"Capital Gains or Business Income? Court Rules in Favor of Long-Term Capital Ga…

Full News

"Capital Gains or Business Income? Court Rules in Favor of Long-Term Capital Gains"

"Capital Gains or Business Income? Court Rules in Favor of Long-Term Capital Gains"

This case involves a dispute between the Commissioner of Income Tax and HMA Data Systems (P) Ltd. The main issue was whether the income from the sale of shares should be taxed as capital gains or business income. The court ruled in favor of treating the income as long-term capital gains, affirming the decision of the lower appellate authorities.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. HMA Data Systems (P) Ltd. (High Court of Karnataka)

ITA No. 700 of 2009 C/w ITA No. 684 of 2009

Date: 26th June 2015

Key Takeaways:

- The court affirmed that the income from the sale of shares should be treated as long-term capital gains, not business income.

- The decision highlights the importance of how investments are recorded and treated in financial statements.

- The ruling also addressed the treatment of professional charges and travel expenses related to the sale of shares.

Issue

Should the income from the sale of 50,000 shares be taxed as long-term capital gains or as business income?

Facts

- HMA Data Systems (P) Ltd. sold 50,000 shares of Diebold HMA Pvt. Ltd. for a significant profit.

- The company declared this profit as long-term capital gains in its tax return.

