Court Upholds Tax Authority's Jurisdiction to Levy Penalty in Mining Land Resto…

Full News

Court Upholds Tax Authority's Jurisdiction to Levy Penalty in Mining Land Restoration Case

Court Upholds Tax Authority's Jurisdiction to Levy Penalty in Mining Land Restoration Case

This case involves a dispute between a taxpayer (the appellant) and the Income Tax Department (the respondent) regarding the jurisdiction of the Assessing Officer (AO) to levy a penalty. The main issue was whether the AO had the authority to impose a penalty based on an endorsement in an earlier order that was subject to appeal. The court ultimately ruled in favor of the Income Tax Department, affirming the AO's jurisdiction to levy the penalty.

Get the full picture - access the original judgement of the court order here

Case Name:

Gangadhar Narsingas Agarwal (Huf) Assistant Commissioner of Income Tax (High Court of Bombay)

Tax Appeal No. 52 of 2014

Key Takeaways:

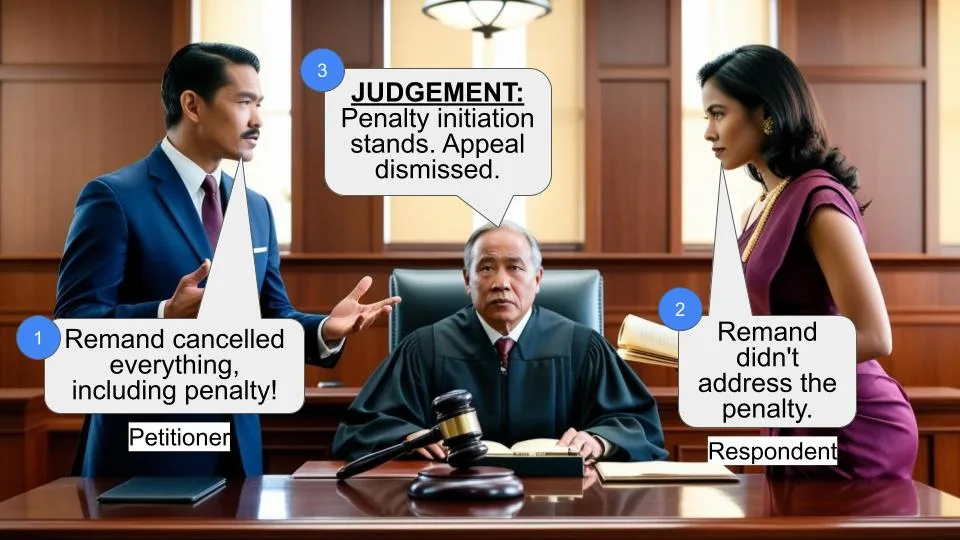

1. The substance of an order is more important than its form when interpreting its effects.

2. An appellate authority's remand order doesn't necessarily wipe out all aspects of the original order, especially if not explicitly addressed.

3. The initiation of penalty proceedings can survive a remand if the underlying assessment is ultimately maintained.

Issue:

Did the Assessing Officer have jurisdiction to impose a penalty on the appellant based on the initiation of penalty proceedings endorsed in the original assessment order, which was subsequently subject to appeal and remand?

Facts:

1. The appellant filed a tax return for the Assessment Year 1997-1998, showing a loss.

2. On 8.2.2000, the AO disallowed Rs.1,40,00,000 for mining land restoration charges and initiated penalty proceedings.

3. The appellant appealed to the Commissioner (Appeals), who remanded the matter back to the AO on 16.11.2000.

4. The AO, in a new order dated 30.3.2001, maintained the disallowance.

5. On 28.5.2001, the AO imposed a penalty of Rs.40,00,000 on the appellant.

6. The appellant appealed against both the assessment and penalty orders.

7. After multiple rounds of litigation, the case reached the High Court.

Arguments:

Appellant:

- The Commissioner (Appeals)' order dated 16.11.2000 set aside the entire original assessment order, including the penalty initiation.

- The AO should have issued a fresh notice for initiating penalty proceedings in the new assessment order.

Respondent:

- The Commissioner (Appeals)' order did not explicitly set aside the penalty initiation.

- The original endorsement for penalty proceedings remained valid as the disallowance was maintained in the new assessment order.

Key Legal Precedents:

1. Commissioner of Income-Tax Vs. Bhan Textile P. Ltd.

2. V. K. Packaging Industries Vs. Tax Recovery Officer and others

3. Commissioner of Income-Tax Vs. Basumati (P) Ltd.

4. Kunhayammed Vs. State of Kerala

These cases were cited to discuss the principles of interpreting orders and the doctrine of merger.

