Court Upholds Tax Benefit for Rights Issue: Shareholders Deemed “Public” for Am…

Full News

Court Upholds Tax Benefit for Rights Issue: Shareholders Deemed “Public” for Amortization

Court Upholds Tax Benefit for Rights Issue: Shareholders Deemed “Public” for Amortization

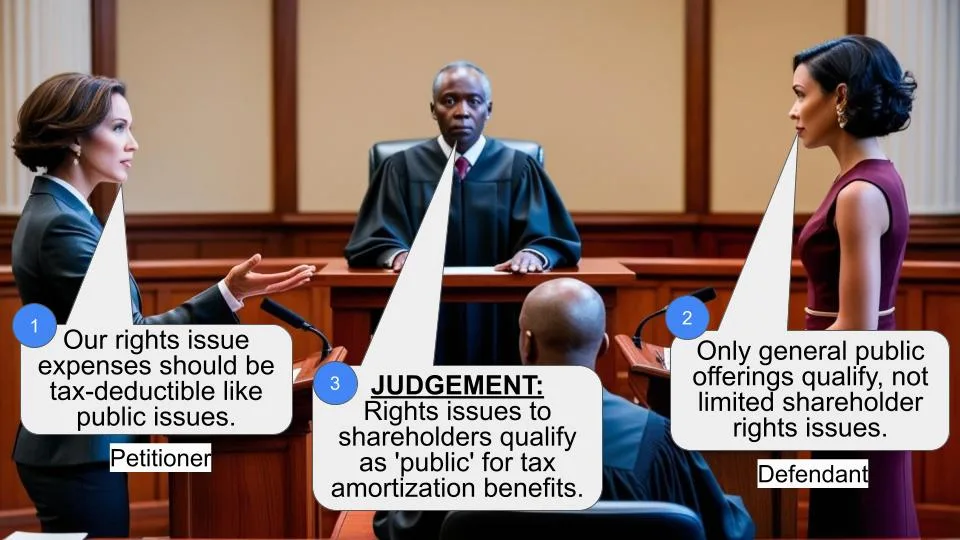

A company called Nitta Gilatine India Ltd. was fighting with the tax authorities over whether they could get a tax benefit for expenses related to issuing shares to existing shareholders. The tax folks said no, but the High Court disagreed and ruled in favor of the company. It’s a win for businesses that want to claim tax benefits on rights issues.

Get the full picture - access the original judgement of the court order here

Case Name:

Nitta Gilatine India Ltd. Vs Assistant Commissioner of Income Tax (High Court of Kerala)

ITA. No. 88 of 2009

Date: 26th August 2016

Key Takeaways:

- The court broadened the interpretation of “public subscription” in tax law to include rights issues to existing shareholders.

- This decision allows companies to claim tax benefits (amortization) on expenses related to rights issues.

- The ruling aligns the interpretation of “public” in tax law with that in company law, creating consistency across legal domains.

Issue:

The main question here was: Does the term “public subscription” in Section 35D(2) (of Income Tax Act, 1961)©(iv) of the Income Tax Act include rights issues to existing shareholders, allowing companies to claim amortization benefits on related expenses?

Facts:

- Nitta Gilatine India Ltd., a public limited company, announced a rights issue in July 1998.

- They offered shares to existing shareholders, as per Section 81 of the Companies Act.

- Many shareholders accepted, and promoters subscribed to the remaining shares.

- The company tried to claim amortization of preliminary expenses for this rights issue under Section 35D(2) (of Income Tax Act, 1961)©(iv) of the Income Tax Act.

- The tax authorities said “Nope!” arguing that only public issues qualify, not rights issues to existing shareholders.

- This dispute went through various levels of appeal before landing at the High Court.

Arguments:

The company’s side:

- Existing shareholders should be considered “public” for tax purposes.

- The rights issue qualifies as “public subscription” under Section 35D(2) (of Income Tax Act, 1961)©(iv).

- They should get the tax benefit of amortizing the expenses.

The tax authorities’ side:

- Rights issues are only to a “section of the public” (existing shareholders), not the general public.

- Section 35D(2) (of Income Tax Act, 1961)©(iv) benefits should only apply to general public issues.

- Therefore, the company shouldn’t get the amortization benefit.

Key Legal Precedents:

- The court referred to Section 67 of the Companies Act, which treats “any section of the public” as “public” for share offerings.

- They also cited the Supreme Court case “Commissioner of Income Tax, Madras v. Andhra Chamber of Commerce, Madras (AIR 1965 SC 1281)”. This case established that “general public utility” can apply to a section of the public, not necessarily the whole world.