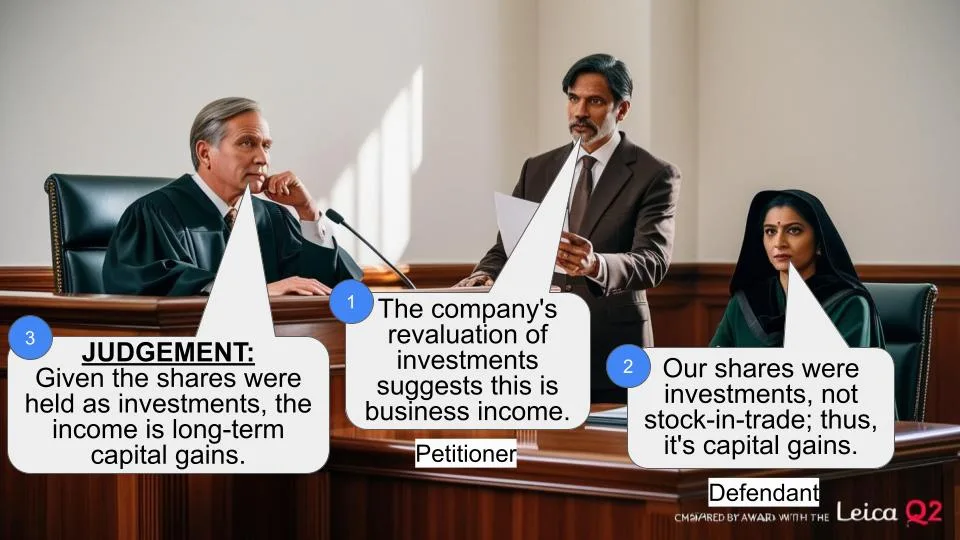

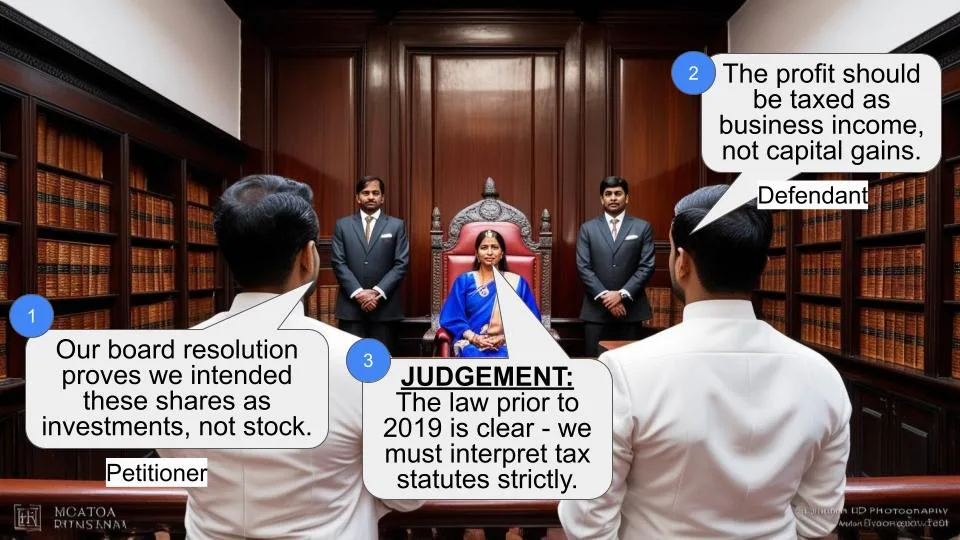

- The Assessing Officer disagreed, treating the income as business income due to the company's history of revaluing investments.

- The case was appealed, and the appellate authorities ruled in favor of the company, treating the income as capital gains.

Arguments

- For the Revenue: The income should be treated as business income because the company regularly revalued its investments, indicating a business activity.

- For the Assessee: The income should be treated as capital gains because the shares were held as investments, not as stock-in-trade.

Key Legal Precedents

The judgment did not explicitly cite specific past cases but focused on the interpretation of tax laws regarding the classification of income from the sale of shares.

Judgement

The court ruled in favor of HMA Data Systems (P) Ltd., affirming the decision of the lower appellate authorities. The income from the sale of shares was to be treated as long-term capital gains. The court also upheld the allowance of professional charges related to the sale of shares as part of the capital gains computation.

FAQs

Q1: Why was the income treated as capital gains and not business income?

A1: The court found that the shares were held as investments, not as part of a business activity, which justified treating the income as capital gains.

Q2: What was the significance of the professional charges in this case?

A2: The professional charges were related to the sale of shares and were allowed as deductions in computing the capital gains, not as business expenses.

Q3: How does this case impact future tax assessments?

A3: This case reinforces the importance of how companies classify and report their investments and related income, impacting how such income is taxed.

1. These two appeals have been preferred by the Revenue and the assessee respectively being aggrieved by the order passed by Income Tax Appellate Tribunal, Bangalore Bench in ITA No.1154/Bang/2009 dated 29.05.2009 whereunder the Tribunal has held:

(i) income earned on the sale of 50,000 equity shares of M/s.Diebold HMA Pvt. Ltd., was liable to be brought to tax under the head “Capital gains” and not as “income from business” as held by the assessing officer;

(ii) travel expenditure, professional charges and other expenses in connection with sale of said shares had nexus to such sale; and

(iii) amount paid towards legal charges in respect of such sale was allowed by the CIT(A) was correct.

2. This Court has admitted both the appeals on 24.09.2010 and 27.10.2009 respectively to consider the following substantial questions of law:

1. ITA 700/2009:

(i) “Whether the Appellate Authorities

were correct in holding that the

income of Rs.21,55,47,800/- earned

on the sale of 50,000 equity shares

of M/s.Diebold HMA P. Ltd., was

liable to be brought to tax under the

head “capital gains” and not “income

from business” as held by the

Assessing Officer despite the

assessee increasing the profit and

loss account in respect of the value

of the shares for each assessment

year from the date of purchase i.e.,

assessment year 1992-93?

(ii) Whether the Appellate Authorities

were correct in not taking into

consideration the fact that the

assessee had claimed travel

expenditure, professional charges

and other expenses in connection

with sale of M/s.Diebold HMA P.

Ltd., shares and especially when the

assessee had no other business

income during the current

assessment year?

(iii) Whether the sum of Rs.24,93,800/-

paid to M/s.Amarchand Mangaldas

towards legal charges in respect of

sale of M/s.Diebold HMA P. Ltd.,

shares is liable to be deducted from

the sale value when computing

capital gains tax when the actual

payment accrued and was paid in

the earlier assessment year 2003-04

and allowing the claim during the

current assessment year would

distort the profits of the current

year?”

