ITAT's Misstep: Tribunal's Decision Overturned on TDS Non-Compliance

Full News

ITAT's Misstep: Tribunal's Decision Overturned on TDS Non-Compliance

ITAT's Misstep: Tribunal's Decision Overturned on TDS Non-Compliance

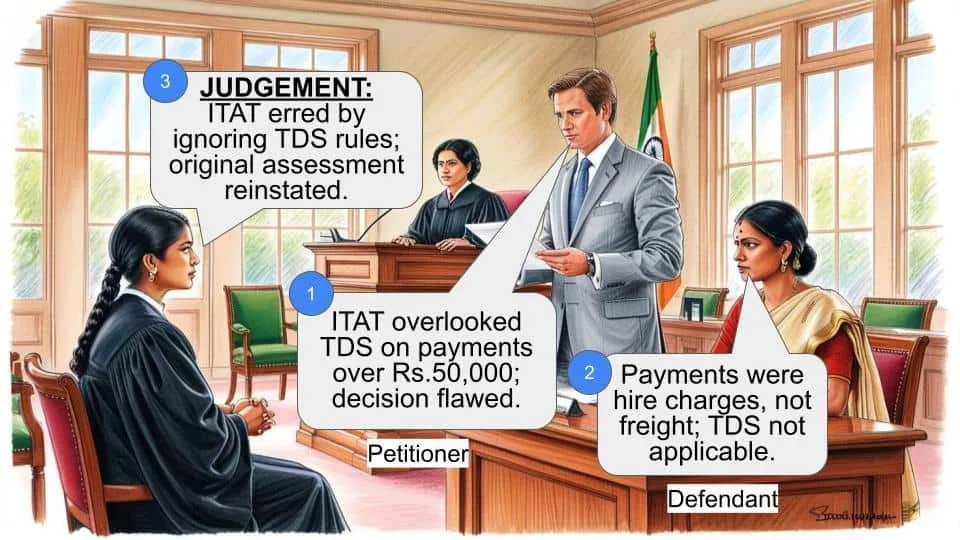

In the case of the Commissioner of Income Tax vs. Maruti Subray Patil, the court addressed whether the Income Tax Appellate Tribunal (ITAT) erred in its decision regarding the non-deduction of tax at source (TDS) on payments exceeding Rs.50,000. The court found that the ITAT had misapplied legal principles and failed to consider critical facts, leading to the reinstatement of the original assessment order.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Maruti Subray Patil (High Court of Karnataka)

ITA No. 5027 of 2010

Date: 29th July 2015

Key Takeaways:

- The court emphasized the importance of deducting TDS on payments exceeding Rs.50,000 in a financial year, as mandated by Section 194C (of Income Tax Act, 1961).

- The ITAT's reliance on broad principles without addressing specific facts was deemed erroneous.

- The decision underscores the necessity for tribunals to base their judgments on concrete evidence rather than assumptions or oral assertions.

Issue

Did the ITAT err in deleting the addition made under Section 40(a)(ia) (of Income Tax Act, 1961) by ignoring the requirement to deduct TDS on payments exceeding Rs.50,000?

Facts

- Maruti Subray Patil, the assessee, was involved in the transportation business and had a contract with M/s. Infrastructures Logistics Pvt. Ltd. for transporting iron ore.

- The assessee paid over Rs.5 crore as "freight charges" but did not deduct TDS, claiming these were "hire charges" due to an accounting error.

- The Assessing Officer disallowed Rs.4,07,73,435 under Section 40(a)(ia) (of Income Tax Act, 1961) for non-deduction of TDS.

Arguments

- Assessee's Argument: The payments were hire charges, not freight charges, and thus not subject to TDS. The term "freight paid" was a mistake by the accountant.

- Revenue's Argument: The payments exceeded Rs.50,000, necessitating TDS deduction under Section 194C (of Income Tax Act, 1961). The ITAT failed to consider the aggregate payments and relied on unsubstantiated claims.

Key Legal Precedents

- Section 194C (of Income Tax Act, 1961): Mandates TDS deduction on payments exceeding Rs.50,000 in a financial year.

- Section 40(a)(ia) (of Income Tax Act, 1961): Disallows certain expenses if TDS is not deducted as required.

