No TDS Required for Property Sale Disguised as Construction Contract

Full News

No TDS Required for Property Sale Disguised as Construction Contract

No TDS Required for Property Sale Disguised as Construction Contract

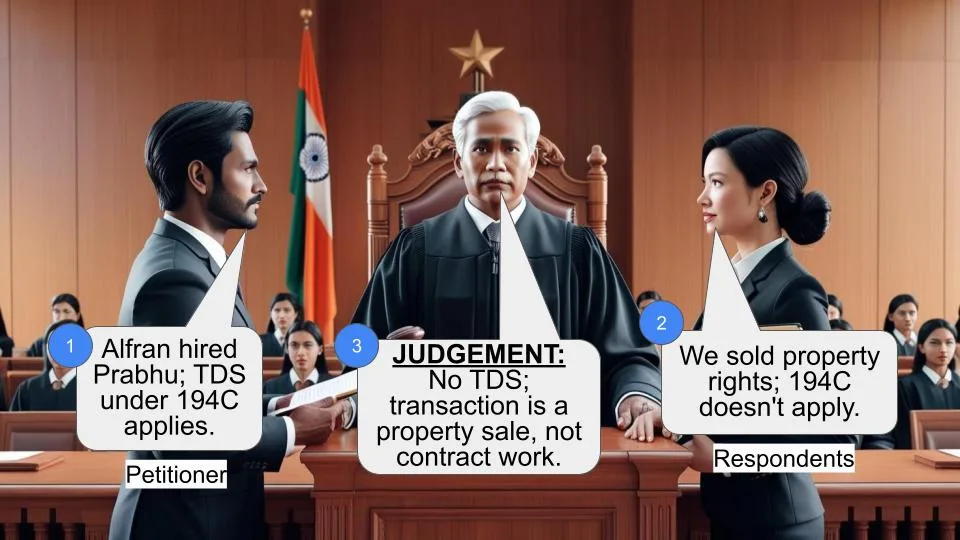

The Income Tax Department went up against Alfran Construction Pvt. Ltd. in the High Court. The big question was whether Alfran should have deducted tax at source (TDS) for a deal they made with another company. The court sided with Alfran, saying they didn't need to deduct TDS because this wasn't actually a contractor situation - it was more of a property sale deal.

Get the full picture - access the original judgement of the court order here

Case Name:

Assistant Commissioner of Income Tax Vs Alfran Construction Pvt. Ltd. (High Court of Bombay)

Tax Appeal No.13 of 2012

Date: 2nd December 2019

Key Takeaways:

1. The court emphasized that the nature of a transaction matters more than how it's labeled.

2. Section 194C (of Income Tax Act, 1961) only applies to genuine contractor relationships.

3. Courts are reluctant to interfere with factual findings of lower authorities unless there's clear perversity.

4. The interpretation of "sum" in Section 194C (of Income Tax Act, 1961) is limited to cash payments.

Issue:

The main question here was: Should Section 194C (of Income Tax Act, 1961) (which requires TDS on payments to contractors) apply to Alfran Construction's deal with Prabhu Construction?

Facts:

1. Alfran Construction had agreements with property owners to develop two projects: Mount Mary's Complex and Alfran Plaza.

2. These agreements gave Alfran rights to certain areas in these projects (5047.66 sq m and 1515.35 sq m respectively).

3. Alfran then made a deal with Prabhu Construction, transferring their rights in these projects.

4. The Income Tax Department thought this was a contractor situation and that Alfran should have deducted TDS.

5. Both the CIT(Appeals) and the Income Tax Appellate Tribunal (ITAT) disagreed with the tax department.

Arguments:

The Income Tax Department said:

- Alfran was originally a contractor for these projects.

- The deal with Prabhu Construction was just Alfran hiring another contractor.

- Therefore, Alfran should have deducted TDS under Section 194C (of Income Tax Act, 1961).

Alfran Construction's side (implied from the judgment):

- The original agreements weren't contractor agreements, but property rights deals.

- The transfer to Prabhu Construction was a sale of these rights, not a contractor arrangement.

- Therefore, Section 194C (of Income Tax Act, 1961) doesn't apply here.

Key Legal Precedents:

1. H.H. Sri Rama Verma vs. Commissioner of Income Tax, Ernakulam, 1991 Supp (1) SCC 209: This case was cited to interpret the word "sum" in Section 194C (of Income Tax Act, 1961) as meaning cash money.

Judgement:

The High Court agreed with Alfran Construction. Here's why:

1. They found no reason to disagree with the factual findings of the CIT(Appeals) and ITAT.

2. These lower authorities had concluded that this was a sale of property rights, not a contractor situation.

3. The court said that neither Alfran nor Prabhu Construction could be considered contractors in this case.

4. Therefore, Section 194C (of Income Tax Act, 1961) didn't apply.

5. The court also agreed that since 194C didn't apply, the related provision 40(a)(ia) also couldn't apply.

FAQs:

1. Q: What's the main takeaway from this case?

A: The main takeaway is that the substance of a transaction matters more than its form. Even if something looks like a contractor agreement on the surface, if it's actually a property sale, it won't be treated as a contractor relationship for tax purposes.

2. Q: Does this mean companies can avoid TDS by structuring deals as property sales?

A: Not exactly. The court looked closely at the original agreements and the rights they conferred. Companies can't just label any transaction as a property sale to avoid TDS.

3. Q: Why didn't the High Court re-examine the facts of the case?

A: High Courts generally don't interfere with factual findings of lower authorities unless there's clear perversity or misreading of evidence. In this case, they found no such issues.

