Court Upholds Settlement Commission’s Decision, Urges Timely Challenges to Inte…

Full News

Court Upholds Settlement Commission’s Decision, Urges Timely Challenges to Interim Orders

Court Upholds Settlement Commission’s Decision, Urges Timely Challenges to Interim Orders

The Income Tax Department (the Revenue) is challenging an order made by the Income Tax Settlement Commission. The Commission had allowed a taxpayer’s application for settlement to proceed, but the Revenue wasn’t happy with this decision. The High Court ultimately decided not to disturb the Commission’s order but gave some important directions for future proceedings.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax Vs Income Tax Settlement Commission (ITSC) (High Court of Bombay)

Writ Petition No. 26 of 2016

Date: 28th April 2016

Key Takeaways:

- The Settlement Commission must consider all issues of full and true income disclosure in its final order.

- The Revenue should challenge interim orders quickly to avoid jeopardizing settlement attempts.

- The court emphasized the importance of timely action in settlement cases due to the 18-month time limit.

Issue:

The main question here is: Did the Income Tax Settlement Commission err in allowing the taxpayer’s settlement application to proceed without adequately addressing the Revenue’s objections regarding full and true disclosure of income?

Facts:

- On March 27, 2015, a taxpayer (Respondent No.2) filed a settlement application for tax years 2007-08 to 2014-15.

- The Settlement Commission allowed the application to proceed on April 8, 2015.

- On May 15, 2015, the Principal Commissioner of Income Tax submitted a report objecting to the application, claiming the taxpayer hadn’t made a full and true disclosure.

- The Commission, after hearing both sides, passed an order on May 21, 2015, allowing the application to continue.

- The Revenue challenged this order in the High Court, but only filed the petition in October 2015 and didn’t actively pursue it until early 2016.

Arguments:

Revenue’s side:

- They argued that the Commission didn’t properly address their objections, especially regarding a seized document showing higher profits than declared.

- They claimed the Commission’s order was non-speaking (meaning it didn’t give proper reasons).

Taxpayer’s side:

- They insisted they made a full and true disclosure of income.

- They argued that rejecting the application at this stage would require a more detailed hearing.

- They pointed out the Revenue’s delay in challenging the order, which could lead to the settlement application becoming time-barred.

Key Legal Precedents:

The judgment doesn’t mention specific case laws, but it does refer to several sections of the Income Tax Act, 1961:

- Section 245C(1) (of Income Tax Act, 1961): Filing of settlement application

- Section 245D(1) (of Income Tax Act, 1961): Initial acceptance of application

- Section 245D(2B) (of Income Tax Act, 1961): Commissioner’s report on the application

- Section 245D(2C) (of Income Tax Act, 1961): Commission’s order on validity of application

- Section 245D(3) (of Income Tax Act, 1961): Further report by Commissioner

- Section 245D(4) (of Income Tax Act, 1961): Final order by Settlement Commission

Judgement:

The court decided not to disturb the Settlement Commission’s order. However, it directed the Commission to consider all of the Revenue’s objections (from both the 245D(2B) and 245D(3) reports) when making its final decision under Section 245D(4) (of Income Tax Act, 1961).

The court also emphasized that the Revenue should challenge interim orders quickly in the future, given the 18-month time limit for settlement applications.

FAQs:

Q: Why didn’t the court overturn the Settlement Commission’s order?

A: The court was concerned about the delay caused by the Revenue in challenging the order, which could have led to the settlement application becoming time-barred.

Q: What happens next in this case?

A: The Settlement Commission will proceed with the final hearing, considering all objections raised by the Revenue in its reports.

Q: What’s the significance of the 18-month time limit mentioned in the judgment?

A: Settlement applications must be decided within 18 months, or they automatically abate. This puts pressure on both parties and the Commission to act quickly.

Q: Does this judgment set any new legal principles?

A: While it doesn’t set new principles, it emphasizes the importance of timely challenges to interim orders in settlement cases and the need for comprehensive consideration of objections in the final order.

Q: What lesson can tax authorities learn from this case?

A: They should act quickly when challenging interim orders in settlement cases to avoid risking the entire settlement process due to time constraints.