Judgement

The court set aside the ITAT's decision, reinstating the original assessment order. It held that the ITAT erred by not considering the aggregate payments and relying on broad principles without factual basis. The court emphasized the need for TDS deduction on payments exceeding Rs.50,000.

FAQs

Q1: What was the main issue in this case?

A1: Whether the ITAT erred in deleting the addition made under Section 40(a)(ia) (of Income Tax Act, 1961) by ignoring the requirement to deduct TDS on payments exceeding Rs. 50,000.

Q2: Why was the ITAT's decision overturned?

A2: The ITAT's decision was overturned because it relied on broad principles without addressing specific facts and failed to consider the aggregate payments exceeding Rs.50,000.

Q3: What does this case mean for businesses?

A3: This case highlights the importance of complying with TDS requirements on payments exceeding Rs.50,000 to avoid disallowance of expenses under Section 40(a)(ia) (of Income Tax Act, 1961).

Q4: How does this case impact the interpretation of Section 194C (of Income Tax Act, 1961)?

A4: It reinforces the interpretation that TDS must be deducted on aggregate payments exceeding Rs.50,000 in a financial year, not just on individual payments.

1. This appeal is preferred under the provisions of Section 260A of ITA Act, 1961, arising out of the order dated 25.11.2009 passed by the Income Tax Appellate Tribunal, Panaji Bench, Panaji in ITA No.86/PNJ/2009, praying that the Hon’ble Court may be pleased to:

I) Formulate the substantial questions of law and further has stated hereinafter;

II) Allow the appeal and set aside the orders passed by the ITAT, Panaji Bench in ITA No.86/PNJ/2009, dated 25.11.2009, whereby the order of the appellate Commissioner dated 30.03.2009 confirming the order of the assessing officer was set aside and confirm the assessment of the assessing

authority for the assessment year 2005-06.

2. The above appeal is filed by the Revenue impugning the order passed by the Tribunal.

3. The substantial questions of law that arise for consideration in the

above appeal are as follows:

1. Whether in the facts and circumstances of the case, the ITAT is right in law in deleting the addition made under Section 40(a)(ia) (of Income Tax Act, 1961) ignoring the facts that there was oral contract with transporters which was evident from the fact that, payments made to each lorry owner exceeded Rs.50,000?

2. Whether the ITAT is right in deleting the addition made ignoring Explanation-III to Sectiion 194C defining “Work” as only carriage of goods and not sub-contract of entire work as held by ITAT and also ovelooking Uttaranchal High Court decision in 290 ITR 530 wherein, it is held that once

agents are appointed by contractor liability to TDS arises under Sectiion 194C?

3. Whether the ITAT is right in deleting the addition made on the ground that entire work undertaken by contractor was not sub-contracted to transporters ignoring provisions of Section 194C(2) (of Income Tax Act, 1961) which clearly provides that, even sub-contracting part of work by contractor also attracts T.D.S.?

4. The brief facts of the case are as follows:

The assessee, who is the respondent herein claims to be in the

business of transportation. It is the further claim by the assessee that he

had entered into a contract with one M/s.Infrastructures Logistics Pvt.

Ltd., Goa for transportation of iron ore from Sandur Mines to a place

called Redi. It is further asserted that under the contract, the assessee has claimed to have paid a sum of Rs.5,10,16,407/-. In the books of

account of the said assessee, the amount mentioned supra was described

as “Freight Paid”.

It is the case of the Revenue that the Assessing Authority at the

time of scrutinizing the returns for the assessment year 2005-06 noticed

that the assessee had made aggregate of payment in excess of

Rs.50,000/- in a single assessment year and towards freight charges to

various truck owners/operators, without deducting tax at source, on

such payments, as mandated under the provisions of Section 194C (of Income Tax Act, 1961) of

the IT Act. Upon noticing the discrepancy, the assessee was called upon

to explain. Whereupon it was claimed by the assessee that there is no

sub-contract and that he has loaded the vehicle whichever had come to

the site and that the heading “freight paid” is a misnomer and a factual

error and that the amount paid in fact represent the hire charges and not

freight charges. Rejecting the specious contentions the Assessing

Authority disallowed certain amounts. The Assessing Authority noticing

the discrepancy was constrained to invoke the provisions of Section

40(a)(ia) of I.T. Act and disallowed the amount of Rs.4,07,73,435/-.

