Pre-2019 Stock-to-Investment Conversion Taxed as Capital Gain, Not Business Inc…

Full News

Pre-2019 Stock-to-Investment Conversion Taxed as Capital Gain, Not Business Income

Pre-2019 Stock-to-Investment Conversion Taxed as Capital Gain, Not Business Income

This case involves Kemfin Services Pvt. Ltd. (the assessee) appealing against the Income Tax Department's decision to treat their income from the sale of shares, which were converted from stock-in-trade to investments, as business income rather than capital gains. The High Court ruled in favor of the assessee, stating that prior to the 2019 amendment, such income should be treated as capital gains.

Get the full picture - access the original judgement of the court order here

Case Name:

Kemfin Services Pvt Ltd. Vs Assistant Commissioner of Income Tax (High Court of Karnataka)

I.T.A. No.149 of 2011

Date: 11th June 2020

Key Takeaways:

1. Prior to April 1, 2019, income from the sale of shares converted from stock-in-trade to investments should be treated as capital gains, not business income.

2. The court emphasized the importance of strictly interpreting tax laws.

3. This ruling highlights the significance of legislative amendments in tax treatment.

Issue:

Whether the income arising from the sale of shares held as capital assets after their conversion from stock-in-trade should be treated as business income or capital gains, prior to the 2019 amendment of the Income Tax Act?

Facts:

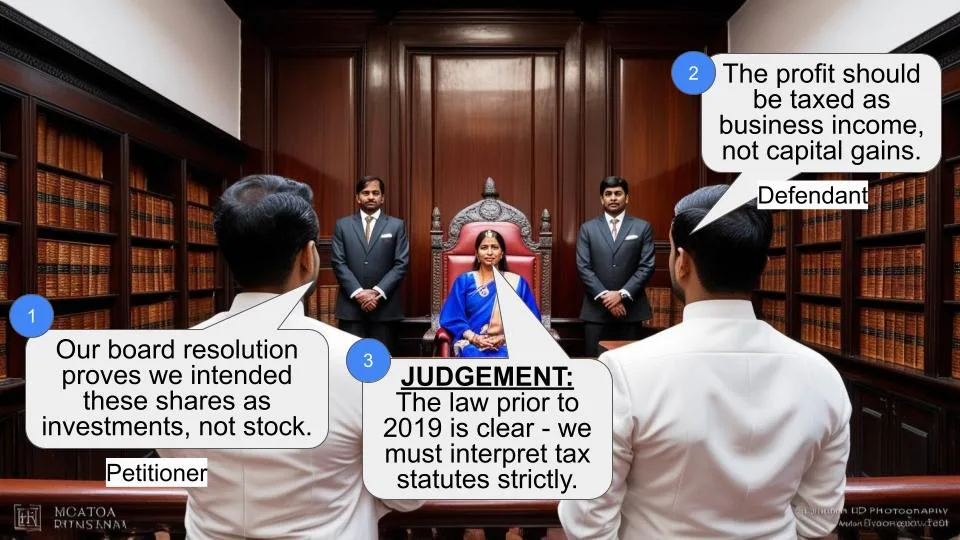

1. Kemfin Services Pvt. Ltd., a non-banking financial corporation, passed a board resolution to stop trading activities and convert stock-in-trade worth Rs.1,30,98,529/- into investments on April 1, 2004.

2. The assessee filed tax returns for the Assessment Year 2005-06, declaring a total income of Rs.38,03,595/-.

3. The Assessing Officer treated the transactions as business income rather than capital gains.

4. The case went through appeals at various levels before reaching the High Court.

Arguments:

Assessee's arguments:

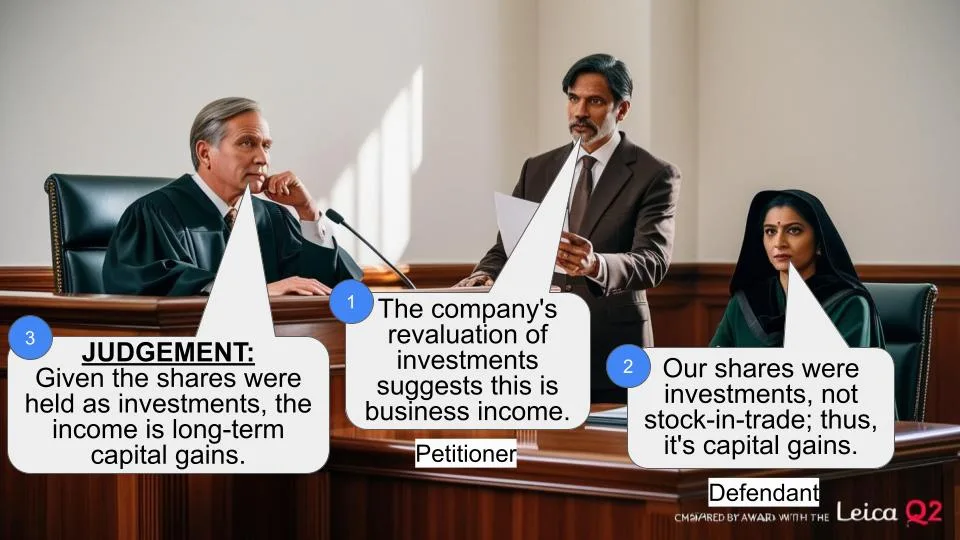

1. The profits from selling converted shares should be assessed as capital gains, not business profits.

2. No income arises from the mere conversion of stock-in-trade to capital assets.

3. The cost at the time of actual acquisition should be considered the cost of acquisition.

Revenue's arguments:

1. Capital gains should be calculated up to the date of conversion into stock-in-trade.

2. The difference between the sale value and stock-in-trade value should be considered business income.

3. Provisions of Section 45(2) (of Income Tax Act, 1961) should be taken into account.

Key Legal Precedents:

1. SIR KIKABHAI PREMCHAND VS. CIT (1953) 24 ITR 506 (SC):

Held that it's artificial to separate a business from its owner and create fictional profits.

2. SARASWATI SUGAR MILLS VS. HARYANA STATE BOARD (1992) 1 SCC 418: Established that taxing statutes must be strictly construed.

3. Various High Court decisions (e.g., PAVITRA COMMERCIAL LTD., YATISH TRADING CO. PVT. LTD., EXPRESS SECURITIES PVT. LTD.) supporting the treatment of such income as capital gains prior to the 2019 amendment.

Judgement:

The High Court ruled in favor of the assessee, stating that:

1. Prior to the amendment effective from April 1, 2019, there was no provision to tax the conversion of stock-in-trade into capital assets.

2. The income arising from the sale of shares held as capital assets after conversion from stock-in-trade should be treated as capital gains, not business income.

3. The tribunal erred in treating this income as business income.

FAQs:

Q1: What was the main issue in this case?

A1: The main issue was whether income from selling shares converted from stock-in-trade to investments should be taxed as business income or capital gains, prior to the 2019 amendment.

Q2: When did the amendment changing this tax treatment come into effect?

A2: The amendment came into effect on April 1, 2019.

Q3: Why did the court rule in favor of the assessee?

A3: The court ruled in favor of the assessee because, prior to the 2019 amendment, there was no specific provision in the Income Tax Act to tax such conversions as business income.

Q4: What principle of statutory interpretation did the court apply?

A4: The court applied the principle that taxing statutes must be strictly construed, meaning that without clear words for taxation, a subject cannot be taxed.

Q5: Does this ruling apply to current cases?

A5: No, this ruling applies to cases prior to April 1, 2019. After this date, the amended law would apply.

1. These appeals under Section 260A (of Income Tax Act, 1961) (hereinafter referred to as the Act for short) has been preferred by the assessee. The subject matter of ITA No.149/2011 pertains to Assessment year 2004-05, whereas, subject matter of I.T.A.No.70/2011 relates to Assessment year 2005-06. Since, common question of law arise for consideration in these appeals, they were heard analogously and are being decided by this common judgment. The appeals were admitted by a bench of this Court vide order dated 03.08.2011 on following substantial question of law:

(i) Whether on the facts and in the circumstances of the case, the Hon’ble ITAT was right in law in holding that the income arising on sale of shares held as capital asset after conversion from stock in trade as business income and not as capital gains?

2. For the facility of reference, facts from I.T.A.No.70/2011 are being referred to. The assessee is a non banking financial corporation engaged in the activity of investment in shares. The Board of the assessee passed a resolution to stop its trading activities in shares and securities under the portfolio management scheme and to convert the stock in trade worth Rs.1,30,98,529/- into investment on 01.04.2004. The financial statements were adopted and signed by the Board of Directors and the statutory auditors for Assessment year 2005-06. The assessee filed its return of income for Assessment year 2005-06 on 26.10.2005 declaring total income of Rs.38,03,595/-. The case of the appellant was selected for scrutiny and notice under Section 143(2) (of Income Tax Act, 1961) was issued. The assessee furnished the details asked for by the assessing officer.