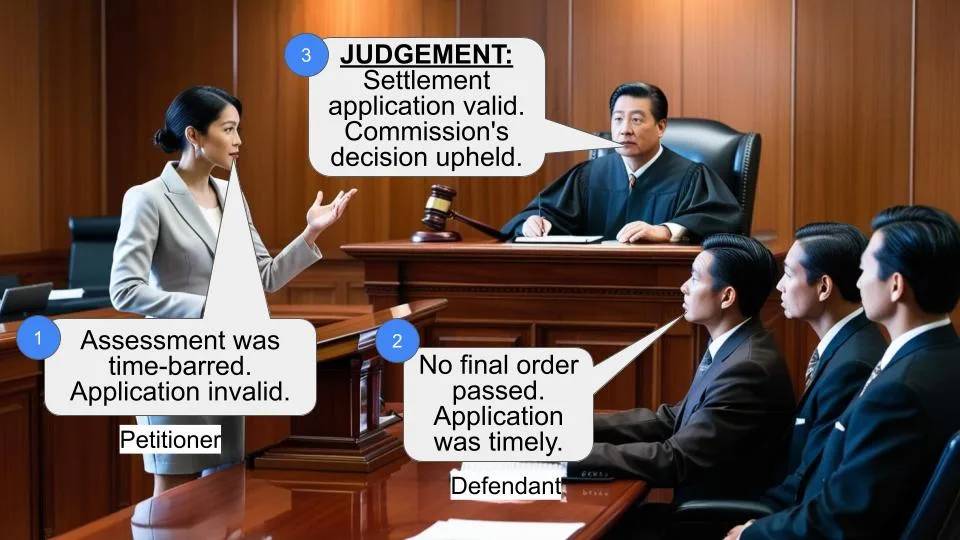

1. This petition under Article 226 of the Constitution of India challenges the order dated 21st May, 2015 passed under Section 245D(2C) (of Income Tax Act, 1961) of Chapter XIXA of the Income Tax Act, 1961 (the Act) by the Income Tax Settlement Commission (Settlement Commission). The impugned order dated 21st May, 2015 of the Settlement Commission held that the application for settlement filed by the petitioner is not invalid at the stage of Section 245D(2C) (of Income Tax Act, 1961) and is allowed to be proceeded with under Chapter XIXA of the Act.

Brief facts:

2. On 27th March, 2015 the Respondent No.2Applicant had filed an application for settlement under Section 245C(1) (of Income Tax Act, 1961) with the Settlement Commission. This with a view to settle cases for Assessment Years 200708 to 201415 which were all pending before the Assessing Officer.

3. On 8th April, 2015, the Settlement Commission passed an order under Section 245D(1) (of Income Tax Act, 1961) allowing the application for settlement filed by Respondent No.2 Applicant to be proceeded within Chapter XIX of the Act. This was after hearing the Respondent- Applicant.

4. Consequent to the above and in response to a call from the Settlement Commission, on 15th May, 2015 the Principal Commissioner of Income Tax (Commissioner) submitted his report under Section 245D(2B) (of Income Tax Act, 1961) to the Settlement Application in respect of the application for Settlement. The Commissioner in his report dated 15th May, 2015 under Section 245D(2B) (of Income Tax Act, 1961) raised various objections and sought to declare the petitioner's application for Settlement of case for Assessment Years 200708 to 201415 as invalid. This on the ground that the applicant has not made true and full disclosure of its income which had not been declared before the Assessing Officer by the RespondentApplicant for the concerned Assessment Years.

5. On 21st May, 2015, the Settlement Commission after hearing the RespondentApplicant and the Commissioner passed the impugned order under Section 245D(2C) (of Income Tax Act, 1961). The impugned order holds that the disclosure of its income made by the applicant in its application for Settlement was true and full at the stage of 245D(2C) of the Act.

Therefore, the application for settlement filed by the Respondent- Applicant No.2 is not declared invalid and allowed to be proceeded with under Chapter XIXA of the Act.

6. The PetitionerRevenue challenges the impugned order dated 21st May, 2015 by filing this petition on 12th October, 2015 in the Registry of this Court. Thereafter, the petitioners did not have the office objections removed for long. Consequently, it was only on removal of objections that the petition was allotted its regular number in January, 2016. The petition thereafter came up for hearing for the first time on 3rd February, 2016. On that date, it was adjourned at the request of the RespondentApplicant. On 10th February, 2016, the petitioner sought time to amend the petition. This application for amendment was granted. Thus, the petition was adjourned to 9th March, 2016 for the purpose of enabling the petitioner to carry out the amendment and serve the copy of the amended petition upon the RespondentApplicant. On 10th March, 2016, when the petition was on board, it was again adjourned to 13th April, 2016 as the petitioner sought time to consider the affidavitinreply filed by the RespondentApplicant. When the Petition reached hearing on 13th April, 2016, the same was adjourned at the instance of the RespondentApplicant to 27th April, 2016. The petition was heard for some time – yesterday and today.

