Penalty on Assessee Overturned: No Concealment Found

Full News

Penalty on Assessee Overturned: No Concealment Found

Penalty on Assessee Overturned: No Concealment Found

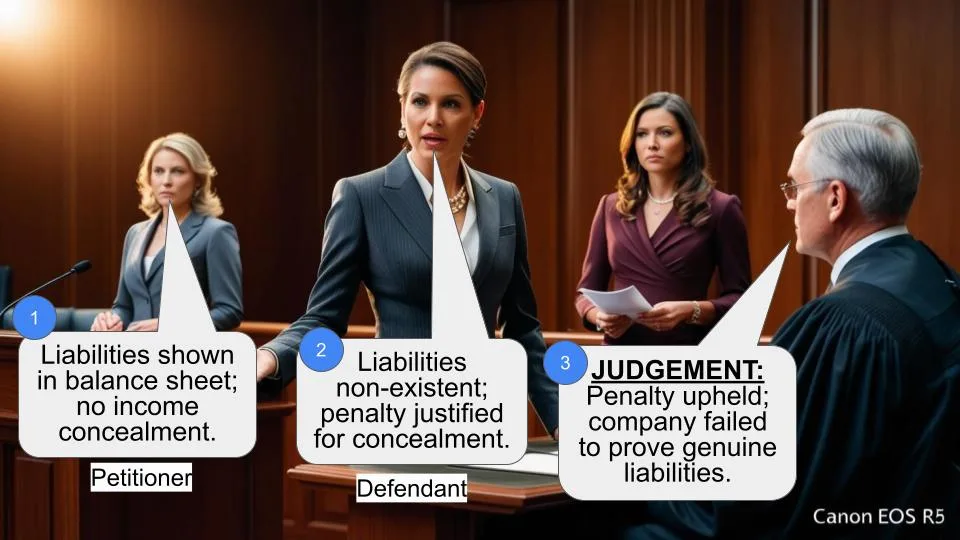

The case involves the Commissioner of Income Tax and Dalima Dyechem Industries Ltd., where the central issue was whether a penalty under Section 271(1)(c) (of Income Tax Act, 1961) was justified. The court found that there was no concealment or furnishing of inaccurate particulars by the assessee, leading to the dismissal of the penalty.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Dalima Dyechem Industries Ltd. (High Court of Bombay)

Income Tax Appeal No. 1396 of 2013

Date: 6th July 2015

Key Takeaways:

- No Penalty Without Concealment: The court emphasized that penalties under Section 271(1)(c) (of Income Tax Act, 1961) require clear evidence of concealment or inaccurate particulars.

- Strict Interpretation: The decision reinforced the need for strict interpretation of tax laws, as highlighted in the Apex Court's decision in Reliance Petroproducts.

- Bonafide Actions: The court recognized the assessee's actions as bonafide, given the legal interpretations and previous tribunal decisions in their favor.

Issue

Was the penalty under Section 271(1)(c) (of Income Tax Act, 1961) justified when there was no evidence of concealment or furnishing of inaccurate particulars by the assessee?

Facts

- The assessee, Dalima Dyechem Industries Ltd., was penalized by the Assessing Officer for allegedly concealing income and furnishing inaccurate particulars.

- The penalty was based on disallowed interest deductions related to interest-free advances to sister concerns.

- The assessee contested the penalty, arguing there was no malafide intention and all facts were disclosed.

Arguments

- Revenue's Argument: The Revenue argued that the assessee concealed income and misrepresented facts, justifying the penalty.

- Assessee's Argument: The assessee contended that their actions were bonafide, supported by legal interpretations and tribunal decisions, and that no notice was served before imposing the penalty.

Key Legal Precedents

- Reliance Petroproducts Pvt. Ltd. [2010] 322 ITR 158 (SC): The court applied the principle that incorrect claims in law do not equate to furnishing inaccurate particulars.

- S.A. Builders Ltd. v. Commissioner of Income Tax (Appeals): Referenced for the principle of commercial expediency in interest deductions.

Judgement

The court upheld the decision of the Commissioner (Appeals) and the Tribunal, which found no concealment or furnishing of inaccurate particulars by the assessee. The penalty was deemed unjustified, and the appeal by the Revenue was dismissed.

FAQs

Q1: What does Section 271(1)(c) (of Income Tax Act, 1961) entail?