Judgement:

The High Court ruled in favor of Nitta Gilatine India Ltd. Here’s the gist:

- They said it’s okay to look at the Companies Act to understand what “public” means in the Income Tax Act.

- Based on Section 67 of the Companies Act, existing shareholders count as a “section of the public”.

- Therefore, rights issues should qualify as “public subscription” under Section 35D(2) (of Income Tax Act, 1961)©(iv) of the Income Tax Act.

- The court felt that denying this benefit to rights issues while allowing it for public issues wouldn’t make sense.

- They allowed the company to claim amortization benefits on the expenses related to the rights issue.

FAQs:

Q: What does this mean for companies planning rights issues?

A: Good news! They can now claim tax benefits on expenses related to rights issues, potentially making these offerings more attractive.

Q: Does this apply to all types of companies?

A: The judgment specifically mentions Indian companies, so it’s most relevant to them. However, the principle might be applied more broadly.

Q: Why is this decision important?

A: It creates consistency between company law and tax law interpretations, which can lead to clearer rules for businesses.

Q: Could this decision be challenged?

A: Potentially, yes. The tax authorities could appeal to a higher court if they disagree with this interpretation.

Q: Does this mean rights issues and public issues are now treated the same for all tax purposes?

A: Not necessarily. This ruling is specific to Section 35D(2) (of Income Tax Act, 1961)©(iv) of the Income Tax Act. Other differences may still exist in other areas of tax law.

1. These appeals are filed by the assessee challenging the orders passed by the Income Tax Appellate Tribunal in I.T.A. Nos.477 of 2005 and 195 of 2007, pertaining to assessment years 1999-2000 and 2003-2004.

2. The assessee is a Public Limited Company. In terms of the provisions contained in Section 81 of the Companies Act, in July 1998, the assessee announced a rights issue of shares and accordingly shares were offered to its existing share holders. Many of them accepted the shares offered and the shares which were not accepted by the existing shareholders were subscribed by the promoters of the Company themselves. In terms of the provisions contained in Section 35D(2)(c)(iv) (of Income Tax Act, 1961), the assessee claimed amortization of the preliminary expenses incurred for the rights issue. On the ground that only shares issued for public subscription qualified for the benefit of Section 35D(2)(c)(iv) (of Income Tax Act, 1961) and that in a rights issue, shares are issued only to a section of the public, the Assessing Officer disallowed the claim. This order was confirmed by the First Appellate Authority and the Tribunal.

3. It is in this background these appeals are filed and the questions of law framed for the consideration of this Court are the following:

“1. Whether on the facts and in the circumstances of the case the Appellate Tribunal was right in holding that the expenditure incurred by the Appellant in connection with the issue of Right Shares to the public is not covered under Section 35D(2) (of Income Tax Act, 1961) (c ) (iv) of the Income Tax Act?

2. Whether there were any materials on record for the Appellate Tribunal to hold that the issue was not for public subscription especially after having accepted that share holders of the Appellant form part of the public?

3. Whether on the facts and in the circumstances of the case, having regard to the provisions of the Companies Act and other enactments the Appellate Tribunal was justified in its conclusion that the expenditure incurred in connection with the rights issue cannot be amortized and allowed as a deduction under Section 35D (of Income Tax Act, 1961)?”

4. We heard the learned Senior Counsel for the assessee and the learned Senior Counsel appearing for the Revenue.

5. The primary question that is to be answered in these appeals is whether the preliminary expenses incurred by the assessee in connection with the rights issue of shares qualified for the benefit of Section 35D(2)(c)(iv) (of Income Tax Act, 1961) .

6. Relevant part of Section 35D(2)(c)(iv) (of Income Tax Act, 1961), reads as follows:

“35D. Amortisation of certain preliminary expenses:- (1) Where an assessee, being an Indian company or a person (other than a company) who is resident in India, incurs, after the 31st day of March, 1970, any expenditure specified in sub-section (2),-

(i) before the commencement of his business, or

(ii)......

the assessee shall, in accordance with and subject to the provisions of this section, be allowed a deduction of an amount equal to one-tenth of such expenditure for each of the ten successive previous years beginning with the previous year in which the business commences or, as the case may be, the previous year in which the extension of the undertaking is completed or the new unit commences production or operation:

(2) The expenditure referred to in sub-section (1) shall be the expenditure specified in any one or more of the following clauses, namely:—

(a) expenditure in connection with-

(c) where the assessee is a company, also expenditure—

( iv) in connection with the issue, for public subscription, of shares in or debentures of the company, being underwriting commission, brokerage and charges for drafting, typing, printing and advertisement of the prospectus”

7. From a reading of this provision, it can be seen that where the assessee is an Indian Company, the expenditure incurred by it in connection with the issue of its shares for public subscription, being underwriting commission, brokerage and charges for drafting, typing, printing and advertisement of prospectus, qualify for amortization as provided in the Section. Companies incorporated in India are permitted to issue shares to its existing shareholders and such issue of shares is governed by Section 81 of the Companies Act. This Section provides that such shares shall be offered to the persons who, at the date of the offer, are holders of equity shares of the company, in proportion to the capital paid up on those shares at that date. It is also provided that after the expiry of the time specified for accepting the offer thus made by the company, if the offer is declined, the Board of Directors may dispose of the shares in such a manner as they think most beneficial to the company.