Submissions:

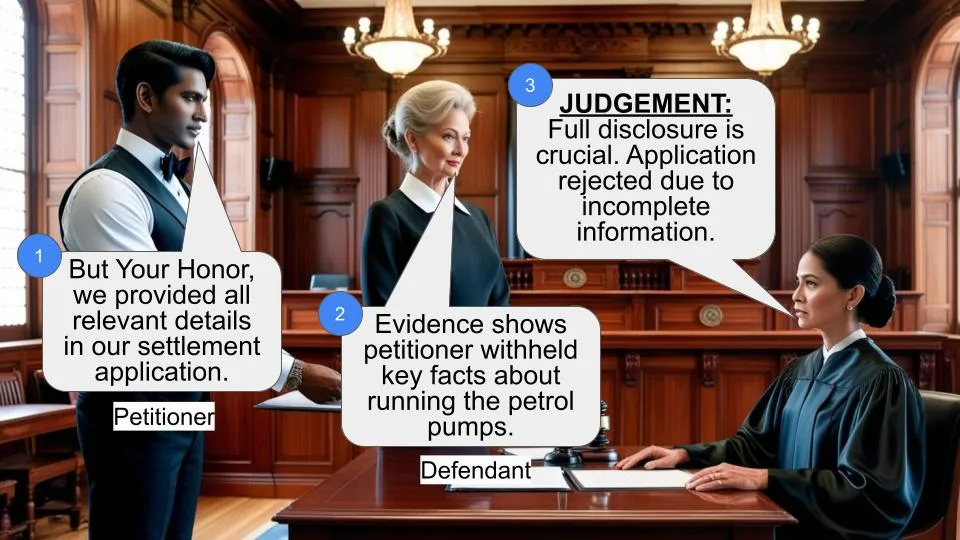

7. The grievance of the petitioner is that the issues raised by it in its report dated 15th May, 2015 under Section 245D(2B) (of Income Tax Act, 1961) were not dealt within the impugned order of the Settlement Commission dated 21st May, 2015. The principal grievance is that during the course of search, a document had been seized which according to the Revenue indicates that till 20th February, 2010, the RespondentApplicant had a profit of Rs.47.82 crores. However, as against the above, the RespondentApplicant had offered only Rs.9.61 crores as its income in its application for settlement for Assessment Years 200708 to 201415.

This according to the Petitioner was an indicator/ pointer to non- disclosure by the RespondentApplicant of its true and full income. However, the impugned order does not even record the aforesaid objection much less deal with it. Besides, it is contended that other issues raised in the objection were also not satisfactorily dealt with.

In the above view, Mr. Mohanty, learned Counsel appearing on behalf of the Petitioner submits that the impugned order is a nonspeaking order as it is passed without considering the important objection as particularized above and urged in the Commissioner's report under Section 245D(2B) (of Income Tax Act, 1961). Therefore, it is prayed that the impugned order be quashed and the issue be restored to Settlement Commission to pass a fresh order at the stage of Section 245D(2C) (of Income Tax Act, 1961).

8. As against the above, Mr. Mistri, learned Senior Counsel appearing for the RespondentRevenue points out that there has been a true and full disclosure of its income on the part of the Respondent- Applicant in its application for Settlement. In any case, the Revenue has not pointed out any failure to disclose primary facts. Rejection of an application for Settlement at the stage of Section 245D(2C) (of Income Tax Act, 1961) cannot be done on the basis of mere inferences. The rejection of an application requires a detailed hearing and consideration which would in any case happen at the stage of Section 245D(4) (of Income Tax Act, 1961).

Moreover, it is submitted that the order at stage of Section 245D(2C) (of Income Tax Act, 1961) was merely a prima facie view and the entire issue including the questions raised in the objections would still be subject to examination at stage of Section 245D(4) (of Income Tax Act, 1961). It was also urged on behalf of the respondent applicant that the application has to be disposed of by the Settlement Commission within a period of eighteen months from the date of its filing. The aforesaid period of eighteen months would expire in September, 2016. In case the eighteen months period expires, the Respondent's application would stand abated. This delay on the part of the Revenue in moving the Court challenging the impugned order appears to be deliberate. This is so as even after filing of the present Petition in October, 2015, the objections were not removed for long time and the adjournment sought without having at any time seeking an adinterim stay. Therefore, this Court should not entertain the Petition only on the ground of laches.

