Delhi High Court Reduces Penalty for Inaccurate Expense Claims Due to Lack of S…

Full News

Delhi High Court Reduces Penalty for Inaccurate Expense Claims Due to Lack of Supporting Bills

Delhi High Court Reduces Penalty for Inaccurate Expense Claims Due to Lack of Supporting Bills

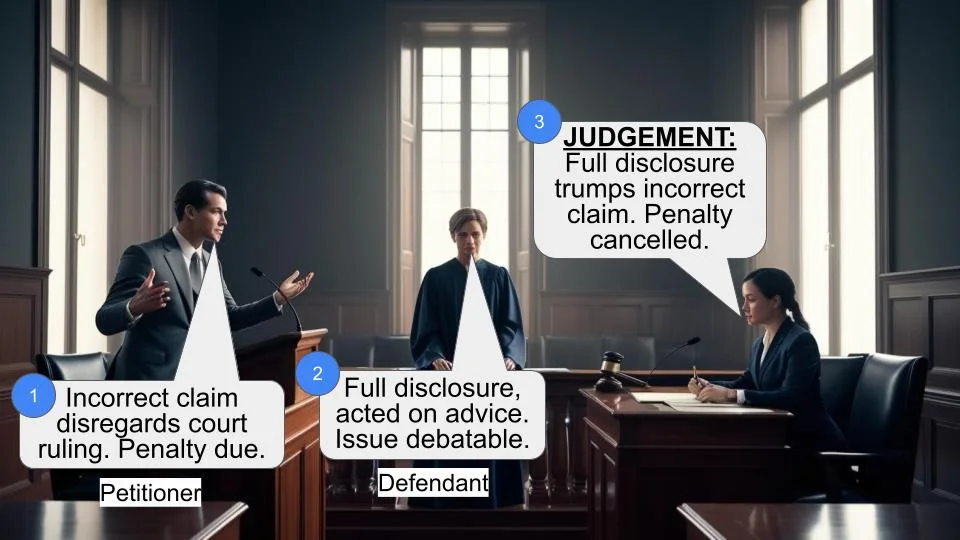

The Delhi High Court dealt with a case involving Clariant Chemicals India Ltd. and the Assistant Commissioner of Income Tax. The main issue was the imposition of a penalty on Clariant Chemicals for failing to produce supporting bills for certain expenses claimed as deductions. The court upheld the penalty but reduced the amount from the original sum to Rs.39,76,739.

Get the full picture - access the original judgement of the court order here.

Case Name:

Clariant Chemicals India Ltd. vs. Assistant Commissioner of Income Tax (High Court of Bombay)

Income Tax Appeal No. 1685 of 2012

Date: 7th January 2015

Key Takeaways

- The court upheld the imposition of a penalty under Section 271(1)(c) (of Income Tax Act, 1961), for furnishing inaccurate particulars of income.

- The penalty was reduced from the original amount to Rs. 39,76,739 due to the partial production of supporting bills.

- The court emphasized that audit reports and minutes of meetings were insufficient to prove the genuineness of the transactions without the supporting bills.

Issue

Was the imposition of a penalty under Section 271(1)(c) (of Income Tax Act, 1961), justified when the assessee failed to produce supporting bills for claimed expenses?

Facts

- Clariant Chemicals India Ltd. claimed deductions for certain expenses.

- The supporting bills for these expenses were not produced, leading to the disallowance of the expenses and the imposition of a penalty.

- The Tribunal and the Commissioner of Income Tax (Appeals) upheld the penalty but reduced the amount based on the partial production of bills.

Arguments

For the Assessee:

- The expenses were genuinely incurred, and the failure to produce bills should not lead to a penalty.

- Audit reports and other materials should be considered sufficient evidence.

For the Revenue:

- The failure to produce supporting bills justified the disallowance of expenses and the imposition of a penalty.

- The audit reports and other materials were not sufficient to prove the genuineness of the transactions.

Key Legal Precedents

- Commissioner of Income Tax vs. Reliance Petro (322 ITR 158)

- Price Waterhouse vs. Commissioner of Income Tax (348 ITR 306)

- Additional Commissioner of Income Tax vs. Jay Engineering (113 ITR 389)

Judgement

The Delhi High Court upheld the imposition of the penalty but reduced the amount to Rs.39,76,739. The court found that the Tribunal did not act perversely or commit an error of law. The audit reports and minutes of meetings were deemed insufficient to prove the genuineness of the transactions without the supporting bills.

FAQs

Q1: Why was the penalty imposed on Clariant Chemicals India Ltd.?

A1: The penalty was imposed because the company failed to produce supporting bills for certain expenses claimed as deductions, leading to the disallowance of those expenses.

Q2: What was the original penalty amount, and what was it reduced to?

A2: The original penalty amount was higher, but it was reduced to Rs.39,76,739 by the Tribunal.

Q3: Were audit reports and minutes of meetings considered sufficient evidence?