Judgment:

The court ruled in favor of the Income Tax Department, holding that:

1. The Commissioner (Appeals)' order dated 16.11.2000 did not set aside the entire assessment order, including the penalty initiation.

2. The AO had jurisdiction to continue with penalty proceedings based on the original endorsement.

3. A fresh notice for penalty proceedings was not necessary when the disallowance was maintained in the new assessment order.

The court dismissed the appeal and directed the parties to appear before the Commissioner (Appeals) to decide on the merits of the penalty imposition.

FAQs:

1. Q: Why didn't the court agree with the appellant's argument about the entire order being set aside?

A: The court focused on the substance of the order rather than its form, interpreting that the Commissioner (Appeals) didn't intend to interfere with the penalty initiation.

2. Q: What's the significance of the "doctrine of merger" in this case?

A: While the court acknowledged that the ITAT's observation on merger was incorrect, it didn't affect the overall decision on the AO's jurisdiction to levy the penalty.

3. Q: Does this judgment set a precedent for future cases?

A: Yes, it emphasizes the importance of interpreting orders based on their substance and context, rather than just their literal wording.

4. Q: What happens next in this case?

A: The parties are directed to appear before the Commissioner (Appeals) to decide on the merits of the Rs. 40,00,000 penalty imposed on the appellant.

5. Q: Could the outcome have been different if the Commissioner (Appeals) had explicitly mentioned setting aside the penalty initiation?

A: Possibly. The court's decision heavily relied on the interpretation that the Commissioner (Appeals) didn't intend to interfere with the penalty initiation.

Heard Mr. Ashok Kulkarni along with Ms. Vinita Palyekar, the learned Counsels for the appellant and Ms. Amira Abdul Razaq, the learned Standing Counsel for the respondent.

2. This appeal was admitted on 9.9.2014 by making a speaking Order and incorporating therein the substantial questions of law. Accordingly, for convenience of reference, we transcribe the Order dated 9.9.2014:

“Question is whether Order dated 16.11.2000 passed by CIT (Appeals) which remands the matter back to AO completely wipes out the earlier order appealed against.

2. In earlier order, the Assessee was not permitted deduction of Rs.1,40,00,000/- on account of mine refilling charges and initiated Section 271 (of Income Tax Act, 1961) proceedings. CIT (Appeals) found some fault in the exercise of jurisdiction by AO and remanded the matter back. However, in the process CIT (Appeals) did not observe anything expressly on the direction about initiating the penalty proceedings.

3. A fresh order was thereafter passed by AO without observing on need to initiate Section 271 (of Income Tax Act, 1961) proceedings therein. Perhaps on the strength of the earlier observation, the penalty proceedings have been taken up. The objection of Assessee is earlier order did not survive and in absence of any specific direction to initiate such proceedings in later assessment order, the initiation itself is barred.

4. We have heard the respective counsels.

5. Admit on the following substantial questions of law:

1. Whether on the facts and in the circumstances of the case, there was jurisdiction in the respondent to levy the impugned penalty?

2. Whether on the facts and in the circumstances of the case, the Tribunal was right in law in giving a finding that as at the relevant time, the Commissioner of Income Tax (Appeals) had the power to partially set aside an order of assessment and any finding in the order of assessment so set aside as regards satisfaction as no concealment survives after such set aside?

6. Advocate Ms. Desai waives notice for the respondent”.

3. The appellant in the present case filed a return of income disclosing a loss of Rs.13,32,280/- and net agricultural income of Rs.10,500/- for the Assessment Year 1997-1998 before the concerned Assessment Officer (AO). By Order dated 8.2.2000, made under Sec.143(3) (of Income Tax Act, 1961), 1961 (said Act), the AO, disallowed the mining land restoration charges in an amount of Rs.1,40,00,000/- and added back this amount to the return income. In the said Order dated 8.2.2000, the AO, also made the following endorsement, which was to form a part of the Order:

“Issue penalty notice u/s.271 (of Income Tax Act, 1961) (1) (c)”

4. The appellant, aggrieved by the aforesaid Order dated 8.2.2000 instituted an appeal before the Commissioner (Appeals). The Appeal Memo in this appeal is produced before us. The Appeal Memo makes no reference to the endorsement in relation to the issuance of the Notice under Section 271(1)(c) (of Income Tax Act, 1961) or to the initiation of any penalty proceedings. Order of the Commissioner of Income Tax (Appeals) dated 16.11.2000 also records that the only objection raised in the appeal was against the disallowance of Rs.1,40,00,000/- being the provision made for the expenses on restoration of land affected by mining.

