No Incriminating Evidence, No Income Additions: Court Rules in Favor of Assessee

Full News

No Incriminating Evidence, No Income Additions: Court Rules in Favor of Assessee

No Incriminating Evidence, No Income Additions: Court Rules in Favor of Assessee

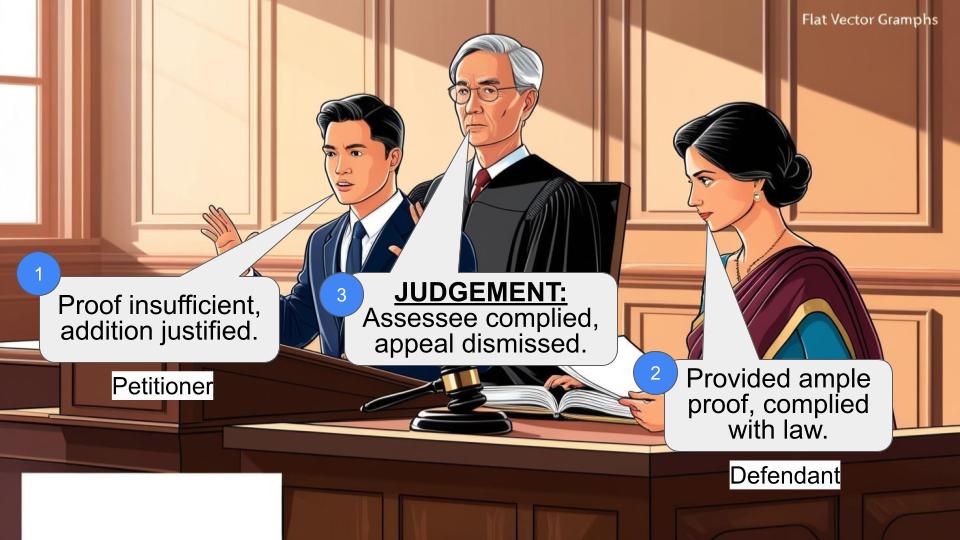

In a case involving the Principal Commissioner of Income Tax and Allied Perfumers Pvt. Ltd., the court ruled that no additions could be made to the assessee’s income as no incriminating material was found during a search. The Income Tax Appellate Tribunal (ITAT) quashed the assessment orders, emphasizing that the absence of incriminating evidence invalidated the Revenue’s claims.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax & Anr. Vs. Allied Perfumers Pvt. Ltd. & Anr. (High Court of Delhi)

ITA 391/2019

Date: 14th December 2020

Key Takeaways:

- The court emphasized that without incriminating material found during a search, additions to income cannot be justified.

- The decision reinforces the legal principle that assessments under Section 153C (of Income Tax Act, 1961) require concrete evidence.

- The ruling aligns with previous judgments, notably the case of “Commissioner of Income Tax Vs. Kabul Chawla.”

Issue

Can the Revenue make additions to an assessee’s income without any incriminating material found during a search?

Facts

- The case involves the Surya Vinayak Group, with a search conducted on March 21, 2007.

- The group was accused of taking accommodation entries by paying cash to entry operators.

- Despite a satisfaction note, no incriminating material was found against Allied Perfumers Pvt. Ltd. during the search.

- The Assessing Officer issued notices under Section 153C (of Income Tax Act, 1961), but the ITAT found no basis for income additions.

Arguments

- Revenue’s Argument: The Revenue contended that incriminating documents were found, justifying the issuance of notices under Section 153C (of Income Tax Act, 1961).

- Assessee’s Argument: The assessee argued that no incriminating material was found, making the assessment and subsequent income additions invalid.

Key Legal Precedents

- Commissioner of Income Tax Vs. Kabul Chawla (2016) 380 ITR 573 (Del.): This case established that without incriminating evidence, assessments under Section 153C (of Income Tax Act, 1961) are not valid.

- Commissioner of Income Tax- III, Pune vs. Sinhgad Technical Educational Society (2017) 84 taxmann.com 290 (SC): Reinforced the need for concrete evidence in such assessments.

Judgement

The court ruled in favor of the assessee, Allied Perfumers Pvt. Ltd., quashing the assessment orders. The ITAT found that the Revenue’s actions were based on conjectures without any incriminating material, thus making the additions unsustainable in law.