An order of assessment was passed on 31.12.2007 and it was inter alia held that mere interchange of heads in books of accounts as investment or stock in trade does not alter the nature of transaction and the transactions of the assessee fall within the ambit of business income and not short term capital gain. Thus, the transactions, were treated as business income and an order of assessment was passed. Being aggrieved, the assessee filed an appeal. The Commissioner of Income Tax (Appeals) vide order dated 18.12.2009 inter alia held that the shares had to be considered as stocks in trade and income from sale of shares has to be treated as income under the head business. It was further held that the assessee is entitled to relief of Rs.16,215/- towards securities transaction tax under Section 88E (of Income Tax Act, 1961) and the assessing officer was directed to grant the relief after verification. Accordingly, the appeal was partly allowed.

3. Being aggrieved, the assessee filed an appeal before the Income Tax Appellate Tribunal. The tribunal vide order dated 07.10.2010 inter alia held that assessee had acquired certain shares under portfolio management scheme and those shares were treated by the assessee and accepted by the department as stock in trade for the Assessment years 2003-04 and 2004- 05. It was further held that assessee had changed the character of its asset from stock in trade to investments. It was further held that surplus had arisen in the course of conversion of aforesaid shares and therefore, stock in trade is a business asset and any income arising on account of stock in trade is obviously a business income. It was also held that income always arises from an existing source and not from a potential source. In the result, the appeal preferred by the assessee was dismissed. Being aggrieved, the assessee is in appeal before us.

4. Learned counsel for the assessee submitted that the assessee converted stock in trade to shares and sold the same and therefore, the profits arising therefrom have to be assessed as capital gain and not as business profit in the absence of any provision in the Act at the relevant time. It is further submitted that the tribunal ought to have appreciated that the surplus did not arise due to conversion. It is also submitted that Section 2(14) (of Income Tax Act, 1961), which defines the expression ‘capital asset’ excludes stock in trade. Attention of this court has also been invited to the memorandum to Finance Bill, 2018 in support of the submission that Section 45 (of Income Tax Act, 1961) provides for capital gains arising from conversion of capital asset into stock in trade. However, it does not provide for levy of tax in cases where stock in trade is converted into or treated as capital asset. It is pointed out that the provisions of the Act were amended. It is further submitted that the tribunal ought to have appreciated that from conversion of stock in trade to capital asset, no income has resulted as person cannot be said to have transaction with ones own self and there cannot be any actual profit or loss where no third party is involved. It is also submitted that assessee had converted stock in trade of shares into investment during Assessment year 2005-06. The tribunal by an order dated 07.06.2016 passed in ITA Nos.1450 and 1451 (B)/2015 decided on 07.06.2016 held that shares held by the appellant as investments is liable to be taxed as capital gain and not as business income. The aforesaid order was not assailed by the revenue in an appeal before this court and therefore, the aforesaid issue has attained finality. It is also submitted that sale of shares held in stock in trade converted into investments being capital gains is not a business income and the determination whether the property is a capital asset or not has to be made only at the time of transfer and not at any other point of time and therefore, the cost on the date of actual acquisition must be taken as cost of acquisition. In support of aforesaid submissions, reliance has been placed on decisions in ‘CIT VS. DHANUKA & SONS’, (1980) 124 ITR 24 (CAL), ‘SIR KIKABHAI PREMCHAND VS. CIT’, (1953) 24 ITR 506 (SC), ‘KEMFIN SERVICES PVT. LTD. VS. ACIT’, ITA NOS.1450 & 1451(B)/2015, ‘CIT VS. BANGALORE DEVELOPERS PVT. LTD.,’, (2017) 392 ITR 379 (KAR), ‘PR.CIT VS. PAVITRA COMMERCIAL LTD.’, (2018) 402 ITR 66 (DEL), ‘CIT VS. YATISH TRADING CO. PVT LTD.,’, 2013-TIOL-117-HC-MUM- IT, ‘CIT VS. EXPRESS SECURITIES PVT. LTD.,’, 2013-TIOL-862-HC-DEL-IT, ‘DEEPLOK FINANCIAL SERVICES LTD VS. CIT’, (2017) 393 ITR 395 (CAL), ‘ADITYA MEDISALES LTD. VS. DCIT’, (2016) 242 TAXMAN 228 (GUJ), ‘ CIT VS. JANNHAVI INVESTMENT (P,) LTD.’, (2008) 304 ITR 276 (BOM), ‘RANCHOD BHAI BHAIJIBHAI PATEL VS. CIT’, (1971) ITR 446 (GUJ), ‘M.VENKATESAN VS. CIT’, (1983) 144 ITR 886 (MAD), ‘CIT VS. SMT.M.SUIBAIDA BEEVI’, (1986) 60 ITR 557 (KERALA), ‘CIT VS. VISHWANATH’, (1993) 201 ITR 920 (ALL).

