Tax Deductions Allowed for Late PF Payments, Technical Know-How Depreciation

Full News

Tax Deductions Allowed for Late PF Payments, Technical Know-How Depreciation

Tax Deductions Allowed for Late PF Payments, Technical Know-How Depreciation

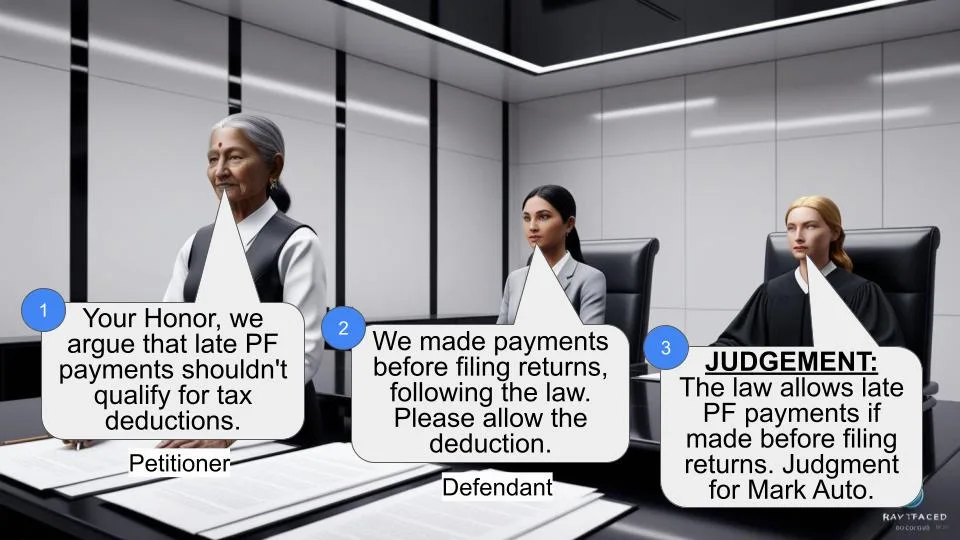

The Income Tax Department (the revenue) appealed against Mark Auto Industries Ltd. (the assessee) regarding two main issues: late payment of Provident Fund (PF) contributions and depreciation on technical know-how expenses. The High Court dismissed the appeal, ruling in favor of the assessee on both counts. It's a win for the company!

Case Name**: Commissioner of Income Tax vs Mark Auto Industries Ltd.

**Key Takeaways**:

1. Late PF payments can still be deducted if made before filing tax returns.

2. Depreciation on capitalized technical know-how expenses doesn't require tax deduction at source.

3. The court relied on previous Supreme Court judgments to make its decision.

**Issue**:

The main questions were:

1. Can the assessee claim deductions for late PF payments?

2. Can the assessee claim depreciation on technical know-how expenses without deducting tax at source?

**Facts**:

Alright, let's break this down:

- The case is about the assessment year 2003-04.

- Mark Auto Industries Ltd. filed a tax return on 27.11.2003, showing a loss of ₹7,90,68,960.

- The Assessing Officer completed the assessment on 28.3.2006, adjusting the loss to ₹7,78,55,860.

- The company appealed to the Commissioner of Income Tax (Appeals), who ruled in their favor.

- The revenue then appealed to the Income Tax Appellate Tribunal, which dismissed their appeal.

- Finally, the revenue brought the case to the High Court.

**Arguments**:

The revenue's main arguments were:

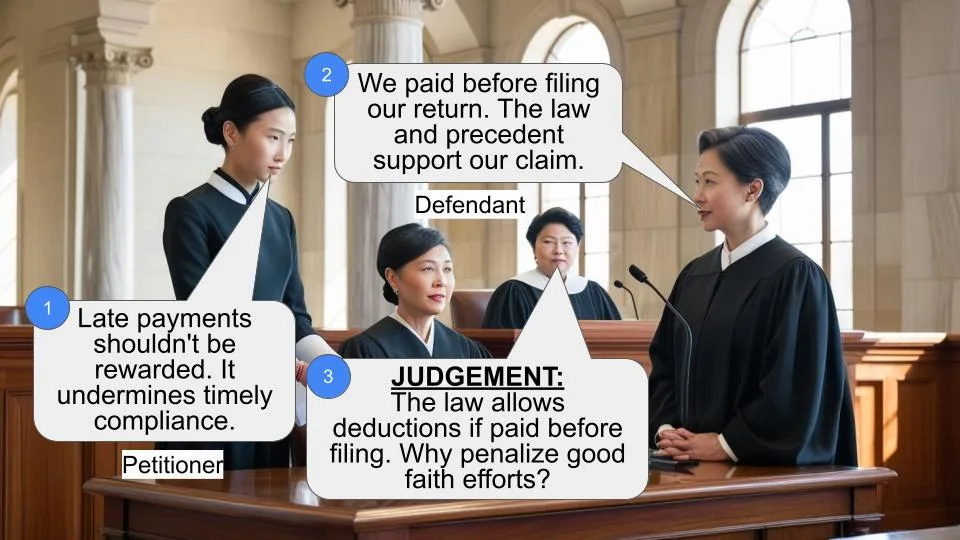

1. Late PF payments shouldn't be allowed as deductions.

2. Depreciation on technical know-how expenses should be disallowed under Section 40(a)(i) (of Income Tax Act, 1961) because no tax was deducted at source.

The assessee argued that:

1. PF payments were made before filing the tax return, so they should be allowed.

2. Technical know-how expenses were capitalized, not claimed as revenue expenditure, so Section 40(a)(i) (of Income Tax Act, 1961) doesn't apply.

**Key Legal Precedents**:

The court relied on two important cases:

1. Commissioner of Income Tax v. Alom Extrusions Ltd. [2009] 319 ITR 306 (SC)

2. The Commissioner of Income Tax, Patiala v. M/s Rai Agro Industries Ltd. Sangrur (Income Tax Appeal No. 663 of 2005, decided on 30.11.2010)

These cases established that the Second Proviso to Section 43B (of Income Tax Act, 1961), which was omitted in 2003, was clarificatory and should be applied retrospectively.

**Judgement**:

The High Court dismissed the revenue's appeal and ruled in favor of Mark Auto Industries Ltd. Here's the breakdown:

1. On PF payments: The court allowed the deduction because the payments were made before filing the tax return under Section 139(1) (of Income Tax Act, 1961).

2. On technical know-how: The court agreed that Section 40(a)(i) (of Income Tax Act, 1961) doesn't apply to capitalized expenses, so depreciation can be claimed without tax deduction at source.

**FAQs**:

1. Q: What's the significance of this judgment for other companies?

A: It clarifies that late PF payments can be deducted if made before filing tax returns, and depreciation on capitalized technical know-how doesn't require tax deduction at source.

2. Q: Does this mean companies can always delay PF payments?

A: Not exactly. While this judgment allows some flexibility, it's still best practice to make PF payments on time to avoid potential issues.

3. Q: How does this affect the treatment of technical know-how expenses?

A: Companies can now be more confident in claiming depreciation on capitalized technical know-how expenses without worrying about tax deduction at source.

4. Q: What sections of the Income Tax Act were key in this case?

A: The main sections discussed were 43B, 40(a)(i), and 139(1) of the Income Tax Act.

5. Q: Could this judgment be overturned in the future?

A: While it's based on Supreme Court precedents, tax laws can change. It's always best to consult with a tax professional for the most up-to-date advice.

1. This appeal has been preferred by the revenue under Section 260A (of Income Tax Act, 1961) (in short “the Act”) against the order dated 8.8.2008 passed by the Income Tax Appellate Tribunal, Delhi Bench “C”, Delhi (hereinafter referred to as “the Tribunal”) in ITA No. 4768/DEL/2007, for the assessment year 2003-04, claiming the following substantial questions of law:-

(i) Whether, on the facts and in the circumstances of the case, the Ld. ITAT was right in law in upholding the order of the Ld. CIT(A) in deleting the addition of Rs.5,24,929/- on account of late payment of PF made by the Assessing Officer u/s 2(24)(x) (of Income Tax Act, 1961) read with section 36(1)(va) (of Income Tax Act, 1961) without appreciating the fact that the payments were made beyond the due date?

(ii) Whether on the facts and in the circumstances of the case Ld. ITAT is right in law in upholding the order of Ld. CIT(A), that the provision of Section 40(a)(i) (of Income Tax Act, 1961) are not applicable to payments of Technical know-how, simply because only part of it is written off by the assessee, each year by way of depreciation u/s 32 (of Income Tax Act, 1961)?

(iii) Whether on the facts and in the circumstances of the case Ld. ITAT is right in law in upholding the order of Ld. CIT(A) ignoring the legal position that section 40 (of Income Tax Act, 1961) provides for non deduction of all amounts allowable u/s 30 (of Income Tax Act, 1961) to 38 and section 35AB (of Income Tax Act, 1961) also falls within these sections?