5. The assessee aggrieved by the assessment order preferred an

appeal before the Commissioner Appeals, contending that there was

neither an oral or written contract, by which the contract work of

transportation was sub-contracted to the truck owners and it was

contended that the amounts paid represent the hire charges and are not

freight charges. It was also contended that in the absence of the sub-

contract the amount though described as freight charges ought to be

read as “hire charges only”. The Commissioner (Appeals) is said to have

thoroughly scrutinized the records and is said to have found that the

payments made to the various vehicle owners depended on the quantity

transported and in this regard, he has relied upon certain vouchers dated

between 13th March to 31st March for the year 2005, wherein it is seen

that for the same distance, different rates have been paid to different

vehicles under different voucher numbers and thus arrived at the

conclusion that the amounts expended was indeed freight charges and

not hire charges. Though, it was the specific case of the assessee that the

amounts paid reflect only the hire charges. No material has been placed

to demonstrate the same either before the Assessing Officer or before

the Commissioner (Appeals). Hence, the Commissioner (Appeals) by a

detailed and reasoned order was pleased to conclude that the amounts

allegedly paid are indeed freight charges and not hire charges and

rejected the contention of the assessee that the entry “freight paid” is on

account of the mistake committed by the accountant and in fact such

amount represent the hire charges only. It is the admitted case of the

assessee that there are no written contract nor bills issued by the

transporters and the entire case is sought to be demonstrated and

supported only by the vouchers maintained by the assessee.

6. The other undisputed fact is that the asseessee has described the

payments in the vouchers as “freight charges” (though it is alleged to be

the result of error by the assesseee’s accountant) in its books of

accounts.

7. In the above background of facts the assessee aggrieved by the

order of the Commissioner (Appeals) preferred the appeal before the

Income Tax Appellate Tribunal impugning the conclusion of the

assessing officer and its confirmation by the Commissioner (Appeals)

concluding that the provisions of Section 194C(2) (of Income Tax Act, 1961) was

attracted and the assessing authority invoked consequential provisions of

Section 40(a)(ia) (of Income Tax Act, 1961).

8. The learned counsel for the appellant would take the Court

through the order rendered by the appellate Tribunal. He would state

that the Tribunal after merely recanting the respective submissions of

the parties before the authorities below, thereafter, simply proceeded to

rely upon the judgments and citations, to dispose off the appeals. He

would submit that the Tribunal misdirected itself by relying upon the

broad principles to dispose off the appeal, which has resulted in grave

miscarriage of justice.

9. The appellant’s counsel dilating at the bar, would point out that

the facts pleaded herein and the facts in the case laws relied upon are at

variance and the facts are not identical. He would submit that the

Tribunal erred in observing the fact that the decisions of the

Visakahpattanam Bench involved almost similar facts. He would further

submit that the Tribunal erred in accepting the contention of the

assessee at the face value. The contention is that there are no written

sub-contract and hence, in the absence of written sub-contracts the

payments have to be construed as hire charges is not only materially

irregular, but contrary to the law resulting in travesty of justice and

rendition of an illegal order which resulted in unjustified avoidance of

tax.

10. The appellant would further submit that the Tribunal materially

erred in not appreciating the various contentions on behalf of the

revenue. He would contend that the Tribunal erred in holding the

assessing authority responsible for not placing on record, any material to

demonstrate that the obligation of the assessee are taken over by the

truck owners engaged by the assessee.

11. The appellant counsel would further submit that the Tribunal

erred in holding that the element of risk remained with the assessee only

and was not transferred to the truck owners. He would submit that it is

not the case of the assessee nor the assesseee placed any material to

demonstrate or buttress the case made out by the Tribunal.

12. The appellant counsel would submit that the reasoning of the

Tribunal that the Revenue failed to place any material to controvert “oral

statement” of the assessee is not only perverse but also contrary to all

known canons of evidence. He would submit that the reasoning of the

Tribunal calling upon the revenue to disprove or controvert,

unsubstantiated and uncorroborated self serving statement of the

assessee is not only whimsical but highly illegal. He would state that no

burden is caste upon a person to disprove anything that has not been

proved.