A1: It allows for penalties if a person is found to have concealed income or furnished inaccurate particulars.

Q2: Why was the penalty overturned?

A2: The court found no evidence of concealment or inaccurate particulars, and the assessee's actions were considered bonafide.

Q3: What was the significance of the Reliance Petroproducts case?

A3: It established that making an incorrect claim in law does not automatically mean furnishing inaccurate particulars, requiring strict interpretation of tax laws.

Q4: What does this mean for the assessee?

A4: The assessee is not liable for the penalty, as their actions were deemed within legal bounds and not intentionally misleading.

1. By this appeal under Section 260A (of Income Tax Act, 1961), the Revenue seeks to challenge the order passed by the Income Tax Appellate Tribunal, Mumbai dated 21 November 2012. By the impugned order, the appeal filed by the Revenue before the Tribunal for the Assessment Year 20032004 was dismissed. The present Appeal relates to Assessment Year 2003-2004.

2. The Respondent Assessee, in it's accounts, had shown borrowed funds and interest free advances to it's sister concerns. The Assessing Officer disallowed the proportionate interest out of the interest paid for the interest free advances given to the sister concern. The Assessee challenged this order before of Income Tax (Appeals)(Commissioner), who upheld the same. Thereafter the Assessee filed an appeal before the Income Tax Appellate Tribunal. The Tribunal set aside the orders and restored the matter to the file on Assessing Officer for reexamination of the deductibility. The Tribunal relied on the decision of the Apex Court in S.A. Builders Ltd. v. Commissioner of Income Tax (Appeals) and another reported in [2007] 288 ITR 1(SC).

3. Upon remand, the Assessing Officer again disallowed the

proportionate interest holding that the Assessee had borrowed

funds of which interest liability had been incurred. The Assessing

Officer also levied penalty holding that the Assessee concealed it's

income by furnishing inaccurate particulars. The Assessee

thereafter filed an appeal before the Commissioner. The levy of

penalty was challenged on the ground that Assessee had no

malafide intention to evade any tax and all the facts and details

were placed on record. The Commissioner by the order dated 10

June 2011 allowed the appeal. The Commissioner came to the

conclusion that merely because the claim made by an Assessee was

disallowed, penalty cannot be levied, unless it is demonstrated that

the Assessee had any malafide intention.

4. The Revenue thereafter filed an appeal to the Income Tax

Appellate Tribunal. The Tribunal accepted the reasoning of the

Commissioner that the penalty cannot be levied merely because

the claim of the Assessee is found to be incorrect. The

Commissioner and the Tribunal relied upon the decision of the

Apex Court in the case of Commissioner of IncomeTax Vs

Reliance Petroproducts Pvt. Ltd. [2010] 322 ITR 158 (SC) to

hold that in the present facts no penalty is impossible.

5. Being aggrieved Revenue has approached this Court by way

of the present appeal.

6. Mr.Chhotaray, learned counsel for the Revenue contended

that Assessee had concealed its income and had misrepresented

the facts. He submitted that the Assessee did not even bother to

furnish explanation and penalty was rightly imposed. He submitted

that the Tribunal mechanically applied the decision of the Apex

Court in the case of Reliance Petroproducts (supra) without

appreciating the factual aspects in which the decision was

rendered. He submitted that the decision of the Apex Court has not

laid down an absolute proposition as held by the Tribunal and if

such interpretation is accepted there will be virtually no case where

a penalty can be levied. He submitted that in the case of Reliance

Petroproducts (supra), the Assessee therein had given an

explanation, which is not the present case. He submitted that the

Delhi High Court in the case of Commissioner of Income Tax Vs

Zoom Communication P. Ltd. [2010] 327 ITR 510 (Delhi),

reversed the order of Tribunal deleting the penalty relying on the

decision of the Apex Court in Reliance Petroproducts(supra), by

reading the decision of the Apex Court in the proper perspective.

Mr.Chhotaray therefore submitted that the questions of law that

would arise in this Appeal are, firstly: whether on facts and

circumstances of the case and in law the Tribunal was justified in

upholding the order of Commissioner (Appeals) deleting the

penalty imposed by the Assessing Officer, and secondly : whether

the Tribunal was right in law in deleting the penalty and upholding

the order of the Commissioner of IncomeTax ignoring that

Assessee had wilfully claimed deductions in respect of interest on

borrowed funds which were diverted to sister concern and not for

the business.

