Court Upholds Tax Addition on Unexplained Investments Despite Family Affidavits

Full News

Court Upholds Tax Addition on Unexplained Investments Despite Family Affidavits

Court Upholds Tax Addition on Unexplained Investments Despite Family Affidavits

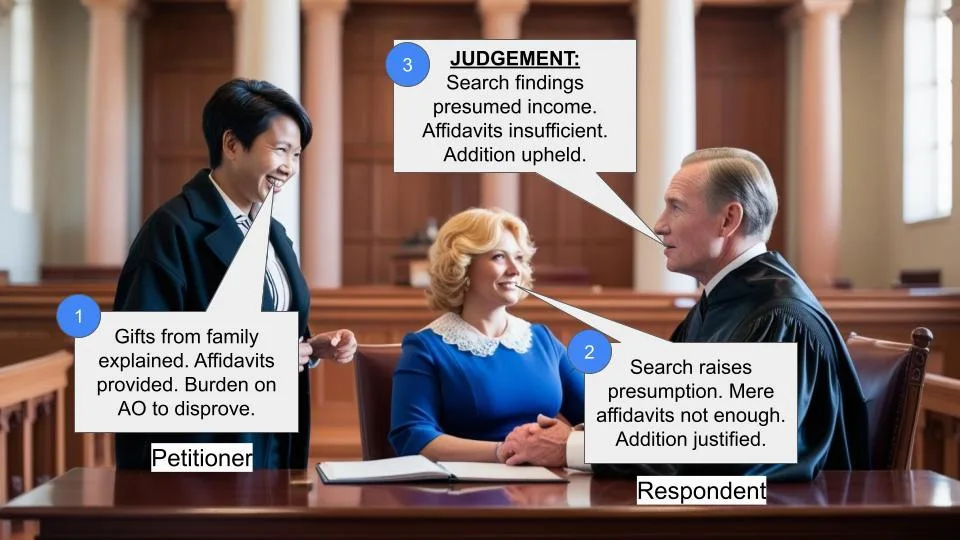

The High Court dismissed an appeal by Hemant Kumar Ghosh against an Income Tax Appellate Tribunal order. The case involved unexplained investments of Rs. 1.50 lacs and Rs. 1 lac, which the assessee claimed were gifts from his mother and wife respectively. The court upheld the tax authorities' decision to treat these amounts as undisclosed income, despite affidavits provided by the family members.

Get the full picture - access the original judgement of the court order here.

Case Name:

Hemant Kumar Ghosh Vs Assistant Commissioner of Income Tax (High Court of Patna)

Miscellaneous Appeal No.141 of 2008

Key Takeaways:

1. Investments found in an assessee's name during a search and seizure operation are presumed to be unaccounted income.

2. Affidavits from close family members may not be sufficient to explain the source of unexplained investments.

3. The burden of proof is higher on the assessee in cases arising from search and seizure operations.

4. The court emphasized the importance of satisfactory explanations for investments, especially when found during raids.

Issue:

Whether the assessee provided satisfactory explanation for the source of investments found in his name during a search and seizure operation under Section 132 (of Income Tax Act, 1961)?

Facts:

1. Hemant Kumar Ghosh, the assessee, is a proprietor of M/s. H.K. Footwear.

2. A search and seizure operation under Section 132 (of Income Tax Act, 1961) was conducted on 27.11.1996.

3. During assessment proceedings, the assessee claimed to have received gifts of Rs. 1.50 lacs from his mother and Rs. 1 lac from his wife.

4. Affidavits from the mother and wife were produced to support these claims.

5. The Assessing Officer and the Income Tax Appellate Tribunal rejected these explanations and treated the amounts as undisclosed income.

Arguments:

Assessee's Arguments:

1. The assessee relied on Section 69 (of Income Tax Act, 1961), arguing that once an explanation is offered, the burden shifts to the Assessing Officer.

2. Cited case laws, including Sarogi Credit Corporation Vs. Commissioner of Income Tax, Bihar, to support his position.

Tax Department's Arguments:

1. The burden of proof is higher in cases arising from search and seizure operations under Section 132 (of Income Tax Act, 1961).

2. Section 132(4A) (of Income Tax Act, 1961) raises a presumption that items found during a search belong to the person in whose possession they are found.

3. The assessee failed to rebut this presumption and meet the onus laid by Section 69 (of Income Tax Act, 1961).

Key Legal Precedents:

1. Sarogi Credit Corporation Vs. Commissioner of Income Tax, Bihar:

(1976) 103 ITR 344 - Established the burden of proof for explaining entries in different scenarios.

2. Commissioner of Income-Tax V. Smt. P.K. Noorjahan:

(1999) 237 ITR 570

3. Commissioner of Income-Tax V. P.V. Bhoopathy:

(2006) 283 ITR 365 (Madras)

Judgement:

1. The court dismissed the appeal, finding no substantial question of law arising from the Tribunal's order.

2. It held that when investments are found in the assessee's name during a search and seizure operation, the presumption is that they form part of unaccounted income.