13. The learned counsel for the appellant would submit that the

vouchers and entries in the books of accounts are the evidence of

contract entered into and executed on behalf of the assessee. He would

submit that it is the case of the assessee that he owned only five trucks

and that the trucks of third party has been used to transport the

materials, that is to execute the contract entered into between the

assessee and his principal. He would submit that the same are evidence

of an implied agreement and agreements include oral agreement also. He

would state that it is an undisputed fact that no material has been placed

by the assessee to either (a) demonstrate that no written contract has

been executed between the truck owners and the assessee; (b) no

material is placed by the assessee to demonstrate that the element of risk

remained with the assessee only and was not transferred to the

transporter; (c) no material was placed before the original authority or

the Tribunal to demonstrate that the payments are hire charges only and

not freight charges; and (d) no material is placed either before the

Tribunal or the authorities to corroborate and demonstrate the

statement / alibi of the assessee that the entry in the books of accounts

described as “freight charges” is as a result of factual mistake. He would

submit that in the light of the above, the question of disproving a

unsubstantiated or non existing facts does not arise. He would state that

shifting of the burden of proof on the revenue to disprove the non-

existing fact is contrary to law under the Indian Evidence Act and on the

above contentions the appellants counsel would submit that the

impugned order warrant interference at the hands of the Court and

requires to be set aside.

14. Per contra, the learned counsel for the respondent/assessee

would reiterate his contentions that the payments are indeed hire charges

and the entry in the books of accounts and vouchers describing the

payments as “freight charges” is a factual mistake committed by the

assessee’s accountant. That apart he would submit that in the absence of

the written sub-contract, it is erroneous on the part of the revenue to

presume or assume the violation of the mandate of Section 194C(2) (of Income Tax Act, 1961). He

would also strongly condemn consequential invocation of the provisions

of Section 40(a)(ia) (of Income Tax Act, 1961). He would submit that the invocation is

bad in respect of the payments that have already been made and that the

provision could be invoked and would be applicable only in respect of

pending payments that are yet to be made. He would submit that if the

interpretation placed by the Assessing Authority is allowed, it would

result in grave in justice as the consequence are very grave and have the

capacity to financially ruin the assessee put him out from the business

permanently.

15. The respondent counsel would relay on the various judicial

pronouncements by the Tribunals and of the Panjab and Harayana High

Courts.

16. The above appeal came to be admitted on 03.02.2011 on the

substantial questions of law as framed by the revenue. Apart from the

same, this Court would also deem it necessary to frame an additional

issue, which has arisen incidentally as a result of the approach adopted

by the Tribunal, the same is as follows:

Whether in the facts and circumstances of the case, the income

tax appellate Tribunal was right in allowing the appeal by merely

relying on broad principles without reference to the critical facts of the

case?

17. For the sake of brevity and convenience the provisions of Section

194C of IT Act, are culled out for reference purpose only.

“194C. [(1) Any person responsible for paying any sum to any

resident (hereinafter in this section referred to as the contractor) for

carrying out any work (including supply of labour for carrying out any

work) in pursuance of a contract between the contractor and—

(A) any company; or

shall, at the time of credit of such sum to the account of the contractor or at

the time of payment thereof in cash or by issue of a cheque or draft or by

any other mode, whichever is earlier, deduct an amount equal to—

(i) one per cent in case of advertising,

(ii) in any other case two per cent,

of such sum as income-tax on income comprised therein:

Provided that no individual or a Hindu undivided family shall be liable

to deduct income-tax on the sum credited or paid to the account of the

contractor where such sum is credited or paid exclusively for personal

purposes of such individual or any member of Hindu undivided family.]