A3: No, the court found that these documents were not enough to prove the genuineness of the transactions without the supporting bills.

Q4: What section of the Income Tax Act was invoked for the penalty?

A4: The penalty was imposed under Section 271(1)(c) (of Income Tax Act, 1961).

Q5: Did the court find any substantial question of law in the appeal?

A5: No, the court did not find that the appeal raised any substantial question of law and dismissed it without any order as to costs.

This Appeal challenges the order passed by the Income Tax Appellate Tribunal, copy of which is “AnnexureO” to the Memo of Appeal dated 18th May, 2012.

2] The assessment year in question is 2003-04.

3] The Assessee Appellant challenged the order passed by the

Commissioner of Income Tax (Appeals), namely, the First Appellate

Authority dated 31st May, 2010 before the Tribunal and raised the issue of disallowance of capital expenditure of Research and Development of

Rs.48,76,810/ and essentially the imposition of penalty under section

271(1)(c) after such disallowance.

4] Mr. Sanjiv Shah, learned counsel, appearing on behalf of the

Assessee in support of this Appeal submits that it raises substantial

questions of law. He submits that the substantial question of law is;

whether the Tribunal was justified in upholding the imposition of penalty pertaining to addition of Research and Development expenditure?

In the submission of the counsel, none of the ingredients of section 271(1)(c) (of Income Tax Act, 1961) read with explanation thereto can be said to be attracted. This was not a case, according to him of the expenditure not being incurred at all. The expenditure has not been held to be false. The deduction claimed could not be substantiated according to the Tribunal but the Tribunal omitted from consideration relevant material. In that regard, our attention is invited by Mr. Shah to the Annexures to this memo of Appeal. These Annexures, inter alia, are the entries in the profit and loss account and the books which have to be maintained statutorily according to the counsel.

The entries in this books have been certified and there are reports of the auditors. The auditors have specifically observed that the expenditure was incurred. That the Research and Development activities carried out by the Assessee required it to maintain complete infrastructure. The expenses

have been, therefore, incurred in relation thereto. Merely because the

supporting bills could not be produced does not mean that the

presumption under section 271(1)(c) (of Income Tax Act, 1961) has not been rebutted. The

presumption has been rebutted and by this overwhelming evidence and

material on record. In such circumstances, when the Hon'ble Supreme

Court holds that even the auditors report is a vital material, then, all the more, the findings of fact cannot be sustained. They are contrary to law and, therefore, the Appeal raises a substantial question of law, is the submission.

5] Alternatively and without prejudice submission is that the Tribunal

could not have sustained the penalty on the original addition of

Rs.48,76,810/. The Tribunal has itself derived the figure Rs.39,76,739/ .

The penalty at best could have been sustained to this figure.

6] Mr. Shah has relied upon section 271(1)(c) (of Income Tax Act, 1961),

1961. He has relied upon the judgment of the Hon'ble Supreme Court in

the case of Commissioner of Income Tax V/s. Reliance Petro reported in

322 ITR 158. Mr. Shah has relied upon the judgment in the case of Price

Waterhouse V/s. Commissioner of Income Tax reported in 348 ITR 306

rendered by the Hon'ble Supreme Court and a Division Bench judgment of

the Hon'ble Delhi High Court rendered in the case of Additional

Commissioner of Income Tax V/s. Jay Engineering reported in 113 ITR

389.

7] On the other hand, Mr. Chhotaray appearing on behalf of the

Revenue submits that the Appeal does not raise any substantial question

of law. There are findings of fact rendered concurrently. The deductions

were claimed on the basis of expenses incurred. It may be that certain

expenses have been termed as capital expenditure and, therefore, incurred in relation to the Research and Development wing, hence sustained, but the Assessing Officer, the Commissioner of Income Tax (Appeals) and the Tribunal in Quantum Proceeding as also in Penalty Proceeding concurrently found that there were 9 items of revenue expenditure. In relation to 6 items despite several opportunities being given, the Assessee failed to produce the relevant documents. It is in such circumstances that the Tribunal held that none of the judgments could assist the Assessee.

The judgments proceed on the footing that when a claim is raised and it

could not be sustained or proved, then, straightway the imposition of

penalty was not justified. Further, the auditors report could be a vital

material at the time of assessment but during the course of penalty

proceedings the judgments rendered in assessment matters will not be of

any assistance. Therefore, these are findings of fact consistent with the material which were on record. They cannot be termed as perverse or

vitiated by any error of law apparent on the face of the record. The

Appeal, therefore, does not raise any substantial question of law and

deserves to be dismissed.

8] With the assistance of the counsel appearing for the parties, we

have perused the Appeal paper book and copies of all the relevant orders

and other material annexed to the same.