4. Q: What does this case say about the interpretation of tax laws?

A: It suggests that tax laws, like Section 194C (of Income Tax Act, 1961), should be interpreted strictly based on their plain language. Courts won't expand the scope of these provisions beyond what's clearly stated.

5. Q: Could this decision be appealed further?

A: Potentially, yes. The Income Tax Department could try to appeal to the Supreme Court if they believe there's a substantial question of law involved.

1. Heard Ms. Razaq, the learned Standing Counsel for the Income Tax Department for the appellant.

2. The respondents though served, neither present nor represented.

3. This appeal was admitted on 14.02.2012 on the following substantial questions of law :

(A) Whether the Section 194 (of Income Tax Act, 1961) C could be invoked requiring the Assessee to deduct tax at source on the cost of the construction incurred by M/s Prabhu Construction deeming it as a contract?

(B) Whether consequent provision of sec 40(a)(ia) (of Income Tax Act, 1961) would also apply in making disallowing of expenditure in computing his income from business and profession?

4. Ms. Razaq, the learned Standing Counsel for the applicant submits that in the present case, the Assessee was itself the contractor who had undertaken to complete two projects i.e. Mount Mary's project and M/s. Alfraz Plaza project. The Assessee by Agreement dated 23.11.2003 had purported to assign its rights in favour of M/s Prabhu Construction, a proprietary concern of Shri Venkatesh Prabhu Moni. Ms. Razaq submits that since the Assessee could not transfer or assign any better rights or title in favour of M/s. Prabhu Construction, it is obvious that M/s. Prabhu was also a contractor engaged by the Assessee. She submits that in such circumstances, the provisions of Section 194C(ITA) (of Income Tax Act, 1961) were very clearly attracted and the Assessee was obliged to effect tax deduction at source. She submits that inasmuch as this has not been done and this particular aspect has not been appreciated, the two substantial questions of law as framed are required to be answered in favour of the Revenue and against the Assessee.

5. In this case, the Assessee vide two separate agreements dated 01.03.2003 and 13.11.1991 respectively, had agreed with the owners to undertake the projects of construction of Mount Mary's Complex and M/s. Alfran Plaza. The terms of these agreements do not indicate that the Assessee was appointed as merely a contractor to construct these projects. Rather, the Assessee was to be allotted premises/area in the said project admeasuring 5047.66 square metres and 1515.35 square metres.

The Assessee was given the full liberty to thereafter sell, transfer and convey these areas in favour of third party. Accordingly, it is not correct to say that the original status of the Assessee was that of a contractor and, consequently, Assessee was incapable of assigning any rights better than that of a contractor of M/s Prabhu Construction.

6. The CIT(Appeals) as well as the Income Tax Appellate Tribunal (ITAT), upon consideration of the clauses of the agreements concluded that the Asseesee assigned the rights in favour of M/s. Prabhu Construction. They have concurrently held that this was sale of area in the two projects and this was not a case where the Assessee had merely engaged M/s. Prabhu Construction as its contractor. These findings of fact, concurrently recorded cannot be said to be vitiated by any perversity or misreading of the documents on record. The two authorities have basically taken a plausible view on the basis of the interpretation of the agreements which forms part of the record.

In the absence of any use of perversity being made out, it would not be proper for us to interfere in such finding of fact in exercise of the jurisdiction under Section 260 (of Income Tax Act, 1961) A of the IT Act.

7. Once the finding of facts are to be sustained, it is obvious that the provisions of Section 194 (of Income Tax Act, 1961) C of the IT Act cannot be said to be attracted. Section 194 (of Income Tax Act, 1961) C of the IT Act deals with deduction of tax at source when it comes to payment to contractors. In the present case, since neither the Assessee nor M/s. Prabhu Construction can be styled as contractors, it is obvious that the provisions of Section 194 (of Income Tax Act, 1961) C of the IT Act were not attracted as held by both the Commissioner (Appeals) and the ITAT.

8. Section 194-C (of Income Tax Act, 1961) refers to any person responsible for paying 'any sum' to any resident referred to as contractor in the said section for carrying out any work in pursuance of a contract. The expression 'sum', in the context, would mean sum of cash money as was held by the Hon'ble Supreme Court in the case of H.H. Sri Rama Verma vs. Commissioner of Income Tax, Ernakulam, 1991 Supp (1) SCC 209, though in the context of the provisions of Section 80 (of Income Tax Act, 1961)- G of the IT Act as then stood. The Hon'ble Apex Court has held that when the language of the provision is plain and clear, the Courts cannot enlarge the scope of the provision by adopting an interpretative process.

9. Accordingly, the first substantial question of law is liable to be answered against the Revenue and in favour of the Assessee.

10. The second question of law is really consequential and depends upon the answer to the first substantial question of law. If the ITAT, in the impugned order had held that since the provisions of Section 194-C (of Income Tax Act, 1961) were not applicable, the consequent provisions of Section 40(a)(ia) (of Income Tax Act, 1961), will also not apply for making disallowance of the expenditure in computing the income under the head 'income from business or profession'. The ITAT, in such circumstances, was quite justified in holding that the CIT was not right in taking the view as the costs incurred in construction is a capital cost for computation of income under Section 48 (of Income Tax Act, 1961). Accordingly, even the second substantial question of law is required to be answered against the Revenue and in favour of the Assessee.

11. Accordingly, both the substantial questions of law are liable to be answered against the Revenue and in favour of the Assessee.

12. As a consequence, this appeal fails and is hereby dismissed. There shall be no order as to costs.

C. V. BHADANG, J. M. S. SONAK, J.

×

Questions

No TDS Required for Property Sale Disguised as Construction Contract

Write your CommentSimilar Posts

Generic

- Reportdata/5320.pdf