Hotel Under Construction Not Taxable, But Land Is After 2 Years

Full News

Hotel Under Construction Not Taxable, But Land Is After 2 Years

Hotel Under Construction Not Taxable, But Land Is After 2 Years

This case involves the Commissioner of Wealth Tax and Hotel Ornate (Nilgiri) (P) Ltd. The dispute centered around the taxation of a partly constructed hotel building and the land it stands on. The court ruled that the unfinished building is not subject to wealth tax, but the land becomes taxable after a two-year exemption period.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Wealth Tax Vs Hotel Ornate (Nilgiri) (P) Ltd. (High Court of Bombay)

Wealth Tax Appeal No.1003 of 2007

Date: 6th February 2008

Key Takeaways:

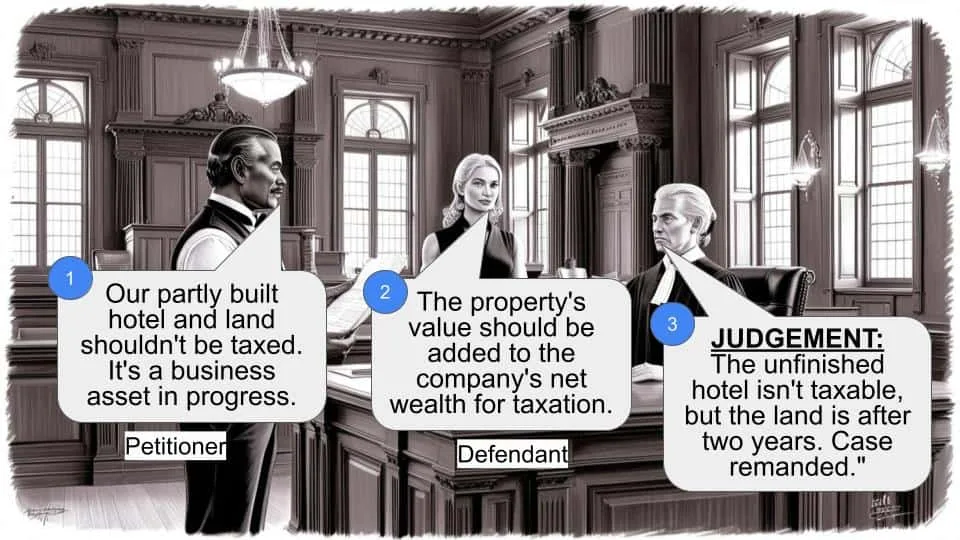

1. Partly constructed, uninhabitable buildings are not subject to wealth tax under section 40(3)(vi) of the Finance Act, 1983.

2. Land purchased for hotel construction is exempt from wealth tax for two years from the date of acquisition.

3. After the two-year exemption period, the land becomes taxable even if construction is incomplete.

Issue:

Is a partly constructed hotel building and the land it stands on assessable for wealth tax under sections 40(3)(vi) (of Income Tax Act, 1961) and 40(3)(v) of the Finance Act, 1983?

Facts:

- Hotel Ornate (Nilgiri) (P) Ltd. purchased land partly on January 5, 1984, and partly on March 4, 1984.

- The company began constructing a hotel on this land.

- The assessment years in question are 1988-89 onwards.

- At the time of assessment, the hotel building was partly constructed and not yet habitable.

Arguments:

The assessee (Hotel Ornate) argued:

- The property should fall under Section 40(3)(vi) (of Income Tax Act, 1961) and not Section 40(3)(v) (of Income Tax Act, 1961).

- The asset is a business asset and should be exempt from tax.

The Revenue (Commissioner of Wealth Tax) argued:

- The value of the under-construction property should be added to the net wealth of the assessee.

Key Legal Precedents:

The court referred to WTA-417/M/2000 and 55 I.T.D. 53, which held that work in progress could not be treated as an asset.

Judgement:

1. The partly constructed hotel building is not assessable under section 40(3)(vi) (of Income Tax Act, 1961) as it is not habitable or usable.

2. The land on which the building stands is assessable under section 40(3)(v) (of Income Tax Act, 1961) after the two-year exemption period.

3. The court set aside the Tribunal's order and remanded the matter to the Assessing Officer to determine the value of the land and pass appropriate orders.

FAQs:

Q1: Why isn't the partly constructed hotel building taxable?

A1: The building is not yet habitable or usable, so it doesn't meet the criteria for taxation under section 40(3)(vi) of the Finance Act, 1983.

Q2: Is there any tax exemption for land purchased for hotel construction?

A2: Yes, there's a two-year tax exemption period from the date of acquisition for land held for hotel construction.

Q3: What happens after the two-year exemption period?

A3: After two years, the land becomes taxable under section 40(3)(v) (of Income Tax Act, 1961), even if the hotel construction is incomplete.

Q4: What was the purpose of introducing these tax provisions?

A4: According to the Finance Minister's statement, these provisions were introduced to prevent tax avoidance by companies holding unproductive assets in closely held companies.

Q5: What's the next step in this case?

A5: The case has been remanded to the Assessing Officer, who must determine the value of the land and pass appropriate orders, including consequential orders.

1. These appeals arise from a common order passed by ITAT for the Assessment years 1988-89 to 1991-92 whereby the appeals preferred by the revenue were dismissed. In the present appeals following two questions according to revenue would arise.