3. The court deemed that mere affidavits from close family members (wife and mother) were not sufficient explanation.

4. The findings of the Assessing Officer and Tribunal were considered factual and not perverse

FAQs:

Q1: Why were the affidavits from family members not considered sufficient?

A1: The court held that in cases of search and seizure, mere affidavits from close family members are not enough to explain unexplained investments found in the assessee's name.

Q2: What is the significance of Section 132(4A) (of Income Tax Act, 1961)?

A2: This section creates a presumption that items found during a search belong to the person in whose possession they are found, placing a higher burden of proof on the assessee.

Q3: How does the burden of proof differ for entries in the assessee's name versus third parties?

A3: For entries in the assessee's name or close family members, the burden is higher to explain the nature and source. For independent third parties, the initial burden is only to establish identity and prima facie evidence of genuineness.

Q4: What lesson can taxpayers learn from this case?

A4: Taxpayers should maintain proper documentation for all significant financial transactions, especially gifts from family members, as mere affidavits may not be sufficient in case of scrutiny.

Q5: How did the court view the Tribunal's decision?

A5: The court considered the Tribunal's findings as factual and within its domain, not finding them perverse or based on no material.

Heard learned counsel for the appellant and learned counsel for the respondent-Income Tax Department.

The appeal has been filed assailing the order dated 7.9.2007 of the Income Tax Appellate Tribunal, Patna Bench, Patna by which the appeal of the assessee-appellant has been allowed in part but with regard to additions of two amounts of Rs.1.50 lacs and Rs.1 lac which the assessee claimed to have been received from his mother and wife respectively, the order of the Assessing Officer has been upheld.

The assessee is a proprietor of M/s. H.K. Footwear which deals in footwear; during the course of search and seizure under Section 132 (of Income Tax Act, 1961) held on 27.11.1996 certain facts came to light and notice under Section 158 (of Income Tax Act, 1961) BC of the Income Tax Act, 1961 was issued for filing return for the block period under consideration. Thereafter notice under Section 143(2) (of Income Tax Act, 1961) was also issued. During the course of assessment proceedings the assessee, inter alia, claimed to have received gifts of Rs. 1.50 lacs from his mother Laxmibala Ghosh and Rs. 1 lac from his wife Smt. Bandana Ghosh. The affidavits of the wife and mother were also produced in which the mother of the assessee stated that she had received the said amount of Rs. 1.50 lacs from her husband which was subsequently handed over to the assessee and similarly, the wife claimed to have received the amount of Rs. 1 lac from her father while he was on his death bed and handed over the same to the assessee. Not satisfied with the aforesaid affidavits the same were treated as undisclosed income of the assessee for the assessment years 1994-95 and 1995- 96. On appeal to the Tribunal, the appeal has been rejected so far as the said two amounts are concerned. Aggrieved by the same the appellant has come up before this Court.

Learned counsel for the appellant relies upon Section 69 (of Income Tax Act, 1961) which is in the following terms:-

“69. Unexplained investments.- Where in the financial year immediately preceding the assessment year the assessee has made investments which are not recorded in the books of account, if any, maintained by him for any source of income, and the assessee offers no explanation about the nature and source of the investments or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, the value of the investments may be deemed to be the income of the assessee of such financial year.”

It is submitted that the appellant having offered explanation about the nature and source of the investments, the burden thereafter shifted upon the Assessing Officer and that burden has not been discharged by him. In support of the aforesaid proposition, learned counsel relies upon a decision of the Division Bench of this Court in the case of Sarogi Credit Corporation Vs. Commissioner of Income Tax, Bihar: (1976) 103 ITR 344 in which it was held as follows:-

“........ In my view, the law is too well-settled, and this I say not only on account of consensus of judicial opinion, but also for the additional reason that, stretching the doctrine of onus too far, in the case of entries in favour of third parties, who themselves come forth and admit that they had advanced the loans, the addition of such amounts as from undisclosed sources or secreted profits in the assessee’s books of account, on rejection of such statements made by disinterested third parties, would lead to an absurd inconvenience, which the statute does not envisage. Decisions are numerous; to wit, a Bench decision of this Court in Radhakrishna Bihari Lal V. Commissioner of Income Tax: (1954) 26 ITR 344 (Pat.), a Bench decision of the Nagpur High Court in Jainarayan Balabakas of Khamgaon V. Commissioner of Income-tax: (1957)31 ITR 271 (Nag.), a Bench decision of the Allahabad High Court in Ram Kishan Das Munnu Lal V. Commissioner of Income-tax: (1961) 41 ITR 452 (All.) and a Bench decision of the Bombay High Court in Orient Trading Co. Ltd. V. Commissioner of Income-tax: (1963) 49 ITR 723(Bom.), may be referred to as authorities for the proposition that, if a credit entry stands in the name of the assessee himself, the burden is undoubtedly on him to prove satisfactorily the nature and source of that entry and to show that it does not constitute a part of his income liable to tax. If the credit entry stands in the names of the assessee’s wife and children, or in the name of any other near relation, or an employee of the assessee, the burden lies on the assessee, though the entry is not in his own name, to explain satisfactorily the nature and source of that entry. But, if the entry stands not in the name of any such person having a close relation or connection with the assessee, but in the name of an independent party, the burden will still lie upon him to establish the identity of that party and to satisfy the Income-tax Officer that the entry is real and not fictitious. Once the identity of the third party is established before the Income-tax Officer and other such evidence are prima facie placed before him pointing to the fact that the entry is not fictitious, the initial burden lying on the assessee can be said to have been duly discharged by him.”