2. Put shortly, the facts necessary for adjudication of the present appeal as narrated therein are that the assessee filed its return for the assessment year 2003-04 on 27.11.2003 declaring a loss of 7,90,68,960/-. The assessment was completed vide order dated 28.3.2006 at a loss of 7,78,55,860/-. Feeling aggrieved, the assessee filed an appeal before the Commissioner of Income Tax (Appeals) [in short “the CIT(A)”]. The CIT(A) vide order dated 19.9.2007 allowed the appeal and observed with regard to addition of ` 5,24,929/- under Section 43B (of Income Tax Act, 1961) that the Assessing Officer should verify the details and allow the deduction in case the payments had been made within grace period allowed under the statute and deleted the addition of ` 6,88,175/- on account of technical know how that the provisions of Section 40(a)(i) (of Income Tax Act, 1961) were not attracted to capitalized expenditure on technical know how. Being dissatisfied with the order of the CIT(A), the revenue filed an appeal before the Tribunal. The Tribunal vide order dated 8.8.2008 dismissed the appeal. Hence, the present appeal by the revenue.

3. We have heard learned counsel for the revenue.

4. Regarding question (i), learned counsel for the appellant could not dispute that the issue raised herein finally stands settled by the Apex Court judgment in Commissioner of Income Tax v. Alom Extrusions Ltd. [2009] 319 ITR 306 (SC) and this Court in Income Tax Appeal No. 663 of 2005 (The Commissioner of Income Tax, Patiala v. M/s Rai Agro Industries Ltd. Sangrur), decided on 30.11.2010 wherein it has been held that Second Proviso to Section 43B (of Income Tax Act, 1961) omitted by Finance Act, 2003 with effect from 1.4.2004 was clarificatory in nature and was to operate retrospectively. Once that is so, in the present case, the respondent-assessee was entitled to deduction in respect of employer and employee's contribution to ESI and Provident Fund as the same had been deposited prior to the filing of the return under Section 139(1) (of Income Tax Act, 1961). Thus, question (i) stands answered against the revenue and in favour of the assessee.

5. Adverting to questions (ii) and (iii), the issue which arises for consideration is whether the assessee could be disallowed claim for depreciation under Section 40(a)(i) (of Income Tax Act, 1961) on the ground that the payments made for technical know-how which had been capitalized, no tax deduction at source has been made thereon. The Tribunal while accepting the plea of the assessee, in para 3, had noticed as under:- “3. Ground no.4 is against deletion of an addition of Rs.6,88,175/- made by the AO on account of deduction of depreciation on technical know-how as the assessee failed to deduct tax in accordance with the provision contained in section 40(a)(i) (of Income Tax Act, 1961). The finding of the learned CIT(A) was that the assessee had incurred expenditure by way of technical know-how, which was capitalized amount as made in the return of income. Since the assessee had not claimed deduction for the amount paid, the provisions contained in section 40(a) (of Income Tax Act, 1961)

(i) were not attracted. The learned DR could not find any fault with this direction of the CIT(A) also although she referred to page 4 of the assessment order, where it was mentioned that the tax deducted in respect of the payment was made over to the Government in the subsequent year and, therefore, depreciation could not be deducted on the capital expenditure incurred by the assessee. In reply, the learned counsel pointed out that the expenditure by way of technical know-how was capitalized and it was not claimed as revenue expenditure. Therefore, there was also no reason to disallow depreciation on such capitalized amount as the aforesaid provision does not deal with deduction of depreciation. Having considered arguments from both the sides, we are of the view that there is no error in the order of the learned CIT(A) which requires correction from us. Thus, this ground is also dismissed.”

6. Learned counsel for the revenue was unable to substantiate that in the absence of any requirement of law for making deduction of tax out of the expenditure on technical know how which was capitalized and no amount was claimed as revenue expenditure, the deduction could be disallowed under Section 40(a)(i) (of Income Tax Act, 1961). Accordingly, no infirmity could be found in the order passed by the Tribunal which may warrant interference by this Court. Thus, both the questions are answered against the revenue and in favour of the assessee.

7. Consequently, the appeal is dismissed.

(AJAY KUMAR MITTAL) JUDGE October 8, 2012 (G.S. SANDHAWALIA) gbs JUDGE

×

Similar Ripples

Questions

Tax Deductions Allowed for Late PF Payments, Technical Know-How Depreciation

Write your CommentSimilar Posts

Generic

- Reportdata/5389.pdf