7. Mr.Atul Jasani, learned counsel for the Respondent Assessee

submitted that no notice was issued to the Assessee before

imposing the penalty and this ground was taken by the Assessee in

the appeal. He submitted that, both the Assessee and it's sister

concerns, were loss making units and the Assessee bonafide felt

that the Assessee was covered by the decision of the Apex Court in

the case of S.A Developers (supra). He submitted that the

Assessee had contested the issue upto the Tribunal and had also

succeeded in as much as the matter was remanded back to the

Assessing Officer. It is therefore submitted that no penalty could be

levied as the actions of the Assessee were bonafide.

8. Section 271(1)(c) (of Income Tax Act, 1961) lays down that the penalty can

be imposed if the authority is satisfied that any person has

concealed particulars of his income or furnished inaccurate

particulars of such income. The Apex Court in Reliance

Petroproducts (supra) applied the test of strict interpretation. It

held that the plain language of the provision shows that, in order

to be covered by this provision there has to be concealment and

that the assessee must have furnished inaccurate particulars. The

Apex Court held that by no stretch of imagination making an

incorrect claim in law, would amount to furnishing inaccurate

particulars.

9. Thus, above conditions under Section 271(1)(c) (of Income Tax Act, 1961) must exist

before the penalty can be imposed. Mr.Chhotaray tried to widen

the scope of the appeal by submitting that the decision of the Apex

Court should be interpreted in such a manner that there is no scope

of misuse especially since minuscule number of cases are picked up

for scrutiny. Because small number of cases are picked up for

scrutiny does not mean that rigors of the provision are diluted.

Whether a particular person has concealed income or has

deliberately furnished inaccurate particulars, would depend on

facts of each case. In the present case we are concerned only with

the finding that there has been no concealment and furnishing of

incorrect particulars by the present assessee.

10. Though the Assessee had given interest free advances to it's

sister concerns and that it was disallowed by the Assessing Officer,

the Assessee had challenged the same by instituting the

proceedings which were taken up to the Tribunal. The Tribunal

had set aside the order of the Assessing Officer and restored the

same back to the Assessing Officer. Therefore, the interpretation

placed by Assessee on the provisions of law, while taking the

actions in question, cannot be considered to be dishonest, malafide

and amounting concealment of facts. Even the Assessing Officer in

the order imposing penalty has noted that commercial expediency

was not proved beyond doubt. The Assessing Officer while

imposing penalty has not rendered a conclusive finding that there

was an active concealment or deliberate furnishing of inaccurate

particulars. These parameters had to be fulfilled before imposing

penalty on the Assessee.

11. The case of Commissioner of Income Tax Vs.Zoom

Communications P.Ltd. [2010] 327 ITR 510 (Delhi) relied upon

by Mr.Chhotaray is clearly distinguishable on facts. In that case

the Assessee had conceded before Assessing Officer that it's action

of claiming revenue deductions was not correct at all. It was not the

case of the Assessee therein, throughout the proceedings, that the

deductions carried out by the Assessee was a debatable issue. The

Delhi High Court noted that even before it the Assessee could not

explain the circumstances and it's conduct.

12. In the present case therefore, when the Assessee had bonafide

pleaded that it was covered by a particular position of law and that

one authority i.e. the Tribunal had passed certain orders in it's

favour during the assessment proceedings, it could not be said that

the Assessee fell within the ambit of Section 271(1)(c) (of Income Tax Act, 1961). The

assertion of the Assessee that it was not served with a notice and

therefore cannot be blamed for not filing a reply, has gone

uncontroverted. This being the position we do not find any

perversity with the decision of the Commissioner (Appeals) and the

Tribunal in deleting the penalty imposed by the Assessing Officer. In

any case this is a possible view of the matter upon appreciating the

evidence. In the circumstances, both the grounds urged by the

Revenue cannot be termed as substantial questions of law.

The Appeal is dismissed.

(N.M.Jamdar, J.) (M.S.Sanklecha, J.)

×

Similar Ripples

Questions

Penalty on Assessee Overturned: No Concealment Found

Write your CommentSimilar Posts

Generic

- Reportdata/3652.pdf