9] The Tribunal had before it the order passed by the First Appellate

Authority on 31st May, 2010. That order, to the extent, it imposes penalty on disallowance of capital expenditure on Research and Development has been upheld by the Tribunal. True, it is that the Tribunal has deleted the penalty imposed in relation to other claims or additions. Further, in Quantum Proceedings the Tribunal has partly allowed ground No.4 and directed the Assessing Officer to allow the claim of the Assessee on account of claim of Capital Expenditure to the extent of Rs.7,70,190/(see the order dated 27th August, 2010 in Income Tax Appeal No.1271/Mum/2007). However, the Tribunal in the impugned order referred to the factual material in para 7 and found that during the Assessment Proceedings, the Assessing Officer had called for the details addition/deletion of fixed assets with date of purchase, cost of assets, date of the installation along with supporting documents. The Assessee produced only three bills. The Assessing Officer found that even those bills were not evidencing the claim made by the Assessee. The Assessee was given one more chance to prove the claim but it did not avail of the same. The judgments of the Hon'ble Supreme Court and particularly in the case of Reliance Petro (supra) have been referred and distinguished by the Tribunal. The Tribunal held that the claim was made for which no evidence was produced. In relation to Reliance Petro (supra) the argument which was accepted by the Hon'ble Supreme Court pertains to the opinion of the Assessing Officer that a particular claim was not permissible. We do not find that the Tribunal misdirected itself while considering the reliance placed by the Assessee on this judgment. Further, the Tribunal also referred to the judgment of the Division Bench of the Delhi High Court. In the Division Bench judgment of the Delhi High Court, the issue arose during the course of Assessment Proceedings. There, the Applicant-Assessee was carry on business of manufacturing of fans etc. on a large scale. The relevant account books of the Assessee were destroyed in fire.

In the returns filed by the Assessee along with the statement of Profit and Loss Account and Balance Sheets a deduction was claimed. That was

disallowed by the Income Tax Officer. However, the First Appellate

Authority and the Tribunal allowed it. The Tribunal, therefore, was asked to refer the two questions of law for opinion of the Delhi High Court.

10] In relation to point No.1, the Delhi High Court concluded that the

detailed information as to expenses which were claimed as deductions

could not be provided as the books for the accounting years were

destroyed by fire. It is in these circumstances that the Tribunal and

equally the Delhi High Court permitted the Assessee to rely on other

materials. Thus, other materials included the auditors report, the extract thereof and the observations and findings therein. It is in that context that the Hon'ble Delhi High Court held that the reports of the auditor can be said to be material on which reliance could be placed by the Income Tax Authorities. We do not see how such observations would render any assistance because in the present case at all stages, whether in Quantum Proceedings or Penalty Proceedings the materials were the bills which were required to be produced. It was not the case of the Assessee that these have been destroyed or lost. The claim was that there was other material. However, it has been concurrently found that the bills have not been produced. In these circumstances, the expenses were disallowed and the penalty was imposed. That was on the satisfaction that the Assessee has furnished inaccurate particulars. The facts material to the computation were, therefore, not produced and in relation to such an act on the part of the Assessee, it is open for the authorities to take assistance of section 271(1)(c) (of Income Tax Act, 1961) read with explanation 1(B). This was a case where the explanation gave was not sustained. The genuineness of the claim itself was in issue and in our opinion the Tribunal while upholding the order of Commissioner of Income Tax (Appeals) and that of the Assessing Officer partially did not act perversely nor committed an error of law apparent on the face of the record. Its order refers to all the opportunities

that were extended and given by the Assessing Officer during Quantum

Proceedings and Penalty Proceeding. Equally the findings of the

Commissioner of Income Tax (Appeals) that before him as well such

opportunity was given but not availed of by the Assessee. The Tribunal

instead of denying any request firstly gave an opportunity to the Assessee to once again produce the materials. Secondly, it interfered with the orders partially by referring to the three bills which were produced. Thus,out of 9 items, the bills or supporting documents in relation to the 6 items have not been produced. The Tribunal concluded that the penalty should not be worked out or computed on the sum quantified and upheld by the Assessing Officer and the Commissioner of Income Tax (Appeals) but reduced it to Rs.39,76,739/. The penalty will now be levied in terms of the order passed by the Tribunal. We have no doubt that such an exercise will be carried out by the Assessing Officer. To our mind, the further observations by the Tribunal were really unnecessary. They are made so as to emphasize the object and purpose of inserting a provision like section 271(1)(c) (of Income Tax Act, 1961) in the Income Tax Act, 1961. We do not agree with Mr. Shah that audit reports and minutes of meeting were important or brushed aside by the Tribunal. The Tribunal in para 9 held that in the given facts and circumstances these documents were not enough to prove the genuineness of the transactions. This is not a finding running contrary to law much less perverse.

11] For the reasons aforesaid indicated, we do not find that this Appeal

raises any substantial question of law. It is, accordingly, dismissed but without any order as to costs.

(S. P. DESHMUKH, J.) (S.C. DHARMADHIKARI, J.)

×

Questions

Delhi High Court Reduces Penalty for Inaccurate Expense Claims Due to Lack of Supporting Bills

Write your CommentSimilar Posts

Generic

- Reportdata/4161.pdf