Jet Airways’ Tax Liability: No Cessation, No Taxation

Full News

Jet Airways’ Tax Liability: No Cessation, No Taxation

Jet Airways’ Tax Liability: No Cessation, No Taxation

This case involves the Commissioner of Income Tax and Jet Airways (India) Ltd. The main issue was whether certain liabilities related to aircraft leases and other expenses should be taxed under Section 41(1) (of Income Tax Act, 1961). The court decided in favor of Jet Airways, ruling that there was no cessation or remission of liability, and thus, no tax was applicable under this section.

Get the full picture - access the original judgement of the court order here

Case Name

Commissioner of Income Tax vs. Jet Airways (India) Ltd. (High Court of Bombay)

Income Tax Appeal No. 2111 of 2013

Date: 11th January 2016

Key Takeaways

- Section 41(1) (of Income Tax Act, 1961) Application: The court clarified that Section 41(1) (of Income Tax Act, 1961) applies only when there is a cessation or remission of liability that results in a benefit to the taxpayer.

- Lease Extensions: The extension of aircraft leases meant that liabilities had not ceased, so Section 41(1) (of Income Tax Act, 1961) was not applicable.

- Prior Period Expenses: The court upheld the allowance of prior period expenses, provided they are genuine and verifiable.

- Ownership and Depreciation: Jet Airways was recognized as the owner of the aircrafts, allowing them to claim depreciation.

Issue

The central legal question was whether the liabilities related to aircraft leases and other expenses had ceased, thereby making them taxable under Section 41(1) (of Income Tax Act, 1961).

Facts

Jet Airways had extended the lease for several aircrafts, which meant that the liabilities for redelivery expenses were still in place. The Income Tax Department argued that these liabilities had ceased and should be taxed. Additionally, there were disputes over prior period expenses and the ownership of aircrafts for depreciation purposes.

Arguments

- Commissioner of Income Tax: Argued that the liabilities had ceased and should be taxed under Section 41(1) (of Income Tax Act, 1961).

- Jet Airways: Contended that the liabilities had not ceased due to lease extensions and that they were the rightful owners of the aircrafts, allowing them to claim depreciation.

Key Legal Precedents

- Section 41(1) (of Income Tax Act, 1961): This section was central to the case, focusing on the cessation or remission of liabilities.

- Toyo Engineering India Ltd v/s JCIT: Cited by the Tribunal to support the allowance of prior period expenses.

Judgement

The court ruled in favor of Jet Airways, stating that there was no cessation or remission of liability, and therefore, Section 41(1) (of Income Tax Act, 1961) was not applicable. The court also upheld the allowance of prior period expenses and recognized Jet Airways as the owner of the aircrafts for depreciation purposes.

FAQs

Q: What does Section 41(1) (of Income Tax Act, 1961) entail?

A: It applies when a liability that was previously allowed as a deduction ceases, resulting in a benefit to the taxpayer, which then becomes taxable.

Q: Why was Jet Airways not taxed under Section 41(1) (of Income Tax Act, 1961)?

A: Because the liabilities related to aircraft leases had not ceased due to lease extensions, and no benefit was obtained by Jet Airways.

Q: What was the significance of the lease extensions?

A: The extensions meant that the liabilities for redelivery expenses were still in place, so they could not be taxed under Section 41(1) (of Income Tax Act, 1961).

Q: How did the court view the ownership of the aircrafts?

A: The court recognized Jet Airways as the owner, allowing them to claim depreciation on the aircrafts.

1. This Appeal under Section 260-A (of Income Tax Act, 1961), 1961 (the Act) challenges the order dated 5th April, 2013 passed by the Income Tax Appellate Tribunal (the Tribunal). The Assessment Year involved is A. Y. 2006-2007.

2. The Appellant has urged the following questions of law, for our consideration:-

1) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made on account of prior period expenses at Rs.1,48,73,553/-?

2) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made on account of leave encashment in computing the book profit u/s.115JB (of Income Tax Act, 1961) at Rs.11,79,38,279/-?

3) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made by the Assessing Officer on account of redelivery of aircraft under normal provision of the Act of Rs.3,03,04,750/-

4) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made by the Assessing Officer under normal provision of law on account of provision for redelivery of aircraft of rs.1,67,50,541/-?

5) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made on account of accumulated provision on account of redelivery of aircraft acquired on operating lease at Rs.3,28,55,249/-

6) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition of 19,47,65,816/- made by the Assessing Officer on account of treating the provision for obsolescence of as contingent liability while computing profit u/s 115JB (of Income Tax Act, 1961)?

7) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made on account of depreciation on aircraft acquired on hire purchase at Rs.98,42,67,988?

8) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made on account of frequent flyer expenses u/s.115JB (of Income Tax Act, 1961) at Rs.6,91,38,488/-

9) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made on account of repair of premises, furniture and fixtures as capital expenditure by the Tribunal at Rs.2,85,09,245/-?

10) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made on account of prior period expenses at Rs.68,50,425/-?

11) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made on account of Directors personal expenses at Rs.11,65,950/-?

12) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made on account of interest income which was treated as business income as against income from other from sources at Rs.55,42,37,262/-?

13) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made on account of provision of gratuity u/s.115JB (of Income Tax Act, 1961) at Rs.104,41,07,743/-?

14) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made on account of aircraft taken on finance lease at Rs.25,22,07,223?

15) Whether on the facts and in the circumstances of the case and in law the Tribunal is justified in deleting the addition made on account of sale and lease back of five aircrafts at Rs.100,52,85,728/- u/s. 41(1) (of Income Tax Act, 1961)?

3. Regarding Question 1:-

(a) According to the Respondent, it had disputes with the parties in respect of prior period expenses which were settled only during the said assessment year. The Assessing Officer disallowed the claim on the ground that no evidence in support was produced. In appeal, the CIT(A) did not disturb the finding of the Assessing Officer.

(b) On further appeal, the Tribunal in the impugned order held that the details in support of the same were filed by the Respondent Assessee before the Assessing Officer. In principle, the impugned order holds that the prior period expenses are allowable as held by it in Toyo Engineering India Ltd v/s JCIT reported in (2006) 5 SOT 0616) and also by this Court in the case of Commissioner of Income Tax, Delhi v/s Nagri Mills Co. Ltd reported in 1958 (33) ITR page 681. The issue was therefore restored to the Assessing Officer for verification.

(c) The grievance of the Revenue is that as no evidence was produced before the authorities, the prior period expenses should have been disallowed.

(d) We find that the impugned order of the Tribunal has in fact restored the issue to the Assessing Officer to allow the prior period expenditures/ expenses subject to verification. This verification would involve satisfaction of genuineness of the claim. Therefore, in our view, no fault can be found with the impugned order on the above issue.

(e) Thus Question (1) does not give rise to any substantial question of law and is not entertained.