5. On the other hand, learned counsel for the revenue submitted that when stock in trade is converted into shares and is sold, the capital gains have to be completed up to the date of conversion into stock in trade and for the period thereafter the difference between value of sale and stock in trade has to be considered as business income and therefore, the order of the tribunal needs modification to the aforesaid extent. It is urged that provisions of Section 45(2) (of Income Tax Act, 1961) have to be taken into account. In support of aforesaid submissions, reliance has been placed on the decisions in ‘COMMISSIONER OF INCOME-TAX, CHENNAI VS. ESSORPE HOLDINGS (P.) LTD.’, (2017) 83 TAXMANN.COM 280 (MADRAS) and ‘COMMISSIONER OF INCOME-TAX, DELHI VS. ABHINANDAN INVESTMENT LTD.’, (2015) 63 TAXMANN.COM 263 (DELHI). It is also submitted that in PAVITHRA COMMERCIAL LTD., supra and YATISH TRADING CO. LTD., it was found that no questions of law arise for consideration. Therefore, the aforesaid decisions have no value as precedents.

6. We have considered the submissions made on both the sides and have perused the record. Admittedly, in the instant case, the assessee had converted stock in trade into investments. The Supreme Court in case of SIR KIKABHAI PREMCHAND supra has held that it is wholly unreal and artificial to separate the business from its owner and treat them as they were separate entities trading with each other and then by means of a fictional sale introduce a fictional profit which include and in fact, is non existent. It has further been held that a person cannot be supposed to sell some thing to himself and making a profit out of the transaction, which on the face of it is not only absurd but against all canons of mercantile and income tax law. The aforesaid decision has been followed by various high courts till the provisions of the Act were amended with effect from 01.04.2019. It is equally well settled legal proposition that income from sale of shares held as investment converted from stock in trade is to be treated as capital gain and not as business income.

7. It is well settled principle of statutory interpretation that a taxing statute has to be strictly construed. It has been held that the subject is not to be taxed without clear words for that purpose and also that every Act of parliament must be read according to the natural construction of its words. [SEE: ‘SARASWATI SUGAR MILLS VS. HARYANA STATE BOARD’, (1992) 1 SCC 418]. It has further been held that if a person sought to be taxed comes within the letter of law he must be taxed, however, great hardship may appear to the judicial mind to be. [SEE: PRINCIPLES OF STATUTORY INTERPRETATION BY JUSTICE G.P.SINGH, PAGE 879, 14TH EDITION].

8. In the instant case, the relevant extract of memorandum to Finance Bill, 2018 reads as under:

“Section 45 (of Income Tax Act, 1961), inter alia provides that capital gains arising from a conversion of capital asset into stock in trade shall be chargeable to tax. However, in cases where the stock in trade is converted into, or treated as capital asset, the existing law does not provide for its taxability.

In order to provide symmetrical treatment and discourage the practice of deferring the tax payment by converting the investory into capital asset, it is proposed to amend the provisions of –“

9. Thus, it is evident prior to introduction of Finance Bill, 2018 by which provisions of the Act have been amended to provide for taxability of in cases where stock in trade is converted into capital asset, there was no provision to tax the same. In the absence of any provision in the Act, the transaction in question could not have been subjected to tax. Prior to amendment of the Act, which came into force with effect from 01.04.2019, the income arising on sale of shares held as capital asset after their conversion from stock in trade was treated as capital gains as has been held by various high courts viz., in the cases of PAVITRA COMMERICAL LTD., YATISH CO. PVT. LTD., EXPRESS SECURITIES PVT. LTD., DEEPLOK FINANCIAL SERVICES LTD., ADITYA MEDI SALES LTD. and JANNHAVI INVESTMENT PVT. LTD., supra. We agree with the view taken by various high courts on this issue.

10. In view of the preceding analysis, the tribunal erred in treating the income arising on sale of shares held as capital asset after conversion from stock in trade as business income. The substantial question of law framed in the appeals is answered in favour of the assessee and against the revenue. The order of the tribunal is quashed.

In the result, the appeal is allowed.

Sd/-

JUDGE

Sd/-

JUDGE

×

Similar Ripples

Questions

Pre-2019 Stock-to-Investment Conversion Taxed as Capital Gain, Not Business Income

Write your CommentSimilar Posts

Generic

- Reportdata/5952.pdf