Tax Deduction Failure Leads to Penalty: High Court Upholds Section 271C (of Inc…

Full News

Tax Deduction Failure Leads to Penalty: High Court Upholds Section 271C (of Income Tax Act, 1961) Penalty for Non-Compliance with TDS Rules

Tax Deduction Failure Leads to Penalty: High Court Upholds Section 271C (of Income Tax Act, 1961) Penalty for…

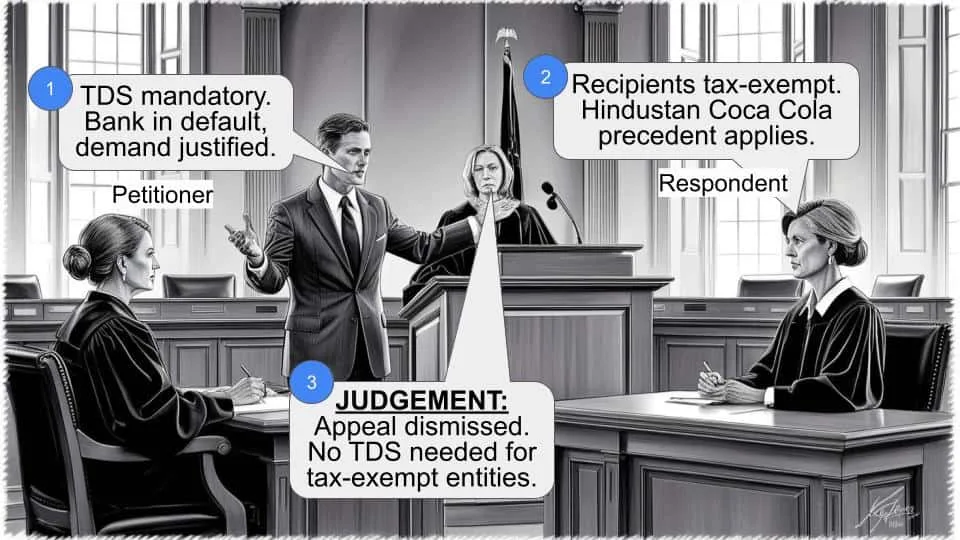

This case involves the Commissioner of Income Tax (the Revenue) challenging an order by the Income Tax Appellate Tribunal that cancelled a penalty imposed on Muthoot Bankers (Aryasala), the assessee. The High Court ruled in favor of the Revenue, reinstating the penalty under Section 271C (of Income Tax Act, 1961) for the assessee’s failure to deduct tax at source as required by Section 194A (of Income Tax Act, 1961).

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax VS Muthoot Bankers (Aryasala) (High Court of Kerala)

ITA. No. 57 of 2007

Date: 6th June 2016

Key Takeaways:

- Failure to deduct tax at source under Section 194A (of Income Tax Act, 1961) attracts penalties under Section 271C (of Income Tax Act, 1961).

- The burden of proving “reasonable cause” under Section 273B (of Income Tax Act, 1961) lies entirely with the assessee.

- Courts should not make assumptions or rely on surmises when evaluating reasonable cause.

- Cancellation of penalties without proper evidence of reasonable cause is illegal.

Issue:

Did the Income Tax Appellate Tribunal err in law by upholding the cancellation of the penalty order under Section 271C (of Income Tax Act, 1961)?

Facts:

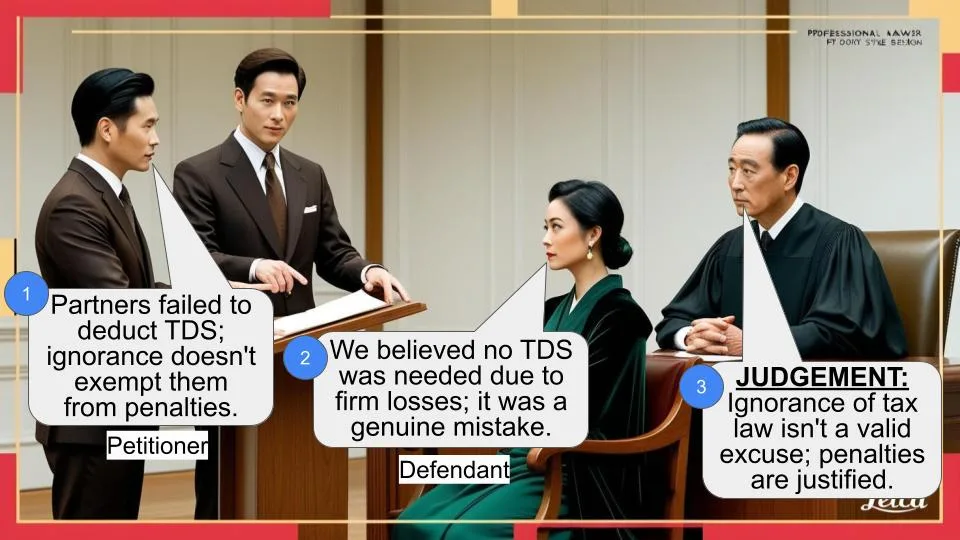

- Muthoot Bankers (Aryasala), a firm engaged in money lending, failed to deduct tax at source on interest payments made to its sister concerns for the assessment year 1998-1999.

- This non-compliance was discovered during an audit.

- The Joint Commissioner initiated proceedings under Section 271C (of Income Tax Act, 1961) and levied a penalty of Rs.10,45,000.

- The assessee admitted to the lapse but requested leniency.

- The Commissioner of Income Tax (Appeals) cancelled the penalty, which was later upheld by the Income Tax Appellate Tribunal.

Arguments:

Revenue’s Arguments:

- The assessee failed to discharge the burden of proof.

- There was no reasonable cause for failure to deduct tax at source.

- The Tribunal considered new reasons not presented before lower authorities.

- The reasons given by the CIT(A) were contradictory and untenable.

Assessee’s Arguments:

- The lapse was technical and deserved a lenient view.

- They requested cancellation of the penalty due to it being a bona fide mistake.

Key Legal Precedents:

- The High Court referred to its own judgment in ITA 139/2013, which established that the burden under Section 273B (of Income Tax Act, 1961) is entirely on the assessee.

- The court also cited a Delhi High Court judgment (253 ITR 745), though the specific details weren’t provided in the context.

Judgement:

- The High Court ruled in favor of the Revenue, setting aside the orders of the CIT(A) and the Tribunal.

- It held that when there’s a failure to deduct tax at source under Section 194A (of Income Tax Act, 1961), penal provisions of Section 271C (of Income Tax Act, 1961) are attracted.

- The court emphasized that the only way for the assessee to avoid penalty was to establish reasonable cause under Section 273B (of Income Tax Act, 1961).

- The High Court found that the assessee failed to produce any evidence to substantiate its claims of reasonable cause.

- The court criticized the CIT(A) for incorrectly placing the burden of proof on the Revenue.

- It also found fault with the Tribunal for relying on mere surmises and assumptions not supported by evidence.

FAQs:

Q: What is Section 194A (of Income Tax Act, 1961)?

A: Section 194A (of Income Tax Act, 1961) deals with the requirement to deduct tax at source on certain interest payments.

Q: What is the significance of Section 273B (of Income Tax Act, 1961) in this case?

A: Section 273B (of Income Tax Act, 1961) provides relief from penalties if the assessee can prove reasonable cause for non-compliance.

Q: Why did the High Court disagree with the Tribunal’s decision?

A: The High Court found that the Tribunal relied on assumptions and reasons not supported by evidence provided by the assessee.

Q: What lesson can businesses learn from this case?

A: It’s crucial to comply with tax deduction at source requirements and maintain proper documentation to prove reasonable cause if there’s a failure to comply.

Q: Can the assessee appeal this decision further?

A: While not mentioned in the judgment, generally, decisions of High Courts can be appealed to the Supreme Court of India.

In this appeal, the Revenue is calling in question the order passed by the Income Tax Appellate Tribunal, Cochin Bench in ITA No. 398/2002 for the assessment year 1998-1999. By the said order, the Tribunal upheld the order passed by the Commissioner of Income Tax (Appeals), by which the Commissioner cancelled the penalty levied under Section 271C (of Income Tax Act, 1961). It is in this background, this appeal is filed with the following questions of law:

“1. Whether, on the facts and in the circumstances of the case the Tribunal is right in law and fact in upholding the cancellation of penalty order by the Commissioner of Income Tax (Appeals).

2. Whether, on the facts and in the circumstances of the case,

i) did the assessee discharge the burden of proof that lay on it.

ii) did the assessee prove that there was reasonable cause for the failure to deduct tax at source?

