTRIES CORPORATION LTD. (292 ITR 362)

4. LIQLUIDATORS OF PURSA LIMITED VS. CIT (1954) 25 ITR 265

These cases established that expenses for debentures and fixed deposits are revenue in nature, and that standby machinery is eligible for depreciation.

Judgement:

The court sided with SPIC on both issues. They said, "Look, the Supreme Court has already decided that debenture expenses are revenue expenditure. As for fixed deposits, they're closely linked to the business needs. And standby machinery? As long as it's ready to use, it gets depreciation, even if it's just chilling there."

FAQs:

1. Q: Why are debenture expenses considered revenue expenditure?

A: The Supreme Court has ruled that borrowing money is part of carrying on business, and the loan isn't a long-term asset.

2. Q: Does it matter what the company uses the loan for?

A: Nope! The court said it's irrelevant to consider the object of the loan.

3. Q: Why does standby machinery get depreciation even if it's not used?

A: The court says as long as it's kept ready for use, it's eligible. They call any non-use "forced idleness".

4. Q: Could this decision affect other companies?

A: Absolutely! It sets a precedent for how similar expenses and assets should be treated for tax purposes.

5. Q: What's the main takeaway for businesses?

A: It's good news for companies with standby assets or those issuing debentures and fixed deposits. They can claim these as revenue expenses and get depreciation on standby machinery.

This appeal has been filed against the order of the Income Tax Appellate Tribunal in I.T.A.No.141/Mds/2004, dated 13.10.2006. The relevant assessment year is 2000-01.

2. The assessee-Company filed return of income for the assessment year 2000-2001 on 28.11.2000 declaring a gross total income of Rs.18,98,72,520 and after setting off an unabsorbed depreciation from the assessment year 1994-1995, arrived at a net taxable income of Rs.Nil. The assessee inter alia claimed deduction of expenditure incurred on issue of debentures and collection of fixed deposits as revenue expenditure. The Assessing Officer disallowed the same, as also the depreciation on standby machinery. Aggrieved by the assessment orders, the assessee filed appeals before the Commissioner of Income Tax (Appeals), who allowed the same based on the orders passed for the earlier years on the same issues. The Revenue took the matter on further appeal to the Income Tax Appellate Tribunal. The Income Tax Appellate Tribunal confirmed the orders of the Commissioner of Income Tax (Appeals). Hence, the present appeal has been filed by formulating the following substantial questions of law:-

" 1. Whether, in the facts and circumstances of the case, the Tribunal was right in holding that the expenditure for issue of debentures and fixed deposits is a revenue expenditure ?

2. Whether, in the facts and circumstances of the case, the Tribunal was right in holding that standby assets which are not put to use during the relevant year are entitled to depreciation ?"

3. We heard the Standing Counsel appearing for the revenue.

4. The issue as to the expenditure incurred for the debentures issued was decided as revenue expenditure by the Apex Court in the case of INDIA CEMENTS LIMITED VS. COMMISSIONER OF INCOME-TAX reported in (1966) 60 ITR 52 and ADDITIONAL COMMISSIONER OF INCOME-TAX VS. AKKAMAMBA TEXTILES LIMITED reported in (1997) 227 ITR 464.

5. When the issue has thus been covered by the decisions of the Supreme Court, the Tribunal is correct in confirming the order of the Commissioner, who regarded that the expenditure incurred in the debentures issued is a revenue expenditure.

6. As far as the expenses relating to obtaining fixed deposit is concerned, the issue was decided as revenue expenditure by the Division Bench of this Court in COMMISSIONER OF INCOME TAX VS. SOUTHERN PETROCHEMICAL INDUSTRIES CORPORATION LTD., reported in 292 ITR 362, wherein this Court held as follows:-

" .... For deciding the issue that the expenses relating to obtaining fixed deposits are closely linked with the business requirement of the assessee, it is apposite to have a cursory look on the decided case-laws on this point. In India Cements Ltd. v. C.I.T. (1966) 60 ITR 52 (SC), while deciding the nature of the amount spent towards stamps, registration fees, lawyer's fees, etc., for obtaining loan, the Supreme Court observed as follows (page 63):

"A loan may be intended to be used for the purchase of raw material when it is negotiated, but the company may, after raising the loan, change its mind and spend it on securing capital assets. Is the purpose at the time the loan is negotiated to be taken into consideration or the purpose for which it is actually used? the purpose for which the new loan was required was irrelevant to the consideration of the question whether the expenditure for obtaining the loan was revenue expenditure or capital expenditure.