FAQs

Q1: What does this ruling mean for other similar cases?

A1: It sets a precedent that without incriminating evidence, the Revenue cannot make additions to an assessee’s income under Section 153C (of Income Tax Act, 1961).

Q2: Why was the Revenue’s argument rejected?

A2: The court found no reference to any incriminating material in the assessment order, making the Revenue’s claims baseless.

Q3: How does this affect the assessee?

A3: The assessee, Allied Perfumers Pvt. Ltd., is not liable for the additional income tax as the court ruled in their favor.

CM APPL. 17945/2019 (exemption) in ITA 391/2019

1. Allowed, subject to all just exceptions.

2. The application stands disposed of.

CM APPL. 17946/2019 (condonation of delay in re-filing) in ITA

391/2019

CM APPL. 17378/2019 (condonation of delay in re-filing) in ITA

380/2019

3. There is a delay of 296 days in re-filing the appeals. For the reasons stated in the applications, the delay is condoned.

4. The applications stand disposed of.

ITA 391/2019 & ITA 380/2019

5. The present appeals filed under Section 260A (of Income Tax Act, 1961)

[hereinafter referred to as the ‘Act’], are directed against the common order

dated 07.12.2017 passed by the Income Tax Appellate Tribunal [hereinafter

referred to as ‘ITAT’] in ITA No. 3171/DEL/2011 & ITA No.

3172/DEL/2012 along with corresponding cross objections bearing CO. No.

275/DEL/2011, & CO. No. 274/DEL/2011, for Assessment Years

[hereinafter referred to as ‘AY’] 2001-02 and AY 2002-03 respectively.

6. Considering the fact that the appeals arise from a common impugned order

and raise identical questions of law, the same are being decided by way of this

common order. The brief factual matrix giving rise to the present appeals is

that the assessee is one of the group companies of M/s Surya Vinayak

Industries Ltd. It filed the return of income [hereinafter referred to as ‘ROI’]

for AY 2001-02 & 2002-03, declaring incomes of Rs. 17,47,261/- and Rs.

36,27,660/- respectively which were duly processed under Section 143(1) (of Income Tax Act, 1961) of

the Act.

7. On 21.03.2007, a search and seizure operation was conducted, under

Section 132 (of Income Tax Act, 1961) in respect of Surya Vinayak Group of cases. The

Assessing Officer noticed that, the aforesaid group is headed by Sh. Sanjay

Jain and his brother Sh. Rajiv Jain. The main allegation against this group was

that they had taken a large number of accommodation entries in various group

companies by paying cash to various entry operators. Thus, on 29.09.2008,

after recording a satisfaction note, notice under Section 153C (of Income Tax Act, 1961) was

issued to the assessee requiring it to file the ROI in the prescribed form. In

response thereto, the assessee submitted that the previous returns declared be

deemed as the ROI in response to notice under Section 153C (of Income Tax Act, 1961).

Thereafter, assessment orders were framed under Section 153 (of Income Tax Act, 1961)/143(3) of the

Act, determining total incomes of Rs. 3,64,74,420/- and Rs. 2,28,13,060/- for

AY 2001-02 and AY 2002-03 respectively.

8. Aggrieved with the aforesaid assessments, the assessee filed an appeal

before the CIT(A) challenging the order of the Assessing Officer, on the

ground that no addition could be made in absence of any incriminating

material found during the course of search. The said appeals were allowed in

favour of the assessee on merits and the additions made by the Assessing

Officer under Section 68 (of Income Tax Act, 1961) were deleted. However, CIT(A) dismissed

the challenge as regards the issue of validity of assessment under Section

153A/143(3) of the Act.

9. Revenue then preferred an appeal before the ITAT, impugning the order of

CIT(A). In the said proceedings, Assessee filed cross objections and

contended that, the assessment order [hereinafter referred to as ‘AO’] framed

under Section 153A (of Income Tax Act, 1961)/143(3) of the Act was illegal, as consequent upon the

search action under Section 132 (of Income Tax Act, 1961), nothing incriminating was found against the

assessee, and therefore re-visiting the prior settled issues was not permissible.