4. Regarding Question 5:

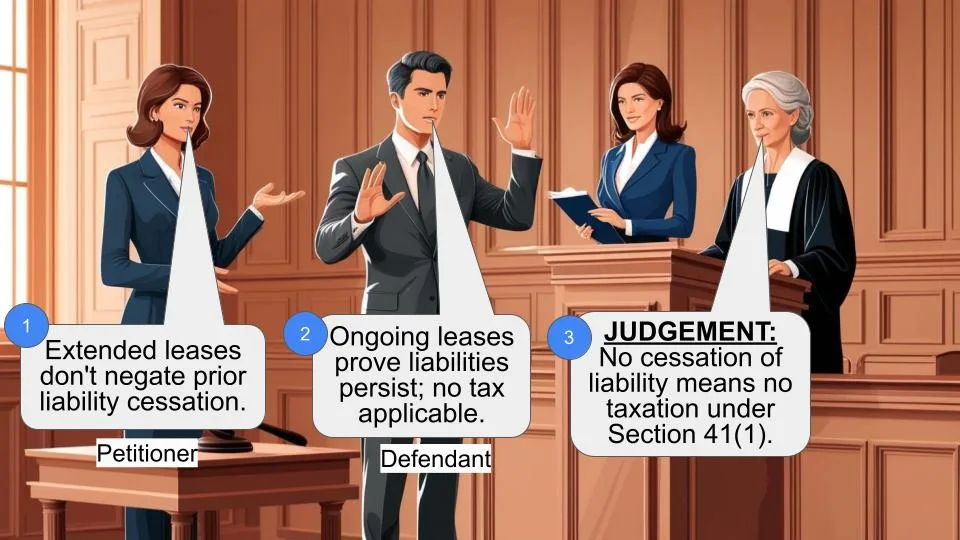

(a) The Respondent-Assessee had made a provision of Rs.3.28 Crores up to 31st March, 2005 in respect of expenses likely to be incurred on redelivery of the four air crafts taken on lease. During the relevant assessment year, the lease period in respect of the four aircrafts was to expire. However, the lease of the four air crafts was extended/renewed for a further period. As a result, the Respondent was not required to redeliver the four aircrafts to the lessor during the subject assessment year. On the basis of the above, the Assessing Officer invoked Section 41(1) (of Income Tax Act, 1961) and held that there was cessation of liability and sought to bring the entire amount which was provided for on the above account of Rs.3.28 Crores to tax.

(b) Being aggrieved, the Respondent-Assessee carried the issue in Appeal to the CIT(Appeals). In appeal, the CIT(Appeals) held that there was no cessation of liability as the lease has been extended for a further period. Thus, expenses which are likely to be incurred at the time of redelivery of the four air craft continues and the provision made continues. Thus, there was no occasion to invoke Section 41(1) (of Income Tax Act, 1961) and the addition was deleted.

(c) On further Appeal by the Revenue, the Tribunal upheld the findings of the CIT(Appeals). The Tribunal by the impugned order holds that as a matter of fact the period of lease has been extended in respect of the four air crafts, and therefore, the provisions made for redelivery expenses could not be said to have ceased for the purposes of invocation of Section 41(1) (of Income Tax Act, 1961).

(d) The learned counsel for the Revenue reiterates the order of the Assessing Officer and prays that the question be admitted.

(e) We find that there are concurrent findings of fact that the lease for the air crafts has been extended for further period and liability of expenses at the time of redelivery of the aircrafts has not ceased. Thus, the same would have to be provided for, as it is likely to be incurred when the lease expires and said four air crafts are redelivered. Section 41(1) (of Income Tax Act, 1961) has application only when there is cessation and/or remission of liability incurred (which has been duly paid and/or provided for) in the subsequent years, consequent of which some benefit in cash or in any other manner were obtained by the party whose liability has ceased. In this case, in fact, there is no cessation or remission of liability nor any benefit obtained by the Respondent-Assessee for the purposes of Section 41(1) (of Income Tax Act, 1961) to be invocable.

(f) Accordingly, the question as framed does not give rise to any substantial question of law and thus not entertained.

5. Regarding Question 10:

(a) The Respondent-Assessee had during the relevant assessment year written back an amount of Rs.1,16,43,548/- on account of excess provision made in earlier years. This on account of inventory and treated the same as prior period income. However, subsequently, the Appellant realized that the amount written back was excessive to the extent of Rs.68.50 lacs and accordingly, reduced that amount from the prior period income.

The Assessing Officer did not accept the reduction of an amount of Rs.68.50 lacs by rectification and held it to be a part of prior period income which he subjected to tax.

(b) Being aggrieved, the Respondent preferred an Appeal to the CIT(Appeals). The CIT(Appeals) on examination of the facts noted that the Appellant had subsequently realized that the amounts which were written back on account of provision for inventory were excessive to the extent of Rs. 68.50 lacs and accordingly reduced the same from the amount written back on account of provision for inventory amount to Rs.116 lacs. This was by way of reversal entry in its books of account. The CIT (Appeals) also placed reliance upon the certificate of the tax auditors in Annexure-XIII in Form-3CD to conclude that the amount of Rs.68.50 lacs was not in the nature of prior period income and deleted the addition.