5. This appeal, as noted earlier, was disposed of by the Commissioner (Appeals) vide Order dated 16.11.2000.

6. In pursuance of the aforesaid remand the (AO) made Order dated 30.3.2001 giving effect to the Order of the Commissioner (Appeals) dated 16.11.2000. This time, the AO, upon reconsideration of the matter in terms of the remand Order, once again, disallowed the amount of Rs.1,40,00,000/- for which the appellant had made a provision towards mining land restoration charges, thereby maintaining the returned income at Rs.54,49,180/-.

In this Order dated 30.3.2001, there was no specific reference to penalty or the initiation of penalty.

7. The AO, however, by a separate Order dated 28.5.2001, imposed penalty of Rs.40,00,000/- upon the appellant in exercise of powers under Section 271 of the Income Tax Act, 1961.

8. The appellant instituted an appeal before the Commissioner (Appeals) against the AO's Order giving effect to the Order of the Commissioner (Appeals) dated 30.3.2001. However, on 7.1.2002, the appellant, withdrew this appeal. Accordingly, the Order of the AO dated 30.3.2001 maintaining the appellant's income at Rs.54,49,180/- or in other words, maintaining the disallowance of Rs.1,40,00,000/-, attained finality.

9. The appellant also instituted a separate appeal before the Commissioner (Appeals) questioning the Order dated 28.5.2001 imposing penalty upon the appellant in the amount of Rs.40,00,000/-.

10. The Commissioner (Appeals) vide Order dated 8.1.2002 allowed the appellant's appeal by agreeing with the appellant's contention that the Order dated 16.11.2000 made by the Commissioner (Appeals) in the first round of litigation had completely set aside and even obliterated the Assessment Order dated 8.2.2000. The Commissioner (Appeals) reasoned that since the entire Order had been set aside, even the endorsement regards issue of penalty notice stands set aside.

11. Accordingly, the AO's Order dated 28.5.2001 levying penalty upon the appellant was set aside.

12. The respondent – Revenue appealed to the Income Tax Appellate Tribunal Panaji Bench (ITAT) against the Order dated 8.1.2002 made by the Commissioner (Appeals) setting aside the levy of penalty. This was disposed of by Order dated 7.4.2006, the operative portion of which, is contained in paragraphs 6 and 7, which reads as follows:

“6.In the light of above discussion, by considering the facts of the case, we are of the view that CIT (A) has cancelled the levy of penalty merely on technical ground without discussing the merit of the case which is not desirable. Therefore, we deem fit to set aside the order of the CIT (A) and restore the matter to him to decide the penalty appeal also on merit, but by providing reasonable opportunity to the assessee. For the similar reasons, the cross objection filed by the assessee is also allowed.

7.In the result, appeal filed by the department and cross objection filed by the assessee are allowed for statistical purposes as stated above and announced in the open court.

13. The appellant, thereupon instituted Tax Appeal No.68/2006 before this Court contending that the ITAT was obliged to first decide the issue of jurisdiction to initiate the penalty proceedings, instead of simply remanding the matter to the Commissioner (Appeals) to decide the matter on the issue of jurisdiction as well as merits.

14. Tax Appeal No.68/2006 was disposed of by this Court vide Judgment and Order dated 19.2.2018, accepting the appellants aforesaid contentions. The matter was once again remanded to ITAT to decide the issue of jurisdiction of the AO in levying penalty. The operative portion of the Judgment and Order dated 19.2.2018 is found in paragraphs no.7, 8 and 9 which read as follows:

“7.After having perused the order passed by CIT (A) and ITAT, it is obvious that the ITAT has committed error of law which is apparent on the face of record in the sense that the core issue which was challenged by the revenue was about the jurisdiction of Assessment Officer in levying penalty without issuance of penalty proceedings.

8.After the said issue had been decided in favour of the respondent herein, then, the question of remand would have arisen. We, therefore, deem it necessary again to remand the matter to the Appellate Tribunal with a direction to decide the issue of jurisdiction of Assessment Officer.

9.With this direction, the appeal is allowed and disposed of”.

15. In pursuance of the remand as aforesaid, the ITAT, has passed the impugned Judgment and Order dated 28.8.2013, in which, it has held that the AO, in the facts and circumstances of the present case, had jurisdiction to levy penalty and that the endorsement regarding initiation of Penalty proceedings contained in the AO's initial Order dated 8.2.2000 was not wiped out by the Order dated 16.11.2000 made by the Commissioner (Appeals).

16. Aggrieved by the impugned Judgment and Order dated 28.8.2013, the appellant instituted the present Tax Appeal, which, as noted earlier came to be admitted vide Order dated 9.9.2014 on the aforesaid substantial questions of law.