2. ITA 684/2009:

(i) “Whether the Tribunal was justified

in law in holding that the appellant

is not entitled to the deduction on

account of technical support charges

on the facts and circumstance of the

case?

(ii) Whether the Tribunal was justified in

law disallowing the expenditure

relating to Travel by the executive for

the purpose of business on the facts

and circumstance of the case?

(iii) Whether the Tribunal was justified in

holding that accrual of income is the

precondition for allowing expenditure

on the facts and circumstances of

the case?”

3. Facts in brief which has led to filing of these appeals are as under:

Assessee is a private limited company

engaged in the development of software as well as

manufacture and sale of equipments and maintenance.

For the assessment year 2004-05 return of income

came to be filed declaring its total income at

`3,70,66,590/-. The assessing officer after issuing

notice under section 143(2) (of Income Tax Act, 1961) after selecting the return for

scrutiny has proceeded to frame the assessment order

under Section 143(3) (of Income Tax Act, 1961) by order dated 22.12.2006,

whereunder disallowances to the tune of `2,67,85,610/-

was made. During the previous year relevant to the

assessment year, assessee sold 50,000 shares of

M/s.Diebold HMA Pvt. Ltd., said to have been acquired

by it during the year 1992-93 for a total consideration of

`21,55,47,800/- and declared a long term capital gain

of `20,51,66,634/- in its return of income. However,

the assessee was denied the benefit of long term capital

gain arising from such sale of shares on the ground that

the assessee had been debiting its profit and loss

account with decrease or increase in the value of

investments and as such it should be treated as `income

from business’. It was also noticed by the assessing

officer that professional charges of `1,19,09,768/-

debited to profit and loss account is to be disallowed to

an extent of `24,93,800/- on the ground that such

professional charges related to sale of shares and the

payment relating to this expenditure had been made in

the year 2002-03 but accounted to in the assessment

year 2004-05. Hence, assessing officer came to a

conclusion that payment was made outside the books of

accounts and accordingly disallowed the claim for

deduction to the extent indicated hereinabove.

However, CIT (A) held such payment had been reflected

as advance (pre-paid professional-charges) in that year

and it cannot be allowed while computing business

income, but it has to be allowed in computing the long

term capital gains, since assessee had incurred

expenditure in sale of Diebold HMA shares and same is

to be allowed in computing long term capital gains as

claimed by assessee and his finding came to be affirmed

by Tribunal. Further, assessing officer also disallowed a

sum of ` 18,55,756/- claimed by the assessee as

expenditure relating to abroad travel by the company’s

Managing Director and his wife on the ground that there

was no business activity justifying their foreign travel

for business purposes. A sum of ` 94,74,184/- claimed

by the appellant as `technical support charges’ paid

towards promotion of products and services in North

America was also disallowed on the ground that the

agreement relating to this activity had not been put into

practice which came to be affirmed by CIT (A) and

Tribunal.

4. Thus, revenue being aggrieved by the order

of the Tribunal which affirmed the finding of CIT(A)

insofar as treating the receipt of the amount by the

assessee insofar as sale of shares as ‘capital asset’ and

allowance of the legal fee paid by the assessee as

professional fee to be allowed while computing the long

term capital gains as claimed by the assessee which

finding has been affirmed by the Tribunal has been

questioned by the revenue in ITA No.700/2009. The

assessee being aggrieved by the finding of the assessing

officer who disallowed the expenditure relating to

foreign travel by the Managing Director and his wife and

disallowing the amount paid by the assessee as

‘technical support charges’ to professionals on the

ground that such activity had not been put into practice

came to be affirmed both by the CIT (A) as well as

Tribunal and as such, the assessee has preferred ITA

No.684/2009.

5. We have heard the learned advocates

appearing for the parties and perused the orders passed

by the Tribunal, CIT(A) and the assessing officer.