(2) Any person (being a contractor and not being an individual or a

Hindu undivided family) responsible for paying any sum to any resident

(hereafter in this section referred to as the sub-contractor) in pursuance of a

contract with the sub-contractor for carrying out, or for the supply of

labour for carrying out, the whole or any part of the work undertaken by

the contractor or for supplying whether wholly or partly any labour which

the contractor has undertaken to supply shall, at the time of credit of such

sum to the account of the sub-contractor or at the time of payment thereof

in cash or by issue of a cheque or draft or by any other mode, whichever is

earlier, deduct an amount equal to one per cent of such sum as income-tax

on income comprised therein:

Explanation III. —For the purposes of this section, the expression

“work” shall also include—

(A) carriage of goods and passengers by any mode of transport

other than by railways;

(3) No deduction shall be made under sub-section (1) or sub-section (2)

from—

(i) the amount of any sum credited or paid or likely to be credited or paid

to the account of, or to, the contractor or sub-contractor, if such sum

does not exceed twenty thousand rupees:

Provided that where the aggregate of the amounts of such sums credited

or paid or likely to be credited or paid during the financial year

exceeds fifty thousand rupees, the person responsible for paying such

sums referred to in sub-section (1) or, as the case may be, sub-section

(2) shall be liable to deduct income-tax [under this section:]”

18. The provisions of Section 40(a)(ia) (of Income Tax Act, 1961) are culled out for the sake of

convenience:

40. Notwithstanding anything to the contrary in sections 30 to [38], the

following amounts shall not be deducted in computing the income

chargeable under the head “Profits and gains of business or

profession”,—

(a) in the case of any assessee—

[(i) any interest (not being interest on a loan issued for public

subscription before the 1st day of April, 1938), royalty, fees for

technical services or other sum chargeable under this Act, which is

payable,—

(A) outside India; or

(B) in India to a non-resident, not being a company or to a

foreign company,

(ia) any interest, commission or brokerage, [rent, royalty,] fees for

professional services or fees for technical services payable to a resident,

or amounts payable to a contractor or sub-contractor, being resident,

for carrying out any work (including supply of labour for carrying out

any work), on which tax is deductible at source under Chapter

XVII-B and such tax has not been deducted or, after deduction, has

not been paid during the previous year, or in the subsequent year

before the expiry of the time prescribed under sub-section (1) of section

200:”

19. A perfunctory reading of the provisions of Section 194C (of Income Tax Act, 1961) of the

Act obviates the necessity for any interpretational exercise as the

provisions are unambiguous. A reading of the provisions of Section

194C mandates that any person who is involved in executing any

contract or carrying out any work under a contract between any

individual and company etc., and where the aggregate of payments to

such person/s or agency engaged by a contractor exceeds Rs.20,000/-, a

mandate is cast on such persons making payments to deduct a sum of

one percent or two percent at the time of making payments to the

person, who carries out the work or such portion of the work under the

Contract. Thus in a sense, the provisions of Section 194C (of Income Tax Act, 1961) enjoins a

positive duty on the persons making the payment to deduct a sum at the

specified rate and as mandated under the Act and that too at the time of

making of payments and the deducted amounts are to be deposited with

the authorities. One such activity which has been brought within the

sweep of the above section is transportation of goods or carriage of

goods by any mode of transport other than the railways.

20. The provisions of Section 40(a) (of Income Tax Act, 1961) provides an exemption from the

rigors of Chapter XVII-B, and the said Chapter includes the provisions

of Section 194C (of Income Tax Act, 1961), provided aggregate of payments made to a

person/entity does not exceed Rs.20,000/-.

21. In the background of the law it is necessary to revisit the facts of

this case and address the poser as to whether the said provisions are

applicable and the revenue was justified in invoking the same.