(a) Whether on the facts and circumstances of the case and in law, the Hon’ble Tribunal erred in confirming the order of the CWT(A) and directing the deletion of the addition of Rs.1,56,00,000/- to the net wealth of the assessee being the value of the under construction property at ooty?

(b) Whether on the facts and circumstances of the case and in law, the Hon’ble Tribunal erred in confirming the order of the CWT(A) and deleting the addition of Rs.26,04,413/- to the net wealth of the assessee being the value of the secured debts?

Admit.

3. In so far as question (b) is concerned, we find that after making additions in the sum of Rs.26,04,413/-, the A.O. in its order of assessment dated 29.3.1995 allowed the deduction of the entire loan taken from Bank of Tokyo in the sum of Rs.97,31,871/-. Considering that, in our opinion, second question being purely academic and consequently need not be answered.

4. We may now proceed to answer the first question. The learned A.O. in its earlier order dated 31.3.1992 in Para-7 noted the contention of the assessee that the property would fall within the purview of Section-40(3)(vi) (of Income Tax Act, 1961) and not under Section 40(3)(v) (of Income Tax Act, 1961). The Commissioner (Appeals) in its finding recorded that the asset being a business asset is exempted from tax and therefore, the value of the same cannot be included in computation of new wealth. The appeal preferred by the assessee against the Commissioner (Appeals) was allowed on 14.8.1992 and the matter was remanded back to the Assessing Officer who thereafter, passed the subsequent order on 23.9.1995. The Commissioner (Appeals) thereafter passed order on 23.9.2002 (wrongly typed as 1995) and held that the asset is a business asset and is exempted from tax. Revenue aggrieved by the said order preferred an appeal before the ITAT which came to be disposed of in September 19th, 2003. The ITAT held that work in progress could not be treated as asset relying on the decision WTA-417/M/2000 and 55 I.T.D. 53. As the issues of law are common the appeals are being disposed of by a common order.

5. For the purpose of our discussion the relevant portion of Section 40 (of Income Tax Act, 1961) as introduced by the Finance Act 1983 is being reproduced.

Section-40(3) (of Income Tax Act, 1961)-The assets, referred to in sub section (2) shall be the following namely :-

(v) land other than agricultural land; Provided that nothing in this clause shall apply to any unused land held by the assessee for industrial purposes or for construction of a hotel for a period of two years from the date of its acquisition by him.

(vi) building or land appurtenant thereto, other than building or part thereof used by the assessee as factory, godown, ware house, cinema house, hotel or office for the purposes of its business or as a hospital, creche, school, canteen, library, recreational centre, shelter, rest room or lunch room mainly used for the welfare of its employees or used as residential accommodation, except as provided in clause (via) and (vib). and the land appurtenant to such building or part;

In the instant case admittedly from the facts on record the building had not become habitable or usable and consequently could not be said to be used by the assessee. Clearly therefore, as the predicate were not satisfied Section 40(3)(vi) (of Income Tax Act, 1961) would not be attracted to the facts of the case. Having said so we may now consider whether Section 40(3)(v) (of Income Tax Act, 1961) would be attracted to the facts of the present case. The statement of the Finance Minister in the Budget Speech is reported in 140 ITR (Statute) Page 32. That would show that this was done with a view to circumventing tax avoidance. The Finance Minister noted that companies are not chargeable to wealth tax, and the value of the shares of such companies does not also reflect the real worth of the assets of the company and those who hold such unproductive assets in closely held companies are able to successfully reduce their wealth tax liability to a substantial extent and in order to circumvent the tax avoidance, tax was sought to be imposed on the various assets.

6. Land ordinarily would be an asset assessable to wealth tax under Section 40(3)(v) (of Income Tax Act, 1961). The proviso however, sets out that it will not apply to any unused land held by the assessee for construction of a hotel for a period of two years from the date of the acquisition. What this would contemplate would be in the nature of tax holiday meaning thereby, that for a period of two years from the date of acquisition of the land on which the assessee seeks to construct the hotel it would be exempted from wealth tax as once the hotel is constructed it would be subject to wealth tax under Section 43(vi) (of Income Tax Act, 1961) except to the extent provided in clause (via) and (vib). A reading of the section would therefore, make it clear that the land which otherwise as assessable for tax as it would be included in net wealth for the purpose of calculating wealth tax, if it is to be put to use for industrial or hotel purpose is exempted for two years from the date of the acquisition.

In the instance case we find that the land was purchased partly on 5.1.1984 and partly on 4.3.1984. We are concerned with the assessment year 1988-89 onwards. In other words after the expiry of the period of two years.

Considering these facts we are of the opinion on the facts here that the land though on which a partly constructed building stands as the building is not usable, the land would be assessed for the purpose of wealth tax as it had to be included in net wealth.

7.The order therefore, of the Tribunal as it suffers from illegalities is consequently set aside. The matter is remanded to the Assessing Officer for determining the value of the land and thereafter to pass appropriate order including consequential orders. Appeal disposed of accordingly. We may only point out that the Commissioner (Appeals) in the order dated 14.8.1982 had directed that the reference be made to the Valuation Officer for the purpose of working out the correct value of the land which directions should be complied with. All the appeals are accordingly disposed of.

(R.S. MOHITE, J.) (F.I. REBELLO, J.)

×

Similar Ripples

Questions

Hotel Under Construction Not Taxable, But Land Is After 2 Years

Write your CommentSimilar Posts

Generic

- Reportdata/4878.pdf