9. We find some merit in the submissions made on behalf of the Revenue that the impugned order dated 21st May, 2015 does not record much less deal with the contention urged by the Revenue in its report under Section 245D(2B) (of Income Tax Act, 1961). This is particularly with regard to Rs.47.82 crores being income till 2010 was indicative of the fact that there was a failure to truly and fully disclose income on the part of the RespondentApplicant. It is noteworthy that the impugned order dated 21st May, 2015 otherwise, prima facie, does record the other contentions urged in the Commissioner's report as also the context of the RespondentApplicant's response to the same. Thereafter, it appears to have taken view that the application as filed is not invalid and it should be allowed to be proceeded further. However, we must not lose sight of the fact that the Commission had while passing the impugned order dated 21st May, 2015 heard the parties i.e. the Commission and the RespondentApplicant. Therefore, if this point was urged by the Commissioner at the hearing or the Settlement Commission had pointed it to RespondentApplicant on its own reading of the Commissioner's report, it is possible that the RespondentApplicant may have had a complete answer to the satisfaction of Settlement Commission. Needless to state this consideration has to be reflected in the impugned order dated 21st May, 2015 of the Settlement Commission which is not found. However, bearing in mind that the application for Settlement would abate if the same is not decided by the Settlement Commission before September, 2016, relegating the RespondentApplicant to the adjudication proceedings under the Act it may result in RespondentApplicant's application for settlement becoming fatal. This is particularly so as the application for settlement is ready for final hearing under Section 245D(4) (of Income Tax Act, 1961) and listed on to 11th May, 2016 before the Settlement Commission.

Therefore, if on hearing the parties completely, we come to a view that the impugned order needs to be set aside and restored to the Settlement Commission, it would take up much time, resulting in abatement of the settlement application. This delay in moving the Petition is entirely due to the lackadaisical attitude of the Revenue in not moving this Petition expeditiously, challenging the interim order under Section 245D(2C) (of Income Tax Act, 1961). Almost eleven months out of the eighteen months were lost in the Petitioner not moving this Court i.e. from May, 2015 to April, 2016.

This coupled with the fact that before the Settlement Commission, the Revenue has after the impugned order proceeded with filing of its report under Section 245D(3) (of Income Tax Act, 1961). Therefore, we are not inclined to consider the challenge in this Petition in detail in view of the peculiar facts and circumstances of this case. In these facts, it would meet the interest of justice if the Settlement Commission will deal with all the issues of full and true disclosure of income in its order under Section 245D(4) (of Income Tax Act, 1961) being raised by the Revenue not only in the Commissioner's Report under Section 245D(2B) (of Income Tax Act, 1961) but also under Section 245D(3) (of Income Tax Act, 1961). This is so as it is the Revenue's case that all issues raised by them have not been adequately dealt with in the impugned order passed at the stage of Section 245D(2C) (of Income Tax Act, 1961).

10. We have not examined in detail the challenge to the impugned order, in the view we have taken on account of delay. Both sides cited decisions, which we have not dealt with, leaving it open for consideration in an appropriate case, as we are passing this order in the peculiar facts and circumstances of the case. The Revenue must bear in mind that the application for settlement has to be decided within a time period of eighteen months. Therefore, if it is aggrieved by any interim order passed by the Settlement Commission such as an order under Section 245D(2C) (of Income Tax Act, 1961), they must challenge the same as expeditiously as possible. As not moving the challenge before the Court at an early date, may render futile the assessee's attempt to adopt a mode of settling its disputes with the Income Tax Department as provided under the Act.

11. In the above view, in the peculiar facts of this case, we are not disturbing the impugned order dated 21st May, 2015 of the Settlement Commission. However, we direct the Settlement Commission to consider the petitioner's objections as recorded in the Commissioner's report under 245D(2B) of the Act at the time of passing an order under Section 245D(4) (of Income Tax Act, 1961).

12. Accordingly, Petition is disposed of in the above terms. No order as to costs.

(A.K. MENON, J.) (M.S. SANKLECHA, J.)

×

Questions

Court Upholds Settlement Commission’s Decision, Urges Timely Challenges to Interim Orders

Write your CommentSimilar Posts

Generic

- Reportdata/2876.pdf