17. Although, this Court, has framed two substantial questions of law in its Order dated 9.9.2014, it is apparent that the issue raised by both the questions is really one and the same namely whether in the facts and circumstances of the present case, did the AO have jurisdiction to impose penalty upon the appellant based upon the initiation of the penalty proceedings as endorsed in AO's Order dated 8.2.2000, which Order was subject matter of appeal before the Commissioner (Appeals) and which appeal came to be disposed of vide Order dated 16.11.2000?

18. Mr. Kulkarni, the learned Counsel for the appellant submits that the Order dated 16.11.2000 made by the Commissioner (Appeals), upon being read in its entirety, clearly suggests that the AO's Order dated 8.2.2000 was set aside in its entirety, i.e. including the endorsement for initiation of penalty proceedings. He submits that merely because expressions like “set aside” or “quash” may not have been used by the Commissioner (Appeals), that does not mean that the AO's Order was not in fact set aside or quashed in its entirety. He submits that it is necessary to read the Order in its entirety and in the context in which it was delivered. He submits that from this it is apparent that the endorsement in the initiation of penalty proceedings was at least impliedly set aside by the Commissioner of Income-Tax (Appeals) in its Order dated 16.11.2000. He relies on Commissioner of Income-Tax Vs. Bhan Textile P. Ltd., V. K. Packaging Industries Vs. Tax Recovery Officer and others,and Commissioner of Income-Tax Vs.Basumati (P) Ltd., in support of his contentions.

19. Mr. Kulkarni, by way of elaboration submits that the Order of the AO merges in the Order of the Commissioner (Appeals) and not the other way round as held by the ITAT in the impugned Order. He also submits that the original endorsement for the initiation of the penalty proceedings was on the basis of the assessment in the Order dated 8.2.2000. Once, the assessment was set aside by the Commissioner (Appeals) though impliedly, and the matter was remanded for reconsideration, obviously, the Order of initiation of proceedings would not survive. He submits that the AO in his Order dated 30.3.2001 giving effect to the Order of the Commissioner (Appeals) has not applied his mind afresh and issued any notice for the initiation of the penalty proceedings, which is a sine qua non for sustaining any order for imposition of penalty. Mr. Kulkarni submits that these are good and weighty reasons for answering the substantial questions of law in favour of the appellant and against the revenue.

20. Ms. Razaq, the learned Standing Counsel for the respondent defends the impugned Order made by ITAT on the basis of the reasoning reflected therein. She submits that the issue raised by the appellant is hyper technical and it ignores the substance of the remand Order dated 16.11.2000. She submits that in this case, the appellant has taken part in the penalty proceedings without any demur or protest. She therefore submits that this appeal warrants dismissal.

21. Rival contentions now fall for our determination.

22. The entire appeal turns on the interpretation of the Order dated 16.11.2000 made by the Commissioner (Appeals), in the appeal against AO's Order dated 8.2.2000. The AO, as noted earlier, by his Order dated 8.2.2000 has not only disallowed the mining land restoration charges and ordered the same to be added back to the return income, but further ordered the initiation of the penalty proceedings under Sec.271(1)(c) (of Income Tax Act, 1961).

23. The appellant in his appeal against the AO's Order dated 8.2.2000 had raised no formal grounds to the initiation of penalty but had only attacked the Order, insofar as it made a disallowance of Rs.1,40,00,000/- being the provision made for expenses on restoration of land affected by mining. This is quite clear not only from the Appeal Memo handed in by the learned Counsel for the appellant but also from the Order dated 16.11.2000 made by the Commissioner (Appeals).

24. The crucial portion of the Order dated 16.11.2000 is to be found in paragraphs 7 and 8, which read as follows:

“7.The AO has assumed without any tangible basis that in the case of Gogte Minerals, the amount of pit filling expenses was actually spent. The fact is that the whole question of deductibility of expenditure, its quatum and point of time of accrual was reverted back to the assessing authority in the said case. Since the AO in the present case has not addressed the question whether the relevant mine was abandoned in this year and whether a liability otherwise arose in this year and what was the basis of quantification of liability at such a huge figure, the matter deserves to be reconsidered by him in accordance with the law in the light of the above discussion. He is directed to ascertain the year of allowability and the precise basis of quantification of provision at Rs.1,40,00,000/- in the light of the factors governing the case on the last day of the relevant accounting year when this provision was made and allow the liability only if, and to the extent, it could be said to be a real liability in praesenti crystallized on or before the last day of the relevant accounting year. For this, the AO will afford a reasonable opportunity to the appellant.

