Full News

Court upholds valuation of property at acquisition cost, not rent capitalization method

Court upholds valuation of property at acquisition cost, not rent capitalization method

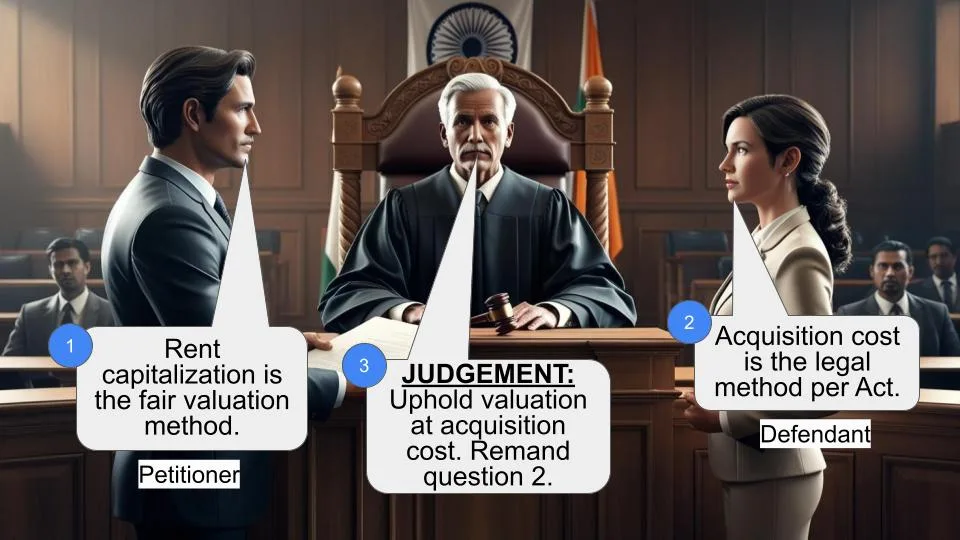

This case involves an appeal by Hindustan Construction Co. Ltd. against a decision made by the Income Tax Appellate Tribunal (ITAT) regarding the valuation of certain premises for wealth tax purposes. The main dispute centered around how the property should be valued - whether at the cost of acquisition or using the rent capitalization method. The court ultimately upheld the Tribunal's decision to value the property at the cost of acquisition.

Get the full picture - access the original judgement of the court order here

Case Name:

Hindustan Construction Co. Ltd. vs Wealth Tax Officer (High Court of Bombay)

Wealth Tax Appeal No. 923 of 2007

Date: 9th January 2008

Key Takeaways:

1. The court affirmed that employees' flats fall within the scope of Section 2(ea) of the Wealth Tax Act.

2. The property should be valued at the cost of acquisition as per the second proviso to Rule 3 (of Income Tax Rules, 1962) of Schedule III of the Wealth Tax Act.

3. The court remanded one question back to the Tribunal for reconsideration, showing the importance of addressing all grounds of appeal.

Issue

The main issue was whether the Tribunal was correct in holding that the premises should be valued at the cost of acquisition according to the second proviso to Rule 3 (of Income Tax Rules, 1962) of Schedule III of the Wealth Tax Act, rather than using the rent capitalization method as proposed by the appellant.

Facts

Let's break this down in a friendly chat:

So, here's what happened. Hindustan Construction Co. Ltd. (let's call them HCC) had some flats that were allotted to their employees. The tax folks wanted to include these flats in HCC's wealth tax assessment for the years 2002-03 and 2003-04.

HCC wasn't happy with how these flats were being valued for tax purposes. They thought the flats should be valued using something called the "rent capitalization method." But the tax tribunal (ITAT) said, "Nope, we're going to value these at the cost of acquisition."

HCC didn't like this decision, so they appealed to the High Court. They raised a few questions, but the big one was about how these flats should be valued.

Arguments

HCC's side:

1. They argued that the flats shouldn't fall under Section 2(ea) of the Wealth Tax Act.

2. They wanted the flats to be valued using the rent capitalization method.

3. They also raised some points about interest charges and exceptions in the law.

Tax department's side:

1. They said the flats do fall under Section 2(ea) of the Wealth Tax Act.

2. They argued that the correct way to value the property was using the cost of acquisition, as per the rules in the Wealth Tax Act.

Key Legal Precedents

The court mentioned a case called "Benett Colemn" when discussing Section 2(ea) of the Wealth Tax Act. They used this case to support the idea that the provision applies not just to directors, but also to employees and officers.

Judgement

Alright, so here's what the court decided:

1. They agreed with the Tribunal that the flats do fall under Section 2(ea) of the Wealth Tax Act. So, point one goes to the tax department.

2. On the big question of valuation, the court sided with the Tribunal. They said, "Yep, the Tribunal was right to value these flats at the cost of acquisition." They based this on the second proviso to Rule 3 (of Income Tax Rules, 1962) of Schedule III of the Wealth Tax Act.