Learned counsel has also relied upon decisions of the Apex Court in the case of Commissioner of Income-Tax V. Smt. P.K. Noorjahan: (1999) 237 ITR 570 and in the case of Commissioner of Income-Tax V. P.V. Bhoopathy: (2006) 283 ITR 365 (Madras).

Learned counsel for the respondent-Income Tax Department, on the other hand, submits that the burden of the appellant is much higher in the present proceeding arising out of search and seizure under Section 132 (of Income Tax Act, 1961) and sub-section (4A) thereof places heavy burden upon the assessee. The said sub-section is quoted below:

“132(4A). Where any books of account, other documents, money, bullion, jewellery or other valuable article or thing are or is found in the possession or control of any person in the course of a search, it may be presumed –

(i) that such books of account, other documents, money bullion, jewellery or other valuable article or thing belong or belongs to such person;

(ii) that the contents of such books of account and other documents are true; and

(iii) that the signature and every other part of such books of account and other documents which purport to be in the handwriting of any particular person or which may reasonably be assumed to have been signed by, or to be in the handwriting of, any particular person, are in that person’s handwriting, and in the case of a document stamped, executed or attested, that it was duly stamped and executed or attested by the person by whom it purports to have been so executed or attested.”

It is submitted that the presumption raised by Section 132(4A) (of Income Tax Act, 1961) has not at all been rebutted by the appellant and the appellant has totally failed in meeting the onus laid upon him by Section 69 (of Income Tax Act, 1961).

It is further submitted by learned counsel that in the present matter the entries were in the name of the appellant himself and no corroborating documents could be produced by the appellant to show when the mother or wife of the appellant had given the said amounts except the affidavits of such close relations. Thus, the said heavy burden which lay on the assessee as per the decision of this Court in Sarogi Credit Corporation’s case (supra) has certainly not been discharged.

From a perusal of Section 132 (of Income Tax Act, 1961) coupled with Section 69 (of Income Tax Act, 1961), it is evident that it is for the assessee to offer satisfactory explanation as to the source of income with regard to any investments found to have been made by him and if the explanation offered is not satisfactory, then it is open to the assessing officer to deem the same to be the income of the assessee for such financial year. In Sarogi Credit Corporation’s case (supra), this Court had clearly held that if an entry stands in the name of the assessee himself the burden is undoubtedly on him to prove satisfactorily the nature and source of that entry and to show that it does not constitute a part of his income liable to tax and even if the entries are in the name of the wife and childen or any near relation or an employee of the assessee, the burden would be upon the assessee to explain satisfactorily the nature and source of that entry. It is only when the entry stands in the name of a 3rd party who is an independent person and not close relation or connected with the assessee then the burden upon the assessee is only to establish identity of the said 3rd party and place such other evidence prima facie, before the Assessing Officer that the entry is not fictitious and then the initial burden upon the assessee would be treated to have been duly discharged and it would be upon the Assessing Officer to show that the investment is to be treated as an unexplained one.

In the present matter undoubtedly the investment having been found to be in the name of the assessee and assessee alone, that too in the course of search and seizure under Section 132 (of Income Tax Act, 1961), the presumption can only be that they form part of unaccounted income of the assessee and the mere fact of producing an affidavit by the wife or mother of the assessee may not be treated by the Assessing Officer as sufficient explanation and neither the Assessing Officer nor the Tribunal has found the same to establish the genuineness of the two transactions. The said findings are purely findings of fact which is in the domain of the Assessing Officer and the Tribunal and it cannot be said that the findings are either based upon no material and are perverse. This Court is of the view that such findings are the natural presumption to be drawn from the nature of evidence that the assessee had produced before the Assessing Officer.

Thus, this Court does not find that any question of law much less substantial question of law arises from the order of the Tribunal.

The appeal is, accordingly, dismissed.

S.Pandey/-

(Ramesh Kumar Datta, J)

(Anjana Mishra, J)

×

Similar Ripples

Questions

Court Upholds Tax Addition on Unexplained Investments Despite Family Affidavits

Write your CommentSimilar Posts

Generic

- Reportdata/4027.pdf