8. The appeal is disposed of accordingly. For statistical purposes, it may be treated as partly allowed”.

25. According to us, the aforesaid portion suggests that the Commissioner (Appeals) basically directed the AO to revisit the issue of disallowance but did not specifically interfere with or set aside the endorsement relating to the issuance of notice under Section 271(1) (c) (of Income Tax Act, 1961). From the tenor of the Order dated 16.11.2000, it is clear that the Commissioner (Appeals) did not wish to interfere with the endorsement at the stage of disposal of the appeal as the endorsement would undoubtedly lose its efficacy, in case, upon remand, the AO were to revoke the disallowance to the extent of Rs.1,40,00,000/- thereby reducing the returned income to that which was originally declared by the appellant at the time of filing of the initial returns for the Assessment Year 1997-1998.

26. The Order dated 16.11.2000, upon contextual reading and understanding also suggests that in case, upon remand, the AO were to maintain his original position of disallowing the amount of Rs.1,40,00,000/-, thereby maintaining the return income at Rs.54,49,180/-, then, obviously, there could be no jurisdictional bar to the continuance of the penalty proceedings, initiated by the endorsement which is to be found in the AO's Order dated 8.2.2000. If the Order dated 16.11.2000 is read and interpreted in this fashion, then, it is difficult to agree with Mr. Kulkarni's submissions or to take a view at variance with that taken by ITAT in the impugned Order dated 28.8.2013.

27. Mr. Kulkarni, is quite right in his submission, that in the absence of the words like “quash” or “set aside” do not really make any significant difference when evaluating the substance of an order as has been held in Bhan Textile P. Ltd. (supra). However, this principle will have to be extended to determining the substance of the Order dated 16.11.2000 in its entirety and not merely to the extent which benefits only appellant assessee. Therefore, applying the principle that it is the substance of the Order which is important and not the mere form, we find that the interpretation of the ITAT in the impugned Order, is the interpretation which promotes such substance over mere form and therefore there is really no case made out to interfere with the impugned Order made by the ITAT.

28. Mr. Kulkarni, quite correctly urged that the observation made by ITAT on aspect of merger is incorrect. Ms. Razaq, also did not defend such observation. In fact, it is settled by the Hon'ble Apex Court in the case of Kunhayammed Vs. State of Kerela,that it is the decree of the Trial Court which merges in that of the Appellate Court and the effect of the merger is that in the eyes of law it dies a civil death. However, based only upon the stray erroneous observation, there is no case made out to interfere with the impugned Order made by the ITAT. In fact, what the ITAT has held is that there was no merger, insofar as the endorsement for the initiation of penalty was concerned. If, upon remand, the AO were to maintain his earlier assessment, then, the endorsement was sufficient to confer jurisdiction to continue with the penalty proceedings, without the necessity of the issuance of the fresh endorsement to that effect.

29. As noted earlier, in this case the AO not only maintained the earlier income as determined in his Order dated 8.2.2000 but even the appeal instituted by the appellant against the same was withdrawn by the appellant. In such circumstances, we are unable to agree with the contentions of Mr. Kulkarni that at the stage of making order giving effect to the Order of the Commissioner (Appeals), there was necessity of making a fresh Order or there was a necessity of issuing a fresh notice for initiating the penalty proceedings. Such a contention appears to emphasise entirely on form than on substance, even, though it is the case of the appellant that it is the substance which must prevail over the form, when it comes to the interpretation of the Order dated 16.11.2000.

30. In the case of Basumati (P) Ltd. (supra) very clearly, the Appellate Court, had set aside the entire Order made by the Assessing Officer. V. K. Packaging Industries (supra) only explains the doctrine of merger, again by relying upon Kunhayammed (supra). Both these decisions, therefore, do not advance the cause of the appellant any further.

31. In view of the aforesaid discussions, we answer the substantial questions of law against the appellant in favour of the Revenue. The appeal is therefore dismissed and the parties are directed to appear before the Commissioner (Appeals) on 9th March, 2020 at 11.00 a.m., in order to enable the Commissioner (Appeals) to decide on merits whether penalty of Rs.40,00,000/- was correctly levied upon the appellant.

32. We make it clear that all contentions of the parties on the merits of the Order dated 28.5.2001, levying penalty upon the appellant are left open for determination by the Commissioner (Appeals) on their own merits and in accordance with law.

33. The appeal is accordingly disposed of in the aforesaid terms. There shall be no order as to costs.

SMT. M.S. JAWALKAR, J. M. S. SONAK, J.

×

Similar Ripples

Questions

Court Upholds Tax Authority's Jurisdiction to Levy Penalty in Mining Land Restoration Case

Write your CommentSimilar Posts

Generic

- Reportdata/6068.pdf