(c) The Revenue being aggrieved carried the issue in Appeal to the Tribunal. The Revenue before the Tribunal did not controvert the findings of the fact arrived at by the CIT(Appeals). The Tribunal, on examination of the order of the CIT(Appeals) upheld the same as the amount of Rs.68.50 lacs was erroneously shown as prior period income and had rectified the same subsequently. We find that both the CIT(Appeals) as well as the Tribunal have arrived at concurrent findings of fact. The Revenue has not been able to show that the same is in any way perverse and/or arbitrary.

(d) Accordingly the question as framed does not give rise to any substantial question of law and therefore, not entertained.

6. Regarding Question 11:-

(a) The Assessing Officer disallowed the expenditure of Rs.11.65 lakhs on the ground that the expenses were incurred not for the purpose of business but on account of its Directors. Thus, not allowed as deduction while computing the profit and gains for business.

(b) On Appeal, the CIT(Appeal) found that the expenses had been incurred in respect of fuel for staff vehicle, hotel accommodation, parking charges, foreign travel, car hire charges, business promotion expenses, driver's expenses, telephone expenses, repair and maintenance expenses etc. On examination, the CIT(Appeals) found that they were allowable as business expenditure, and therefore, deleted the addition of Rs.11.65 lakhs.

(c) On further Appeal by the Revenue, the Tribunal upheld the findings of CIT(Appeals) and inter alia observed that from the assessment year 2003-2004 to assessment year 2005-2006,a similar disallowance has been deleted by CIT(A) and the Revenue has accepted the same by not challenging the findings on the above count. On examination of the orders of the Assessing Officer and CIT(Appeal), the Tribunal upheld the findings of the CIT(Appeals) that the expenses were incurred for the purpose of business, and therefore, could not be disallowed.

(d) Mr. Tejveer Singh on behalf of the Revenue, places reliance upon the order of the Assessing Officer and pleads that the appeal be admitted.

(e) We find that the CIT(Appeals) as well as the Tribunal have arrived at findings of fact that the expenses of Rs.11,65,950/- were incurred for the purposes of Respondent's business. The concurrent finding of fact has not been shown to be in any way perverse and/or arbitrary to give rise to any substantial question of law. Accordingly, above question is not entertained.

7. Regarding Question No.14:-

(a) The Respondent-Assessee had claimed additional expenditure of Rs.25,22,70,223/- relating to aircrafts taken on finance lease. This claim was made for the first time in revised return of income. The Assessing Officer did not accept to revised return of income and disallowed the claim made by the Respondent-Assessee.

(b) In Appeal, the CIT (Appeals) held that the expenses claimed were for the use of aircrafts, and therefore, it was to carry on the business of the assessee and the expenses satisfy the condition of Section 37(1) (of Income Tax Act, 1961). The CIT(Appeals) further holds that the said expenditure has been allowed in the earlier years by the Assessing Officer i.e. for the Assessment year 2004-2005, and therefore, deleted the addition of Rs.25.22,70,223/-.

(c) On further Appeal by the Revenue, the Tribunal upheld the findings of the CIT (Appeals), as the only reason for not allowing these expenses on the part of the Assessing Officer was that it was claimed only in the revised return of income. It is not the case of the Revenue that the revised return of income was invalid. Further, similar expenses when claimed for the assessment years 2007-08 and 2008-09, had been allowed by the Assessing Officer himself treating it to be revenue expenses. The Tribunal upheld the order of the CIT (Appeals).

(d) It is not disputed before us that the revised return of income was a valid return. In that view of the matter, the Assessing Officer was not justified in not considering the claim only on the ground that the claim of Rs.25.22 crores for expenditure was made only in the revised return of income. It is not disputed before us that the expenditure as claimed is eligible for deduction under Section 37(1) (of Income Tax Act, 1961) as it has been expended exclusively for the business of the Respondent-Assessee.

(e) In the above view, the question as framed does not give rise to any substantial question of law. Accordingly, not entertained.