The ITAT allowed the cross objections of the assessee and quashed the AO

following the decision of this Court in the case of Commissioner of Income

Tax Vs. Kabul Chawla, (2016) 380 ITR 573 (Del.). The Revenue has thus

preferred the present appeals, assailing the aforesaid impugned order of the

ITAT.

10. Mr. Abhishek Maratha, learned senior standing counsel appearing on

behalf of the Revenue contends that the ITAT has failed to take note that in

the instant cases, incriminating documents belonging to the assessee were

found and seized during the course of search under Section 132 (of Income Tax Act, 1961).

Thus, after recording of the satisfaction note, notice under Section 153C (of Income Tax Act, 1961) was

issued by the Assessing Officer. Therefore, this does not happen to be a case

wherein no documents were found during search operation. To support his

submissions, Mr. Maratha refers to paragraph 1.3 of the AO. The same is

reproduced as follows:

“1.3 After recording satisfaction note, a notice u/s 153C (of Income Tax Act, 1961) was issued on

29.09.2008 to the assessee requiring it to file the return of income in

the prescribed form.”

11. Mr. Maratha, therefore, submits that the observations of the ITAT are

incorrect and the assumption of jurisdiction by the Assessing Officer, based

on incriminating documents seized during the search, was valid and lawful.

12. We have duly considered the contentions advance by Mr. Maratha,

however, are unable to agree with him. The ITAT, after perusing the relevant

records, including the orders passed by the Revenue Authorities, observed as

follows:

10.“...We find that the additions made by the AO are beyond the scope

of section 153C (of Income Tax Act, 1961), because no incriminating

material or evidence had been found during the course of search so as

to doubt the transactions. It was noted that in the entire assessment

order, the AO has not referred to any seized material or other material

for the year under consideration having being found during the

course of search in the case of assessee, leave alone the question of

any incriminating material for the year under appeal. We also find

that the case laws cited by the Ld. CIT(DR) are not relevant to the

present case. Therefore, in our considered opinion, the action of the

AO is based upon conjectures and surmises and hence, the additions

made is not sustainable in the eyes of law, because this issue in dispute

is now no more res-integra, in view of the decision dated 29.08.2017

of the Hon'ble Supreme Court of India in the case of Commissioner

of Income Tax- III, Pune vs. Sinhgad Technical Educational Society

reported in (2017) 84 taxmann.com 290 (SC) as well as the decisions

of the Hon'ble Delhi High Court passed in the case Commissioner of

Income Tax vs. Kabul Chawla reported (2016) 380 ITR 573 (Del.) and

in the case of Principal Commissioner of Income Tax (Central) -2 vs.

Index Securities (P) Ltd.

11. Respectfully following the precedents as aforesaid, as aforesaid, we

quash the assessment made u/s.153(C) (of Income Tax Act, 1961)/143(3) of the I.T. Act, 1961 and

decide the legal issue in favour of the Assessee and accordingly, allow

the Cross Objection filed by the assessee.

12. Following the consistent view taken in the assessment year 2001-02

in the Assessee’s Cross objection, as aforesaid, th another Cross

objection filed by the Assessee relating to assessment years 2002-03

also stand allowed.”

( Emphasis supplied)

13. Upon reading of the aforesaid extracted portion of the impugned order,

it is clearly discernable that the ITAT has given a finding of fact that the

assessments make no reference to the seized material or any other material for

the years under consideration, that was found during the course of search, in

the case of the assessee. Mr. Maratha is also unable to point out any

incriminating material related to the assessee which could justify the action of

the Revenue. Merely because a satisfaction note has been recorded, cannot

lead us to reach to this conclusion, especially when the Revenue has not laid

any foundation to support their contention. In the factual background as

explained above, the assumption of jurisdiction under Section 153C (of Income Tax Act, 1961) cannot be

sustained in view of the decision of this Court in the case of Kabul Chawla

(Supra).

14. In view of the foregoing, we find no question of law, much less substantial

question of law, that calls for a consideration. Accordingly, the present

appeals are dismissed.

SANJEEV NARULA, J.

MANMOHAN, J.

DECEMBER 14, 2020

×

Similar Ripples

Questions

No Incriminating Evidence, No Income Additions: Court Rules in Favor of Assessee

Write your CommentSimilar Posts

Generic

- Reportdata/6400.pdf