22. The undisputed facts are that the assessee declared a total income

of Rs.25,14,811/- for the assessment year 2005-06. On an inspection of

the accounts by the A.O., it was revealed that the assessee had received

a sum of Rs.5,74,48,399/- as freight charges from M/s.Infrastructures

Logistics Pvt. Ltd., Goa and out of that he declared that he had paid a

sum of Rs.5,10,16,407/-. The said information was furnished vide

questioner dated 06.09.2007, wherein the assessee was asked to furnish

the details of freight paid and also called upon to explain the reason as to

why a tax was not deducted on the freight charges paid. In response to

the same, the assessee vide his letter dated 19.11.2007 stated that it is not

a freight charges but it is lorry hire charges and that by mistake the

accountant has used the word freight paid. Thus it was asserted for the

first time by the assessee that he had hired the vehicles belonging to

others for transportation of materials under contract with principle. It

was also asserted that there are no written contracts with the lorry

owners and who ever was available had been employed by them and

paid hire charges and that as the lorry owners are not fleet owners and

possess one or two trucks, the question of making TDS from hire

charges did not arise. With reference to the explanation offered under

the letter dated 19.11.2007, a further query was addressed by the

Assessing Officer on 12.12.2007. It was pointed out to the assessee that

his explanation vide letter dated 19.11.2007 was self contradictory. It was

pointed out that in one breath he has stated that the amounts paid to the

lorry owners is not freight charges but hire charges and in next breath,

he admits that there are no contracts. It was further pointed out that

there is no hire agreement presented before the Assessing Officer. It was

further pointed out that except for a few cases, the aggregate of amounts

paid to each lorry owners was in excess of Rs.50,000/- and as noted

supra only those payments of aggregate which do not exceed

Rs.50,000/- are exempted under sub-section 3 of Section 194 (of Income Tax Act, 1961)

and where no single payment of Rs.20,000/-, the same are exempted

from the purview of sub-section 3 of Section 194C (of Income Tax Act, 1961) and failure attracts

the consequences under Section 40(a)(ia) (of Income Tax Act, 1961).

23. In reply, the assessee has reiterated that the word freight paid has

been mistakenly used by his accountant and that there are no contracts

with the lorry transporters and that even if it is assumed that there is

implied contract, then the contract is for one trip and that the second

trip will be an independent and that no amount in excess of Rs.20,000/-

has been paid. That is, in sum and substance, the defence of the assessee

is that as he has not paid any transporter in excess of Rs.20,000/- for any

single trip, that is there is no single transactions where payment has

exceeded Rs.20,000/-. But it is to be noted that it has not been denied by

the assessee, that in most of the cases, the aggregate of sums paid in the

assessment year is in excess of Rs.50,000/-. It is seen that the assessee

has conversely argued before the assessing authority stating that he has

not made any single payment either in excess of Rs.20,000/- or

Rs.50,000/- and hence, he has sought exemption from the purview of

the Act mandating deduction of tax at sources. But yet again it is to be

noted that there is no denial of the fact that the aggregate of the

payment in the assessment year in respect of the most of the

transporters exceeds Rs.50,000/- and the provisions of Section 194C(i) (of Income Tax Act, 1961)

read with Section 194C(iii) (of Income Tax Act, 1961) mandates that, if the sum credited/paid to

any person exceeds Rs.50,000/- in a financial year, then the said sums

are liable for deduction of tax at source, in other words, tax is to be

deducted at source (TDS). The assessee has also relied upon a circular

dated 01.10.2004 and the same has also been rejected in view of the fact

that the provisions of Section 194C(i) (of Income Tax Act, 1961) had been amended with effect

from 01.10.2004. Thus, in effect all the contentions raised by the

assessee were negated and the assessing authority invoking the

provisions of section 40(a)(ia) (of Income Tax Act, 1961) disallowed a sum of

Rs.4,07,73,435/- out of the declared sum of Rs.5,10,16,407/- as this

represented the total sum of amounts, where the aggregate of payments

made to the transporters exceeded Rs.50,000/- in the assessment year. It

is seen that the Assessing Authority has also brought out specific

instance which go to demolish the contention of the assessee. The

assessee and his Chartered Accountant attended hearing before the

Assessing Authority.

24. The dispute in a nutshell is as to whether the provisions of

Section 194C (of Income Tax Act, 1961) can be invoked only if any single payment

exceeds Rs.50,000/- or can be invoked if the aggregate of payment in an

assessment year exceeds Rs.50,000/-. As stated supra there is no

controversy regarding the said contention, the provision is clear and

unambiguous and the word aggregate has been specifically used. In that

view of the matter, the assertion on behalf of the assessee, that only in

respect of payment which exceeds Rs.50,000/- is liable to be deducted at

source is liable to be rejected and is accordingly rejected. Accordingly,

the substantial questions of law as framed by the appellant/revenue is

answered in favour of the revenue.