3. The court didn't think questions 4 and 5 (about some technical legal points) were worth considering.

4. Interestingly, the court found that the Tribunal hadn't answered one of HCC's arguments (question 2). So, they sent that part back to the Tribunal to look at again.

In simple terms, HCC mostly lost their appeal, but they got a second chance on one point.

FAQs

1. Q: What does this decision mean for companies with employee housing?

A: It suggests that employee housing can be considered part of a company's taxable wealth, and it should be valued at the cost of acquisition for wealth tax purposes.

2. Q: Why did the court prefer the cost of acquisition method over rent capitalization?

A: The court followed the specific rule in the Wealth Tax Act (second proviso to Rule 3 (of Income Tax Rules, 1962) of Schedule III) which mandates using the cost of acquisition in certain circumstances.

3. Q: What's the significance of the court remanding one question back to the Tribunal?

A: It shows that courts take all grounds of appeal seriously. If a lower court or tribunal misses addressing a point, the higher court may send it back for reconsideration.

4. Q: Does this decision apply to all types of property?

A: This decision specifically applies to property acquired or constructed after March 31, 1974, as mentioned in the proviso to Rule 3 (of Income Tax Rules, 1962) of Schedule III of the Wealth Tax Act.

5. Q: What's the takeaway for companies dealing with wealth tax assessments?

A: Companies should be aware that employee housing can be included in wealth tax assessments, and they should be prepared to value such properties at their cost of acquisition rather than using other valuation methods.

This is an appeal against the order passed by I.T.A.T. in two Wealth Tax Appeals for the assessment year 2002-03 and 2003-04. In the present appeal, we are concerned with the assessment year 2002-03. The first question framed for the consideration reads as under :

"Whether on the facts and in the circumstances of the case and in law, the Tribunal’s was justified in holding that the flats in the impugned premises allotted to the Appellant’s employees does not fall within the four corners of the exception embedded in sub clause (1) of clause (i) of Section 2(ea) (of Income Tax Act, 1961)?"

. Considering the terminology used in sub clause (1) of Clause 2(ea) of the Wealth Tax Act in the case of Benett Colemn, we have held that the provision applies not only to Director but other categories mentioned therein and that includes employee as also officer. There is therefore, no merit in the first question which is accordingly dismissed.

. In so far as third question is concerned, the same reads as under :

"Whether on the facts and in the circumstances of the case and in law, the Tribunal was right in holding that the impugned premises ought to be valued at cost of acquisition in accordance with the second proviso to Rule 3 (of Income Tax Rules, 1962) of Schedule III to the Act vis-a-vis the rent capitalization espoused by the Appellant as mandated by main part of the said Rule 3 (of Income Tax Rules, 1962)?"

. The learned tribunal reproduced the relevant rule which is second proviso to Rule 3 (of Income Tax Rules, 1962) of Schedule III of the Wealth Tax Act and which reads as under :

"Provided further that where such property is acquired or constructed of which is completed after 31.03.74, if the value so arrived at is lower than the cost of acquisition or the cost of construction, as increased, in either case by the cost of any improvement to the property, the cost of acquisition or, as the case may be, the cost of construction, as so increased, shall be taken to be the value of the property under this rule."

. We are in agreement with the construction given by the tribunal to the said provision and consequently the said question would not arise.

. In so far as question No. 4 is concerned, the same would not be substantial question of law and consequently would not arise.

. In so far as question No. 5 is concerned, the same reads as under :

"Whether on the facts and circumstances of the Appellant’s case and in law, the Respondent was justified in exacting the Appellant with interest under Section 17B (of Income Tax Act, 1961)?"

. We find from the order of the Tribunal that this was not in issue and consequently is not required to be answered.

. That leaves us question No. 2 which reads as under :

"Whether on the facts and in the circumstances of the case and in law whether the Tribunal was correct in adjudicating ground no. 1 of the memo of appeal only partially in the sense that it failed to take cognizance of the fact the Appellant’s case is covered by exception (3) of clause (i) of Section 2(ea) (of Income Tax Act, 1961)?"

. The major contention on behalf of the appellant was that the tribunal has not answered the same.

. As question No. 2 is framed was not answered though it has been contended on behalf of the appellant that it was raised and as in the arguments filed before the Commissioner (Appeals), we find that it was raised, the ends of justice will require that in so far as this question is concerned, the impugned order is set aside and the matter is remanded back to the tribunal for reconsideration. If the tribunal holds with the appellant, the consequential relief of interest may also be considered on that aspect only. In so far as other questions are concerned, we find no merit. For the aforesaid reasons, the impugned order is set aside and the matter remanded back to the tribunal for answering de novo, question No. 2 as framed with consequential directions.

(R.S. MOHITE, J.) (F.I.REBELLO, J.)

×

Similar Ripples

Questions

Court upholds valuation of property at acquisition cost, not rent capitalization method

Write your CommentSimilar Posts

Generic

- Reportdata/5033.pdf