To summarise this part of the case, we are of the opinion that: (a) the loan obtained is not an asset or advantage of an enduring nature; (b) that the expenditure was made for securing the use of money for a certain period; and (c) that it is irrelevant to consider the object with which the loan was obtained."

Observing so, the Supreme Court held that the act of borrowing money was incidental to the carrying on of business, the loan obtained was not an asset or an advantage of enduring nature, the expenditure was made for securing the use of money for a certain period and it was irrelevant to consider the object with which the loan was obtained and therefore, the amount spent was not in the nature of capital expenditure and was laid out or expended wholly and exclusively for the purpose of the assessee's business and was therefore allowable as a deduction. The Apex Court also held that obtaining capital by issue of shares is different from obtaining loan by debentures. The Bombay High Court in C.I.T. v. Mahindra Ugine and Steel Co. Ltd. ((2001) 250 ITR 696) considered the allowability of stamp duty paid on debenture issue as business expenditure and held that the expenditure is revenue in nature. In that case, attack was made by the Revenue on the strength of section 35D (of Income Tax Act, 1961) which deals with amortisation of certain preliminary expenses, and the Bombay High Court held that (page 698):

"Section 35D (of Income Tax Act, 1961) deals with amortisation of certain preliminary expenses. Under section 35D(1)(ii) (of Income Tax Act, 1961), it is laid down that after the commencement of the business any expenditure as described in section 35D(2) (of Income Tax Act, 1961), which is incurred in connection with the extension of the industrial undertaking or with regard to setting up a new industrial unit then the assessee shall be allowed a deduction at an amount equal to one-tenth of such expenditure for each of the ten successive previous years beginning with the previous year in which the business commences or the previous year in which expansion of the industrial undertaking is completed, etc. In the present case, on the facts, the Tribunal has found that the object of the debenture issue was to meet the working capital requirement of the assessee and, therefore, the expenditure was considered to be a revenue expenditure."

In C.I.T. v. Investment Trust of India Ltd. ((2003) 264 ITR 506)) this Court held that the expenditure on advertisements in newspapers inviting fixed deposits from the public is allowable in the words (headnote):

"In view of the provisions contained in section 58A of the Companies Act, 1956, the assessee company had to advertise the notice calling for deposits and if there was any breach, the assessee was liable to be proceeded against under the relevant provisions of the 1956 Act. Section 37(3A) (of Income Tax Act, 1961) was introduced to curb extravagant and socially wasteful expenditure on advertisement at the cost of the exchequer. The assessee had incurred the expenditure on advertisements for collecting fixed deposits and the advertisements were statutory advertisements and therefore, the provisions of section 37(3A) (of Income Tax Act, 1961) read with section 37(3B) (of Income Tax Act, 1961) were not applicable to the said expenditure."

Considering the ratio laid down in the above said decisions, we are of the view that when the Tribunal has recorded a finding that the expenses relating to obtaining fixed deposits are closely linked with the business requirement of the assessee, such expenses are allowable expenses. We therefore hold that the Tribunal was right in holding that the expenses for obtaining fixed deposits from the public is revenue in nature. Accordingly, we answer the second question in the affirmative and against the Revenue.

7. In respect of the second question of law, whether the standby assets are eligible for depreciation, the Division Bench of this Court in the case of COMMISSIONER OF INCOME-TAX VS. SOUTHERN PETROCHEMICAL INDUSTRIES CORPORATION LIMITED reported in (2007) 292 ITR 362, after referring the judgment of the Supreme Court in the case of LIQLUIDATORS OF PURSA LIMITED VS. CIT reported in (1954) 25 ITR 265, judgments of Bombay High Court in the case of COMMISSIONER OF INCOME-TAX VS. VISWANATH BHASKAR SATHE reported in (1937) 5 ITR 621 and of this Court in the case of COMMISSIONER OF INCOME-TAX VS. VAYITHRI PLANTATIONS LIMITED reported in (1981) 128 ITR 675, has held that the machinery could be used for the purposes of of the business so long as it is kept ready for such user. Any 'forced idleness' of the machinery cannot disentitle the assesses from getting the benefit of the allowance. It was further held that even in respect of standby assets, which are kept ready for user, during the relevant assessment year are entitled to depreciation. Hence, the second question of law framed by the revenue is already decided against the Revenue.

8. For the fore-going reasons, the appeal is dismissed.

Index : Yes/No

(K.R.P., J.) (C.V., J.) Internet : Yes/No 04.02.2008

×

Similar Ripples

Questions

Court Upholds Depreciation on Standby Machinery, Affirms Revenue Nature of Debenture Expenses

Write your CommentSimilar Posts

Generic

- Reportdata/4902_.pdf