25. The simple issue has been approached by the Tribunal in an

erroneous manner. The Tribunal under the guise of broad principles has

misdirected itself resulting in adjudication of the dispute on the basis of

inferences and assumption, contrary to law. The Tribunal has rendered a

finding without reference to the basic and critical facts which were

necessary for adjudication. The Tribunal has gravely erred in trying to

adjudicate the appeal merely on the basis of broad principles. The

Tribunal gravely erred in inferring that, there ought to be a sub-contract

in writing and only in a such an event the provisions of the Act can be

invoked. It further seriously erred in holding the factual issue in favour

of the assessee, when not even a shred as evidence was placed before it.

A pointer in this direction, is the finding that no risk was undertaken by

the lorry owners. It was not the case of the assessee before the Assessing

Authority or Commissioner (Appeals). The said contention being

question of fact, the appellate Tribunal erred in accepting the same and

on the contrary ought to have outright rejected the same. It ought to

have seen that it is an improvement to the case put forth by the assessee

before the original authority. It is not the finding of the Tribunal that

any independent material either in the form of say of lorry owners, etc.,

were placed before it compelling it to take a different view than the one

adopted by the original authority. The Tribunal has also gravely erred in

holding that the assessee/appellant had made out a case because the

revenue failed to place any material before it, contraverting the vague

and mere oral assertion of the assessee. The said reasoning is contrary to

all known cannons of the law of evidence, logic and law mandates that

the burden and onus is on the person, who alleges a fact, to prove the

said fact. The assessee has pleaded that the entries “freight paid” is on

account of a mistake committed by their accountant and they have come

up with the excuse very belatedly. This being the factual issue, the

Tribunal did not deem it necessary to call upon the assessee to

demonstrate the said fact, but proceeded to accept the statement as a

proven fact. It appears that the Tribunal has diverted itself from

addressing the core issue, that is whether the assessee has paid any sums,

the aggregate of which exceeds Rs.50,000/- in the assessment year to any

single entity. The Tribunal has not addressed itself to any of the findings

of fact rendered by the Assessing Authority. In particular, several

instances of the aggregate of payments have exceeded Rs.50,000/- in the

assessment year have been placed on record. It does not render any

reasoning to unsettle the finding of the original authority, that even the

agreement can also be an oral and that the transactions with the lorry

owners/transporters is within the purview of the provisions of the Act

as it amounts to carriage of goods other than the railways.

26. The finding that the appeal requires to be allowed in view of the

decision by the Co-ordinate Bench and that of the Punjab and Haryana

High Court in the case of Commissioner of Income Tax Vs. United Rice

Land Limited reported in (2010) 322 ITR 594 (P&H) is erroneous.

Therein the finding of fact, that the amounts paid to the transporter is

by way of hire charges, was rendered on the basis of evidence furnished

by the alleged transporters. The assessee therein was in the manufacturer

and export of rice and there was an identified route, quantity etc., in view

of which certain facts could be easily identifiable. The transportation of

goods was from its premises to the port and in the course of its export.

In the present case, the facts and details are not only hazy but are

obfuscated due to lack of clarity. Apart from stating that the ore was

required to be transported from point (a) to point (b), no details are

provided as to whether the point (b) was a licenced or registered place,

where minerals could be stored there, etc., It is seen that a huge sum

amounting to Rs.5=00 crorers is spent merely for transportation of iron

ore from point (a) to point (b), no details are forth coming whether the

transportation is in the course of business or is being transported to the

hands of end user. In such situation, this Court finds it hard to believe

the version put out by the assessee.

27. The counsel for the respondent is unable to answer the queries in

this direction. As stated earlier, the Tribunal gravely erred in adversely

inferring against the revenue for having failed to disprove the oral

assertion of the assessee.

28. On the other hand, the Tribunal ought to have adversely inferred

against the assessee for having failed to place material to substantiate its

oral assertion. Consequently, the order of the Tribunal is vitiated and

requires to be interfered with. Accordingly, the impugned order under

appeal is set aside and the order of the original authority dated

26.12.2007 stands resurrected. The case of the assessee is rejected and

the question of law formulated by the appellant stands answered in

favour of the revenue.

29. The appeal stands disposed of in the above terms.

Sd/-

JUDGE

Sd/-

JUDGE

×

Similar Ripples

Questions

ITAT's Misstep: Tribunal's Decision Overturned on TDS Non-Compliance

Write your CommentSimilar Posts

Generic

- Reportdata/3579.pdf