3. Whether, on the facts and in the circumstances of the case, while considering the cause or causes for the “reasonable cause” under sec 273B (of Income Tax Act, 1961) should not the Tribunal have confined to the causes urged/repeated before the assessing officer/Commissioner of Income Tax (Appeals) and is not consideration of new reasons and sustaining the order of CIT(A) on new reasons without jurisdiction, illegal and vitiated?

4. Whether, on the facts and in the circumstances of the case, are not the reasons urged (para 4 of the order of the Tribunal) in support of 'reasonable cause' under Section 273B (of Income Tax Act, 1961) and considered and relied on by the CIT (A) militating against each other and hence both being non-existing, baseless, untenable, the Tribunal is justified in confirming the order of the CIT(A)?

5. Whether, on the facts and in the circumstances of the case

i) is not the order of the Tribunal against law and facts and also against principle laid down the judgment of the Delhi High Court (253 ITR 745)?

ii) the Tribunal is justified in confirming the order of the CIT(A)?

iii) the Tribunal is right in law in interfering with the order of the Joint Commissioner?”

2. On 03.06.2016, we heard the senior counsel for the revenue. On account of absence of the counsel for the assessee, the case was adjourned to 06.06.2016, when also the counsel for the assessee was absent. Therefore, we proceed to dispose of the appeal on merits.

3. The assessee is a firm engaged in money lending. From the audit report concerning the assessment year in question, it was found that the assessee had not deducted tax at source as required under Section 194A (of Income Tax Act, 1961) on the payments of interest it made to its sister concerns. Therefore, proceedings under Section 271C (of Income Tax Act, 1961) were initiated. In the reply filed, the assessee admitted its lapse and requested that a lenient view should be taken for the technical lapse. However, by Annexure A order, penalty of Rs.10,45,000/-under Section 271C (of Income Tax Act, 1961) was levied. This was cancelled by the Commissioner of Income Tax (Appeals) by Annexure B order where he concluded thus:

“Since the Assessing Officer has not established the absence of reasonable cause in this case, I am of the view that the penalty cannot be sustained legally. Considering all these aspects, I am of the view that the appellant's case deserves a lenient treatment in respect of the bonafide mistake committed by it. The penalty levied u/s 271C (of Income Tax Act, 1961) is accordingly cancelled.”

4. It was this order which was confirmed by the Tribunal.

5. Having heard the Senior Counsel for the revenue and also going through the orders passed by the statutory authorities, we find that it was the admitted case of the assessee that they did not deduct tax at source as required by them under Section 194A (of Income Tax Act, 1961). When there is a failure on the part of the assessee to deduct tax at source in violation of Section 194A (of Income Tax Act, 1961), the penal provisions of Section 271C (of Income Tax Act, 1961) are attracted. In such a case, the only way out for the assessee is to take the benefit of Section 273B (of Income Tax Act, 1961) by establishing that there was reasonable cause justifying their failure to comply with Section 194A (of Income Tax Act, 1961).

Referring to various precedents this Court had occasion to deal with a similar case in the judgment in ITA 139/2013 where it was held that the burden under Section 273B (of Income Tax Act, 1961) is entirely on with the assessee and that a case which is beyond the control of the assessee and which prevents a reasonable man of ordinary prudence acting under normal circumstances, without negligence or inaction or want of bona fides, alone make out a reasonable cause. In this case, Annexure A order of the Joint Commissioner shows that the assessee failed to produce any evidence to substantiate its claims. However, the Commissioner (Appeals) decided the issue by putting the burden on the revenue, which is evident from the extracted portion of the Annexure B order passed by the Commissioner. The order of the Tribunal shows that the Tribunal has given totally different reasons which are mere surmises and assumptions made by it and are not founded on any materials that were made available by the assessee. All this therefore show that the assessee had not established a reasonable cause, as contemplated in Section 273B (of Income Tax Act, 1961) to resist an order of penalty under Section 271C (of Income Tax Act, 1961). Therefore, we find that the Commissioner (Appeals) and the Tribunal acted illegally in cancelling the penalty levied on the assessee. Therefore, answering the question of law in favour of the revenue, this appeal is disposed of.

ANTONY DOMINIC, JUDGE

DAMA SESHADRI NAIDU, JUDGE

×

Questions

Tax Deduction Failure Leads to Penalty: High Court Upholds Section 271C (of Income Tax Act, 1961) Penalty for Non-Compliance with TDS Rules

Write your CommentSimilar Posts

Generic

- Reportdata/2798.pdf