6. It is the contention of Sri K.V.Aravind,

learned Advocate appearing for the revenue that the

appellate authorities committed an error in holding that

income earned by the assessee on sale of 50,000 equity

shares to be brought under the head “Capital Gains”

and not “Income from Business” though assessee had

increased the profit and loss account in respect of the

value of shares for each assessment year from the date

of purchase of shares namely, from 1992-93. He would

also contend that the amount paid towards legal

charges was liable to be deducted from the sale value

when computing capital gains tax when the actual

payment accrued and was paid in the earlier

assessment year 2003-04 and allowing the claim during

current assessment year would distort the profits of the

current year and contends non-consideration of this

aspect by the appellate authorities have resulted in

erroneous order being passed. Hence, he prays for

answering the substantial questions of law in favour of

the revenue.

7. Per contra, Sri A.Shankar, learned Advocate

appearing on behalf of assessee would support the order

of the Tribunal insofar as it has rejected the claim of the

revenue and he would contend that the authorities

erred in disallowing the traveling expenses incurred by

the assessee and merely because there was no business

activity, per se would not indicate that there was no

business activity by the assessee. He would also

elaborate his submission by contending that

professional charges paid to H.M.A.S., an American

based company was on the basis of contract entered

into by the assessee with the said Firm to render

professional services in the form of market input and

other issues as detailed in the contract and accordingly,

as per the contractual term, a sum of $1,00,000 was to

be paid as upfront amount and accordingly, it was paid.

Non-consideration of said plea of the assessee in this

perspective has resulted in great injustice to the

assessee and hence, he prays for substantial questions

of law being answered in favour of the assessee as

formulated in ITA No.684/2009 and he would also pray

for dismissal of the appeal filed by the revenue.

8. RE: FINDING ON SUBSTANTIAL QUESTION OF LAW NO.(1) FORMULATED IN ITA

NO.700/2009.

At the cost of repetition, it is noticed that assessee

had purchased 50,000/- shares of M/s.Diebold HMA

Private Limited during the year 1992-93 and sold the

same during the previous year relevant to the

assessment year 2004-05 for a total consideration of

`21,55,47,800/- and declared a long term capital gain

of `20,51,66,634/- in its return of income. The

assessing Officer denied the benefit of long term capital

gains and held that it should be treated as ‘income from

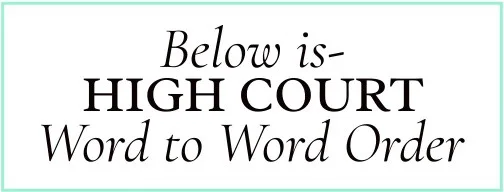

business’. The CIT(A) has noticed that the balance

sheet along with its enclosures of the earlier 2-3 years,

assessee has been showing the value of the shares of

Diebold HMA Private Limited at Rs.50,00,000/- and has

never claimed diminution. It is also noticed by the CIT

(A) that claim for diminution/increase in valuation in

respect of other shares had not been allowed by the

assessing Officer and the assessee had accepted the

same. It has been held that observation made by the

assessing Officer to the effect “assessee has been in the

business of purchase and sale of investments year after

year and has been debiting the P & L A/c with increase

or decrease in the value of investments under the head

‘revaluation of investments’ , is far from the facts. In

that view of the matter, we are not inclined to accept the

contention of the revenue and we are of the considered

view that the finding recorded by the CIT (A) which has

since been affirmed is a question of fact. Hence,

substantial question of law No.(1) is answered in the

affirmative.

9. RE: SUBSTANTIAL QUESTION OF LAW NO.(2) IN ITA No.700/2009 AND SUBSTANTIAL

QUESTIONS OF LAW NOS.(1) AND (2) IN ITA NO.684/2009:

The assessee had claimed a sum of `33,86,284/-

as expenditure relating to travel abroad by the

company’s Managing Director (Sri Harish K Murthy) and

his wife (Smt.Asha Murthy). A sum of `18,55,756/-

came to be disallowed by the assessing Officer on the

ground that there was no business activities in these

years and no explanation was forthcoming to establish

the nexus of travel to that of business purpose.