8. Regarding Question No.15:-

(a) During the subject assessment year, the Respondent- Assessee sold five aircrafts which had been taken on hire purchase basis. The Assessing Officer held that the Respondent- Assessee was not the owner of these aircrafts and in view of the fact that the air crafts have been sold, the balance installments which were payable in the future would not be now payable. This non-payment according to the Assessing Officer resulted in a benefit to the Respondent-Assessee and the same was taxable under Section 41(1) (of Income Tax Act, 1961). Thus, made an addition of the benefit of Rs.100.52 Crores a result of the difference between sale consideration received and installment payable which is now not payable. This benefit of Rs.100.52 Crores being chargeable to tax under Section 41(1) (of Income Tax Act, 1961).

(b) Being aggrieved, the Respondent-Assessee preferred an Appeal to the CIT(Appeals). By an order dated 30th March, 2011, the CIT(Appeals) held that the Respondent-Assessee was the owner of the said aircrafts as held in the earlier assessment years and the claim of depreciation on this aircraft has also been allowed. However, on the sale of the five aircrafts, their value was also reduced from the block of assets. Thus, there was no question of any cessation or remission of liability for the purpose of Section 41(1) (of Income Tax Act, 1961) to apply. In the above view, the CIT(Appeals) deleted the addition made by the Assessing Officer as there was no occasion to invoke Section 41(1) (of Income Tax Act, 1961).

(c) On further Appeal of the Revenue, the Tribunal by the impugned order upheld the findings of the CIT(Appeals) holding that the Respondent-Assessee was the owner of these five air crafts and that depreciation has been allowed in the earlier years. The ownership of the Respondent-Assessee in respect of these aircrafts had been upheld up to the Tribunal in order passed in the earlier years. This was not the case of cessation of any liability. In the above view, the Tribunal upheld the order of the CIT(Appeals) and held that Section 41(1) (of Income Tax Act, 1961) would not apply.

9. It is very clear that for the purposes of Section 41(1) (of Income Tax Act, 1961) to apply, the allowance and/or deduction should have been allowed in an earlier assessment year and in a subsequent assessment year, the amounts so allowed was obtained either in cash or in some other manner in the subject year, then the benefit obtained is chargeable tax under Section 41(1) (of Income Tax Act, 1961) during the subsequent Assessment Year. In the present facts, the amount of Rs.361.72 Crores being installment payable in the future was never claimed as a deduction/expenditure/loss or trading liability by the Respondent-Assessee. Thus, no occasion arises for the purposes of Section 41(1) (of Income Tax Act, 1961) being invoked. Accordingly, the findings of the CIT(Appeals) and Tribunal that Section 41(1) (of Income Tax Act, 1961) is not applicable in the facts of the present case is self evident. Therefore, the proposed of question of law as formulated does not give rise to any substantial question of law and not entertained.

10. So far as Question Nos.6,7,9,12 and 13 are concerned, the learned Counsel for the Revenue very fairly states that the questions formulated herein have been dismissed in Revenue Appeal being Appeal No.1159 of 2010 on 6th May, 2014 wherein identical questions have been raised by the Revenue. Insofar as Question No.13 is concerned, we find that the impugned order dismisses the Revenue's appeal by following the binding decision of this Court in Commissioner of Income Tax V/s M/s. Echjay Forgings Pvt Ltd 251 ITR 15. No distinguishing feature in the present fact which would warrant not following the decision of this Court in Echjay Forgings(supra) has been shown to us. Accordingly, the aforesaid questions of law at Sr Nos.6,7,9,12 and 13 do not raise any substantial question of law and thus not entertained.

11. The Appeal is admitted on the substantial question of law formulated at Question Nos.2,3,4 and 8.

12. The Registry is directed to communicate a copy of this order to the Tribunal. This would enable the Tribunal to keep the papers and proceedings relating to this Appeal available so as to be produced when sought for by this Court.

13. To be heard along with Appeal No.1159 of 2010.

( B. P. COLABAWALLA, J.) (M. S. SANKLECHA, J.)

×

Similar Ripples

Questions

Jet Airways’ Tax Liability: No Cessation, No Taxation

Write your CommentSimilar Posts

Generic

- Reportdata/3186.pdf