8. In compliance with Section 81 of the Companies Act, the assessee Company offered shares to its existing shareholders. Many shareholders accepted the offer and such of those shares which were declined to be accepted, were subscribed by the promoters of the Company themselves. It is because of the fact that the subscription of the shares thus issued by the Company was confined to its existing shareholders, the authorities have declined the benefit of amortization, stating that the subscribers of the shares were only a section of the public and not the public itself.

9. According to us, this interpretation adopted cannot be sustained. The term 'public' is not defined in the Income Tax Act. In such a situation and when the term is to be understood in the context of a rights issue under Section 81 of the Companies Act, to understand the scope of the term 'public' employed in Section 35D(2)(c)(iv) (of Income Tax Act, 1961) it is permissible to refer to the relevant provision of the Companies Act.

10. Section 67(1) of the Companies Act, reads thus:

“67. Construction of references to offering shares or debentures to the public, etc.—(1) Any reference in this Act or in the articles of a company to offering shares or debentures to the public shall, subject to any provision to the contrary contained in this Act and subject also to the provisions of sub-sections (3) and (4), be construed as including a reference to offering them to any section of the public, whether selected as members or debenture- holders of the company concerned or as clients of the person issuing the prospectus or in any other manner.”

11. A reading of this provision shows that any reference in the Companies Act or in the Articles of a Company offering shares to the public shall, subject to the provisions of the Companies Act, be construed as including a reference to offering the shares to any section of the public also. In other words, insofar as the Companies Act is concerned, the section of the public holding shares in a company would be treated as public, for the purposes mentioned in Section 67 (of Income Tax Act, 1961). It is also clear from Section 67 (of Income Tax Act, 1961), that the purposes of the Section would include rights issue of shares under Section 81 of the Companies Act also. Therefore, when the scope and purport of Section 35D(2)(c)(iv) (of Income Tax Act, 1961) is examined, this Court is entitled to refer to the provisions of Section 67 of the Companies Act and if so done, the inevitable conclusion is that the term for “public subscription” employed in Section 35D(2)(c)(iv) (of Income Tax Act, 1961) would include subscription by a section of the public, i.e., the existing shareholders in a Company as well. Any interpretation to the contrary would lead to a situation where the benefit of amortization would be available to public issue of shares and the same benefit would be denied when shares are issued by Companies on rights basis.

12. This conclusion that we have reached is also supported by the interpretation given to the term “general public utility” in the Apex Court judgment in Commissioner of Income Tax, Madras v. Andhra Chamber of Commerce, Madras (AIR 1965 SC 1281) where it has been held that the term general public utility does not mean that the benefit should be available to the whole world, and the benefit can be continued to a section of the public as well. This principle has been laid down in paragraph 15 of the judgment, the relevant part of which reads as follows:

“The expression "object of general public utility" however is not restricted to objects beneficial to the whole mankind. An object beneficial to a section of the public is an object of general public utility. To serve a charitable purpose, it is not necessary that the object should be to benefit the whole of mankind or even all persons living in a particular country or Province. It is sufficient if the intention to benefit a section of the public as distinguished from specified individuals. Observations to the contrary made by Baumont, C. J., in Commissioner of Income tax Bombay v. Grain Merchants' Association of Bombay, 1938 (6) ITR 427 : AIR 1939 Bom 45 that "an object of general public utility means an object of public utility which is available to the general public as distinct from any section of the public" and that objects of an association "to benefit works of public utility confined to a section of the public, i.e. those interested in commerce" are not objects of general public utility, do not correctly interpret the expression "objects of general public utility". The section of the community sought to be benefited must undoubtedly be sufficiently defined and identifiable by some common quality of a public or impersonal nature : where there is no common quality uniting the potential beneficiaries into a class, it may not be regarded as valid.”

13. Sum and substance of the above discussions that the findings of the Assessing Officer confirmed by the First Appellate Authority and the Tribunal is unsustainable.

Therefore, answering the questions of law in favour of the assessee and against the revenue, these appeals are disposed of.

Sd/-

ANTONY DOMINIC, JUDGE.

Sd/-

P.V.ASHA, JUDGE.

×