Undisputedly, before the assessing Officer as well as

before the CIT(A), assessee could not substantiate the

claim by producing cogent evidence with regard to

expenditure incurred towards the Director’s foreign

travel to the extent of disallowance made by the

assessing Officer. The assessee had not discharged the

burden cast on it by furnishing the details like the

business visa, at whose invitation the business trip was

held, proof of any meetings abroad and the details alike.

In that view of the matter, the order of assessing Officer

as affirmed by the lower appellate authorities cannot be

found fault with. In that view of the matter, we are of

the considered view that disallowance made by the

assessing Officer insofar as foreign travel expenditure is

concerned, requires to be affirmed by holding that the

appellate authorities were correct in affirming the

findings of the assessing Officer.

10. The assessing Officer disallowed a sum of Rs.94,74,184/- claimed by the assessee as technical support charges towards promotion of products and

services in North America on the ground that there was no business activities and the agreement on which the assessee based its claim was an agreement which was not put into practice. This finding of the assessing

Officer came to be affirmed by CIT(A) as well as by the Tribunal. The assessee made payment of $1,00,000 on 14.07.2003 and $1,06,000 on 02.12.2003 based on an agreement dated 01.07.2003 contending interalia that such payment was made as per Clause (6) of the agreement and the recipient namely, HMAS was required to render professional services in the form of

furnishing market input and other issues as detailed in

the contract. Undisputedly, assessee did not place any

material to show as to the actual implementation of the

contract and the report which the consultant HMAS had

to furnish to the assessee and as such, in the absence

of any commercial expediency of incurring such

expenditure, the disallowance was sustained by both

the appellate authorities. It cannot be gainsaid by the

assessee that even in the absence of any evidence, the

claim ought to have been allowed. The mere existence

of a technical agreement with HMAS was not sufficient

and there being no business activity in the year under

consideration, the burden was on the assessee to prove

the business expediency to claim expenditure. Hence,

all the authorities were justified in disallowing the claim

or holding that the assessee is not entitled to the

deduction. Accordingly, the questions of law are

answered in the affirmative.

11. RE: SUBSTANTIAL QUESTION OF LAW

NO.(3) IN ITA NO.700/2009 AND ITA NO.684/2009

The assessee also claimed expenditure of

`1,19,09,768/- towards professional charges. Out of

this, the assessing Officer disallowed the assessee’s

claim for deduction of payment of `24,93,800/- and

same was set aside by the CIT(A) on the ground that

there was misinterpretation by the assessing Officer in

respect of payment of professional fees to the legal

advisers and the assessee who had made the payment

in financial year 2002-03, it has been reflected as

advance (pre-paid professional charges). Hence, same

was ordered to be allowed in its entirety namely, to the

extent claimed by the assessee.

12. The Tribunal has rightly noticed that the

exercise undertaken by the assessee in the book is to

transfer the same from pre-paid professional charges to

professional charges account and held that in the year

under consideration, expenditure took place and

accounted for in the books. Hence, the Tribunal found

that the allowance made by the CIT(A) was in

connection with the transfer of shares and hence, it is

to be computed in the income from the long term capital

gains and cannot be allowed while computing the

business income. The said finding of fact by the

authorities does not give rise to the substantial question

of law for being answered in favour of the assessee. As

such, the same is answered in the affirmative.

13. For the reasons aforestated, we proceed to

pass the following:

ORDER

(I) ITA No.700/2009 and ITA No.684/2009 are

hereby dismissed.

(II) Order dated 29.05.2009 passed by Income

Tax Appellate Tribunal, Bangalore Bench in

ITA No.1154/Bang/2009 is hereby affirmed.

(III) The substantial questions of law are

answered as indicated hereinabove.

(IV) No order as to costs.

Sd/-

JUDGE

Sd/-

JUDGE

×

Similar Ripples

Questions

"Capital Gains or Business Income? Court Rules in Favor of Long-Term Capital Gains"

Write your CommentSimilar Posts

Generic

- Reportdata/3670.pdf